import pandas as pd

import numpy as np

import math

from itables import show

np.random.seed(260)Objective

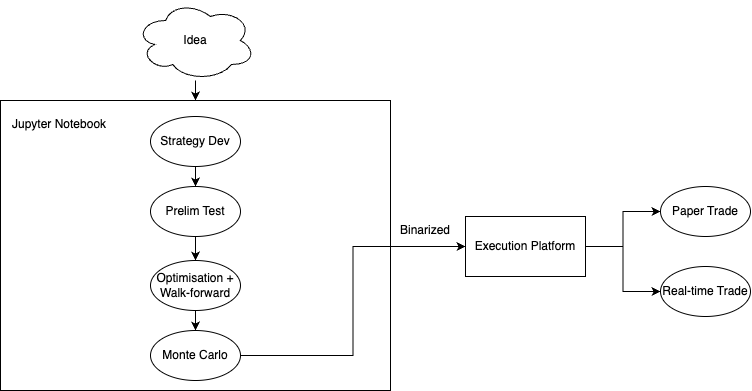

To be able to speed up the system evaluation in a robust manner, here is the template that will be used for develop trading strategy. This notebook will contain all the code required to translate from idea to prelim test. At the end, the strategy will be saved and send to the more robust testing and evaluation platform.

Here is the general workflow of formulating and testing a strategy:

I will use a n-day breakout strategy for demonstration. We will optimise the parameter \(n\) in the evaluation platform.

Developing the strategy

A strategy will have the following components:

Market Selection: Balance between robustness and adaptation

Entry rules

Exit rules

- Stop and reverse, Technical-based exits, Breakeven stops, Stop-losses, Profit targets, Trailing stops

Timeframe/bar size: Daily, Weekly, Monthly. Intentially exclude intra-day to fit my requirements

Consideration between noise and sensitivity

Consideration between more trades and less trades

Consideration of slippage and transaction costs

Programming Consideration: Can you program the strategy?

Data Consideration

How much data should you use?

Futures: Should you use continuous contract data?

Forex: How do you test with Forex data?

Market Selection

Equity:

US: IYY, SPY, QQQ, IWM

Asia: FXI, EWJ, VNM, INDA, EWY, EWT

Europe: EWQ, EWI, EWG, EWU

South America: ARGT, EWW, EWZ

Emerging markets: ACWX, EEM

Bonds: SHY(1-3 years TBond), TLT (20+ Year Treasury Bond)

Commodities: GC, SI, HG, CL, NG, HO, RB, CT, ZC, ZS, ZL, ZW, SB

Forex: 6A, 6B, 6C, 6E, 6J, 6S, 6N, DX

universe = [

"IYY", "SPY", "QQQ", "IWM",

"FXI", "EWJ", "VNM", "INDA", "EWY", "EWT",

"EWQ", "EWI", "EWG", "EWU",

"ARGT", "EWW", "EWZ",

"SHY", "TLT",

"GC=F", "SI=F", "HG=F", "CL=F", "NG=F", "HO=F", "RB=F", "CT=F", "ZC=F", "ZS=F",

"ZL=F", "ZW=F", "SB=F",

"6A=F", "6B=F", "6C=F", "6E=F", "6J=F", "6S=F", "6N=F", "DX=F"

]

import yfinance as yf

tickers = yf.Tickers(universe)

# SPY will be used as sample data for prelim test

SPY = tickers.tickers['SPY'].history(start = "2008-01-01", end = "2025-02-28")Strategy Template

The following block is the strategy template. In the following test, we will subclass the major class BreakoutStrategy to modify the input and output rules.

from backtesting.lib import crossover

from backtesting import Strategy

from strategy.BaseStrategy import BaseStrategy

from strategy.Indicators import HighestInNBars, LowestInNBars

import talib

class BreakoutStrategy(BaseStrategy):

"""

Base Strategy Class

"""

# Parameters that can be optimised

entry_n = 20

exit_n = 5

atr_period = 14

initial_stop_atr_multiplier = 2

trailing_stop_atr_multiplier = 2

# Money management

risk_per_trade = 0.01 # 1%

def init(self):

self.highest_close_entry_n = self.I(HighestInNBars, self.data.High, self.entry_n)

self.lowest_close_entry_n = self.I(LowestInNBars, self.data.Low, self.entry_n)

self.highest_close_exit_n = self.I(HighestInNBars, self.data.High, self.exit_n)

self.lowest_close_exit_n = self.I(LowestInNBars, self.data.Low, self.exit_n)

self.atr = self.I(talib.ATR,

self.data.High,

self.data.Low,

self.data.Close,

timeperiod=14)

self.risk_unit = self.equity * self.risk_per_trade

print(self.risk_unit)

self.long_entry_signal = self.data.Close > self.highest_close_entry_n

self.short_entry_signal = self.data.Close < self.lowest_close_entry_n

def store_indicators(self):

# Store the data you want to display later in a DataFrame

signals_df = pd.DataFrame({

'Date': self.data.index,

'Close': self.data.Close,

'highest_n_entry': self.highest_close_entry_n,

'lowest_n_entry': self.lowest_close_entry_n,

'long_highest_n_exit': self.highest_close_exit_n,

'short_lowest_n_exit': self.lowest_close_exit_n,

'atr': self.atr,

'long_entry_signal': self.long_entry_signal,

'short_entry_signal': self.short_entry_signal

})

return signals_df

def entry_rule(self):

"""

Entry Long if price breaks out from last n high.

"""

if self.data.Close > self.highest_close_entry_n:

return 1

elif self.data.Close < self.lowest_close_entry_n:

return -1

else:

return 0

def exit_rule(self):

"""

Here we define the exit rule

"""

return 0

def update_trailing_stop(self):

# Use fixed ATR trailing stop

for trade in self.trades:

if trade.is_long:

trailing_sl = self.lowest_close_exit_n[-1] - self.trailing_stop_atr_multiplier * self.atr[-1]

trade.sl = max(trade.sl, trailing_sl)

else: # short

trailing_sl = self.highest_close_exit_n[-1] + self.trailing_stop_atr_multiplier * self.atr[-1]

trade.sl = min(trade.sl, trailing_sl)

def next(self):

if not self.position:

# Get entry price - Entry at market

last_close = self.data.Close[-1]

last_atr = self.atr[-1]

if self.entry_rule() == 1:

sl = last_close - self.initial_stop_atr_multiplier * last_atr

size = self.get_position_size(last_close, sl)

tp = self.get_tp_level(last_close, size, 2)

self.buy(size=size, sl=sl, tp=tp)

elif self.entry_rule() == -1:

sl = last_close + self.initial_stop_atr_multiplier * last_atr

size = self.get_position_size(last_close, sl)

tp = self.get_tp_level(last_close, size, False, 2)

self.sell(size=size, sl=sl, tp=tp)

else:

self.update_trailing_stop()

if self.exit_rule() == 1:

self.position.close()Entry rules

- Entry if the price break out from past 20 day new high

def entry_rule(self):

"""

Entry Long if price breaks out from last n high.

"""

if self.data.Close > self.highest_close_entry_n:

return 1

elif self.data.Close < self.lowest_close_entry_n:

return -1

else:

return 0Exit rules

This strategy will only use stop loss and trailing stop as exit rules.

Initial stop at entry - 2 x ATR

Last 5 day lowest low - 1 ATR

At this stage, this is define within the self.buy(sl=..., tp=...) and self.sell(sl=..., tp=...) function

def next(self):

if not self.position:

# Get entry price - Entry at market

last_close = self.data.Close[-1]

last_atr = self.atr[-1]

if self.entry_rule() == 1:

sl = last_close - self.initial_stop_atr_multiplier * last_atr

size = self.get_position_size(last_close, sl)

self.buy(size=size, sl=sl, tp=tp)

elif self.entry_rule() == -1:

sl = last_close + self.initial_stop_atr_multiplier * last_atr

size = self.get_position_size(last_close, sl)

self.sell(size=size, sl=sl, tp=tp)

else:

self.update_trailing_stop()

if self.exit_rule() == 1:

self.position.close()Prelim test

Objective

The objective of Prelim test is to see if the system has potential. If the system survive perlim test, then it makes sense to progress to more rigorous full test.

Data Consideration

In prelim test, we will only run a strategy on a set of data one time, and one time only. If it works, great, but if it doesn’t work, we should just move on to the next data set or instrument.

If we have 10 years of data for full test, in prelim test we will just use 1/5 of the data. We should try to squeeze it as little as possible, while still getting enough trades to be statistically meaningful. We can take the section of data random, by not using the same data all the time or favouring any particular years.

Coverage

Prelim test will cover Entry Test, Exit Test, and Grid Test.

- Random Entry and Exit test

Prelim Test 1 - Entry Test

Objective: We want to know whether the entry has any usefulness

Options:

Fixed-stop and target exit: Exit based on a fixed trailing stop of 4xATR of previous close, and TP at 2R profit

Fixed-bar exit: Exit always at the 10th bar

Random exit: Flip a coin. If head, then exit.

Evaluation Criteria:

Winning Percentage: If without commission and slippage, a good strategy should have over 50% win rate

Expectancy: We could argue that for some strategies, win rate tend to be lower. We can also check the expectancy and that should be positive.

We don’t need to worry about drawdowns or any other metrics in Prelim test

RANDOM_TEST_PERIOD_DAYS = 600class BreakoutStrategyEntryTest1(BreakoutStrategy):

def init(self):

super().init()

# Trailing stop ATR multiplier

self.initial_stop_atr_multiplier = 2

self.trailing_stop_atr_multiplier = 2

self.orders_log = []

def next(self):

order = None

if not self.position:

# Get entry price - Entry at market

last_close = self.data.Close[-1]

last_atr = self.atr[-1]

if self.entry_rule() == 1:

initial_sl = self.lowest_close_exit_n[-1] - self.initial_stop_atr_multiplier * last_atr

size = self.get_position_size(last_close, initial_sl)

# size = 1

tp = self.get_tp_level(last_close, size, 2)

order = self.buy(size=size, sl=initial_sl, tp=tp)

elif self.entry_rule() == -1:

initial_sl = self.highest_close_exit_n[-1] + self.initial_stop_atr_multiplier * last_atr

size = self.get_position_size(last_close, initial_sl)

# size = 1

tp = self.get_tp_level(last_close, size, False, 2)

order = self.sell(size=size, sl=initial_sl, tp=tp)

else:

self.update_trailing_stop()Show the code

from backtesting import Backtest

num_trades = 0

while(num_trades == 0):

rnd_date = np.random.choice(SPY.index)

selection = SPY.loc[rnd_date:rnd_date + pd.Timedelta(days=RANDOM_TEST_PERIOD_DAYS), :]

bt = Backtest(selection,

BreakoutStrategyEntryTest1,

cash=10_000)

stats = bt.run()

signals_df = stats._strategy.store_indicators()

# orders = stats._strategy.orders_log

num_trades = stats["# Trades"]100.0bt.plot()/Users/raylai/Library/Caches/org.R-project.R/R/reticulate/uv/cache/archive-v0/n27kI_pu2kgd7cyXmF2Fh/lib/python3.11/site-packages/bokeh/util/serialization.py:242: UserWarning: no explicit representation of timezones available for np.datetime64

return convert(array.astype("datetime64[us]"))GridPlot(

id = 'p3651', …)

Show the code

prelim1_stats = pd.DataFrame(stats)Show the code

# Show all trades

show(stats["_trades"])| Size | EntryBar | ExitBar | EntryPrice | ExitPrice | SL | TP | PnL | ReturnPct | EntryTime | ExitTime | Duration | Tag | Entry_HighestIn…(H,20) | Exit_HighestIn…(H,20) | Entry_LowestInN…(L,20) | Exit_LowestInN…(L,20) | Entry_HighestIn…(H,5) | Exit_HighestIn…(H,5) | Entry_LowestInN…(L,5) | Exit_LowestInN…(L,5) | Entry_ATR(H,L,C,14) | Exit_ATR(H,L,C,14) |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Loading ITables v2.2.5 from the internet... (need help?) |

class BreakoutStrategyEntryTest2(BreakoutStrategy):

entry_index = None # To track the bar where we entered

num_bars_after_entry = 10 # Exit after 10 bars if no profit

def next(self):

if not self.position:

# Get entry price - Entry at market

last_close = self.data.Close[-1]

last_atr = self.atr[-1]

if self.entry_rule() == 1:

initial_sl = self.lowest_close_exit_n[-1] - self.initial_stop_atr_multiplier * last_atr

size = self.get_position_size(last_close, initial_sl)

# size = 1

tp = self.get_tp_level(last_close, size, 2)

order = self.buy(size=size, sl=initial_sl, tp=tp)

elif self.entry_rule() == -1:

initial_sl = self.highest_close_exit_n[-1] + self.initial_stop_atr_multiplier * last_atr

size = self.get_position_size(last_close, initial_sl)

# size = 1

tp = self.get_tp_level(last_close, size, False, 2)

order = self.sell(size=size, sl=initial_sl, tp=tp)

else:

if (self.entry_index is not None and (self.data.index[-1] - self.entry_index).days >= self.num_bars_after_entry):

self.position.close() # Close all positions

self.entry_index = None # Reset entry trackingShow the code

num_trades = 0

while(num_trades == 0):

rnd_date = np.random.choice(SPY.index)

selection = SPY.loc[rnd_date:rnd_date + pd.Timedelta(days=RANDOM_TEST_PERIOD_DAYS), :]

bt = Backtest(selection,

BreakoutStrategyEntryTest2,

cash=10_000)

stats = bt.run()

num_trades = stats["# Trades"]100.0bt.plot()/Users/raylai/Library/Caches/org.R-project.R/R/reticulate/uv/cache/archive-v0/n27kI_pu2kgd7cyXmF2Fh/lib/python3.11/site-packages/bokeh/util/serialization.py:242: UserWarning: no explicit representation of timezones available for np.datetime64

return convert(array.astype("datetime64[us]"))GridPlot(

id = 'p4098', …)

Show the code

prelim2_stats = pd.DataFrame(stats)Show the code

# Show all trades

show(stats["_trades"])| Size | EntryBar | ExitBar | EntryPrice | ExitPrice | SL | TP | PnL | ReturnPct | EntryTime | ExitTime | Duration | Tag | Entry_HighestIn…(H,20) | Exit_HighestIn…(H,20) | Entry_LowestInN…(L,20) | Exit_LowestInN…(L,20) | Entry_HighestIn…(H,5) | Exit_HighestIn…(H,5) | Entry_LowestInN…(L,5) | Exit_LowestInN…(L,5) | Entry_ATR(H,L,C,14) | Exit_ATR(H,L,C,14) |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Loading ITables v2.2.5 from the internet... (need help?) |

class BreakoutStrategyEntryTest3(BreakoutStrategy):

entry_index = None # To track the bar where we entered

def next(self):

if not self.position:

# Get entry price - Entry at market

last_close = self.data.Close[-1]

last_atr = self.atr[-1]

if self.entry_rule() == 1:

initial_sl = self.lowest_close_exit_n[-2] - self.initial_stop_atr_multiplier * last_atr

size = self.get_position_size(last_close, initial_sl)

# size = 1

tp = self.get_tp_level(last_close, size, 2)

order = self.buy(size=size, sl=initial_sl, tp=tp)

elif self.entry_rule() == -1:

initial_sl = self.highest_close_exit_n[-2] + self.initial_stop_atr_multiplier * last_atr

size = self.get_position_size(last_close, initial_sl)

# size = 1

tp = self.get_tp_level(last_close, size, False, 2)

order = self.sell(size=size, sl=initial_sl, tp=tp)

else:

# Random Exit

if (np.random.uniform(0, 1) > 0.5):

self.position.close() Show the code

num_trades = 0

while(num_trades == 0):

rnd_date = np.random.choice(SPY.index)

selection = SPY.loc[rnd_date:rnd_date + pd.Timedelta(days=RANDOM_TEST_PERIOD_DAYS), :]

bt = Backtest(selection,

BreakoutStrategyEntryTest3,

cash=10_000)

stats = bt.run()

num_trades = stats["# Trades"]100.0bt.plot()/Users/raylai/Library/Caches/org.R-project.R/R/reticulate/uv/cache/archive-v0/n27kI_pu2kgd7cyXmF2Fh/lib/python3.11/site-packages/bokeh/util/serialization.py:242: UserWarning: no explicit representation of timezones available for np.datetime64

return convert(array.astype("datetime64[us]"))GridPlot(

id = 'p4545', …)

prelim3_stats = pd.DataFrame(stats)# Show all trades

show(stats["_trades"])| Size | EntryBar | ExitBar | EntryPrice | ExitPrice | SL | TP | PnL | ReturnPct | EntryTime | ExitTime | Duration | Tag | Entry_HighestIn…(H,20) | Exit_HighestIn…(H,20) | Entry_LowestInN…(L,20) | Exit_LowestInN…(L,20) | Entry_HighestIn…(H,5) | Exit_HighestIn…(H,5) | Entry_LowestInN…(L,5) | Exit_LowestInN…(L,5) | Entry_ATR(H,L,C,14) | Exit_ATR(H,L,C,14) |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Loading ITables v2.2.5 from the internet... (need help?) |

Result

| Win Rate | Expectancy | |

|---|---|---|

| Fixed Stop and Target | 38.461538 | -1.802268 |

| 10-bar Exit | 100.000000 | 17.930682 |

| Random Exit | 51.219512 | -0.034099 |

Prelim Test 2 - Exit Test

Objective: We want to know whether the exit has any usefulness

Options:

Similar-approach Entry: If Trend-following, use n-bar breakout; If countertrend, use RSI entry

Random Entry

Since our entry strategy has been using n-bar breakout. We will just test Random Entry. Our exit rule is 4xATR of previous close

class BreakoutStrategyExitTest1(BreakoutStrategy):

# Trailing stop ATR multiplier

trailing_stop_atr_multiplier = 4

def entry_rule(self):

"""

Random Entry rule

Flip a coin, if head, Flip again to enter either long or short

"""

if np.random.uniform(0, 1) > 0.5:

return 1 if np.random.uniform(0, 1) > 0.5 else -1

else:

return 0

def update_trailing_stop(self):

# Use fixed ATR trailing stop

for trade in self.trades:

if trade.is_long:

trailing_sl = self.data.Close[-2] - self.trailing_stop_atr_multiplier * self.atr[-2]

trade.sl = max(trade.sl, trailing_sl)

else: # short

trailing_sl = self.data.Close[-2] + self.trailing_stop_atr_multiplier * self.atr[-2]

trade.sl = min(trade.sl, trailing_sl)

def next(self):

if not self.position:

# Get entry price - Entry at market

last_close = self.data.Close[-1]

last_atr = self.atr[-1]

if self.entry_rule() == 1:

sl = last_close - self.initial_stop_atr_multiplier * last_atr

size = self.get_position_size(last_close, sl)

tp = self.get_tp_level(last_close, size, 2)

self.buy(size=size, sl=sl, tp=tp)

elif self.entry_rule() == -1:

sl = last_close + self.initial_stop_atr_multiplier * last_atr

size = self.get_position_size(last_close, sl)

tp = self.get_tp_level(last_close, size, False, 2)

self.sell(size=size, sl=sl, tp=tp)

else:

self.update_trailing_stop()Show the code

num_trades = 0

while(num_trades == 0):

rnd_date = np.random.choice(SPY.index)

selection = SPY.loc[rnd_date:rnd_date + pd.Timedelta(days=RANDOM_TEST_PERIOD_DAYS), :]

bt = Backtest(selection,

BreakoutStrategyExitTest1,

cash=10_000)

stats = bt.run()

num_trades = stats["# Trades"]100.0bt.plot()/Users/raylai/Library/Caches/org.R-project.R/R/reticulate/uv/cache/archive-v0/n27kI_pu2kgd7cyXmF2Fh/lib/python3.11/site-packages/bokeh/util/serialization.py:242: UserWarning: no explicit representation of timezones available for np.datetime64

return convert(array.astype("datetime64[us]"))GridPlot(

id = 'p4992', …)

exit_prelim1_stats = pd.DataFrame(stats)# Show all trades

show(stats["_trades"])| Size | EntryBar | ExitBar | EntryPrice | ExitPrice | SL | TP | PnL | ReturnPct | EntryTime | ExitTime | Duration | Tag | Entry_HighestIn…(H,20) | Exit_HighestIn…(H,20) | Entry_LowestInN…(L,20) | Exit_LowestInN…(L,20) | Entry_HighestIn…(H,5) | Exit_HighestIn…(H,5) | Entry_LowestInN…(L,5) | Exit_LowestInN…(L,5) | Entry_ATR(H,L,C,14) | Exit_ATR(H,L,C,14) |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Loading ITables v2.2.5 from the internet... (need help?) |

| 0 | |

|---|---|

| Start | 2018-05-04 00:00:00-04:00 |

| End | 2019-12-24 00:00:00-05:00 |

| Duration | 599 days 01:00:00 |

| Exposure Time [%] | 84.541063 |

| Equity Final [$] | 9122.465625 |

| Equity Peak [$] | 10387.226181 |

| Return [%] | -8.775344 |

| Buy & Hold Return [%] | 20.843784 |

| Return (Ann.) [%] | -5.437163 |

| Volatility (Ann.) [%] | 5.00404 |

| CAGR [%] | -3.789973 |

| Sharpe Ratio | -1.086555 |

| Sortino Ratio | -1.300484 |

| Calmar Ratio | -0.36223 |

| Alpha [%] | -12.268918 |

| Beta | 0.167608 |

| Max. Drawdown [%] | -15.010238 |

| Avg. Drawdown [%] | -2.179718 |

| Max. Drawdown Duration | 474 days 00:00:00 |

| Avg. Drawdown Duration | 61 days 00:00:00 |

| # Trades | 32 |

| Win Rate [%] | 21.875 |

| Best Trade [%] | 10.436857 |

| Worst Trade [%] | -5.211667 |

| Avg. Trade [%] | -0.686613 |

| Max. Trade Duration | 55 days 00:00:00 |

| Avg. Trade Duration | 15 days 00:00:00 |

| Profit Factor | 0.626365 |

| Expectancy [%] | -0.632254 |

| SQN | -1.187401 |

| Kelly Criterion | -0.131341 |

| _strategy | BreakoutStrategyExitTest1 |

| _equity_curve | Equity Drawd... |

| _trades | Size EntryBar ExitBar EntryPrice Exit... |

Prelim Test 3 - Grid Test

In Grid test, we will do limited optimisation on the parameters.

Entry Rules: We will test the number of days for the breakout. [5, 15, 30, 60, 90, 120]

Exit Rules: We will test the multiplier of ATR at the trailing stop [1, 2, 3, 4, 99 (No stop loss)], and the profit taking multiplier [2, 3, 4, 5]

Evaluation Criteria

We would expect a good strategy will have >= 70% of iterations to be profitable

In the range between 30% to 70%, we will see if there’s anything worth to work on

Below 30%, either do the flip side, or discard the system.

import types

import sys

from strategy.BreakoutStrategy import BreakoutStrategy

# Parameters to test

entry_n_parameters = [5, 15, 30, 60, 90, 120]

exit_n_parameters = [5, 10, 15, 20]

exit_rule_trialing_stop_parameters = [1, 3, 4, 99]

num_trades = 0

if '__spec__' not in dir():

sys.modules['__main__'].__spec__ = types.SimpleNamespace()

while(num_trades == 0):

rnd_date = np.random.choice(SPY.index)

selection = SPY.loc[rnd_date:rnd_date + pd.Timedelta(days=RANDOM_TEST_PERIOD_DAYS), :]

selection.set_index(selection.index.tz_localize(tz=None), inplace=True)

bt_opt = Backtest(selection,

BreakoutStrategy,

cash=10_000)

stats, heatmap = bt_opt.optimize(

entry_n=entry_n_parameters,

exit_n=exit_n_parameters,

trailing_stop_atr_multiplier=exit_rule_trialing_stop_parameters,

maximize='Sharpe Ratio',

max_tries=200,

random_state=42,

return_heatmap=True)

num_trades = stats["# Trades"]/Users/raylai/Library/Caches/org.R-project.R/R/reticulate/uv/cache/archive-v0/n27kI_pu2kgd7cyXmF2Fh/lib/python3.11/site-packages/numpy/lib/_function_base_impl.py:552: RuntimeWarning: Mean of empty slice.

avg = a.mean(axis, **keepdims_kw)

/Users/raylai/Library/Caches/org.R-project.R/R/reticulate/uv/cache/archive-v0/n27kI_pu2kgd7cyXmF2Fh/lib/python3.11/site-packages/numpy/_core/_methods.py:137: RuntimeWarning: invalid value encountered in divide

ret = um.true_divide(

/Users/raylai/Library/Caches/org.R-project.R/R/reticulate/uv/cache/archive-v0/n27kI_pu2kgd7cyXmF2Fh/lib/python3.11/site-packages/backtesting/_stats.py:157: RuntimeWarning: Degrees of freedom <= 0 for slice

cov_matrix = np.cov(equity_log_returns, market_log_returns)

/Users/raylai/Library/Caches/org.R-project.R/R/reticulate/uv/cache/archive-v0/n27kI_pu2kgd7cyXmF2Fh/lib/python3.11/site-packages/numpy/lib/_function_base_impl.py:2894: RuntimeWarning: divide by zero encountered in divide

c *= np.true_divide(1, fact)

/Users/raylai/Library/Caches/org.R-project.R/R/reticulate/uv/cache/archive-v0/n27kI_pu2kgd7cyXmF2Fh/lib/python3.11/site-packages/numpy/lib/_function_base_impl.py:2894: RuntimeWarning: invalid value encountered in multiply

c *= np.true_divide(1, fact)

/Users/raylai/Library/Caches/org.R-project.R/R/reticulate/uv/cache/archive-v0/n27kI_pu2kgd7cyXmF2Fh/lib/python3.11/site-packages/backtesting/_plotting.py:55: UserWarning: Jupyter Notebook detected. Setting Bokeh output to notebook. This may not work in Jupyter clients without JavaScript support, such as old IDEs. Reset with `backtesting.set_bokeh_output(notebook=False)`.

warnings.warn('Jupyter Notebook detected. '

/Users/raylai/Library/Caches/org.R-project.R/R/reticulate/uv/cache/archive-v0/n27kI_pu2kgd7cyXmF2Fh/lib/python3.11/site-packages/backtesting/_plotting.py:55: UserWarning: Jupyter Notebook detected. Setting Bokeh output to notebook. This may not work in Jupyter clients without JavaScript support, such as old IDEs. Reset with `backtesting.set_bokeh_output(notebook=False)`.

warnings.warn('Jupyter Notebook detected. '

/Users/raylai/Library/Caches/org.R-project.R/R/reticulate/uv/cache/archive-v0/n27kI_pu2kgd7cyXmF2Fh/lib/python3.11/site-packages/backtesting/_plotting.py:55: UserWarning: Jupyter Notebook detected. Setting Bokeh output to notebook. This may not work in Jupyter clients without JavaScript support, such as old IDEs. Reset with `backtesting.set_bokeh_output(notebook=False)`.

warnings.warn('Jupyter Notebook detected. '

/Users/raylai/Library/Caches/org.R-project.R/R/reticulate/uv/cache/archive-v0/n27kI_pu2kgd7cyXmF2Fh/lib/python3.11/site-packages/backtesting/_plotting.py:55: UserWarning: Jupyter Notebook detected. Setting Bokeh output to notebook. This may not work in Jupyter clients without JavaScript support, such as old IDEs. Reset with `backtesting.set_bokeh_output(notebook=False)`.

warnings.warn('Jupyter Notebook detected. '

/Users/raylai/Library/Caches/org.R-project.R/R/reticulate/uv/cache/archive-v0/n27kI_pu2kgd7cyXmF2Fh/lib/python3.11/site-packages/backtesting/_plotting.py:55: UserWarning: Jupyter Notebook detected. Setting Bokeh output to notebook. This may not work in Jupyter clients without JavaScript support, such as old IDEs. Reset with `backtesting.set_bokeh_output(notebook=False)`.

warnings.warn('Jupyter Notebook detected. '

/Users/raylai/Library/Caches/org.R-project.R/R/reticulate/uv/cache/archive-v0/n27kI_pu2kgd7cyXmF2Fh/lib/python3.11/site-packages/backtesting/_plotting.py:55: UserWarning: Jupyter Notebook detected. Setting Bokeh output to notebook. This may not work in Jupyter clients without JavaScript support, such as old IDEs. Reset with `backtesting.set_bokeh_output(notebook=False)`.

warnings.warn('Jupyter Notebook detected. '

/Users/raylai/Library/Caches/org.R-project.R/R/reticulate/uv/cache/archive-v0/n27kI_pu2kgd7cyXmF2Fh/lib/python3.11/site-packages/backtesting/_plotting.py:55: UserWarning: Jupyter Notebook detected. Setting Bokeh output to notebook. This may not work in Jupyter clients without JavaScript support, such as old IDEs. Reset with `backtesting.set_bokeh_output(notebook=False)`.

warnings.warn('Jupyter Notebook detected. '

/Users/raylai/Library/Caches/org.R-project.R/R/reticulate/uv/cache/archive-v0/n27kI_pu2kgd7cyXmF2Fh/lib/python3.11/site-packages/backtesting/_plotting.py:55: UserWarning: Jupyter Notebook detected. Setting Bokeh output to notebook. This may not work in Jupyter clients without JavaScript support, such as old IDEs. Reset with `backtesting.set_bokeh_output(notebook=False)`.

warnings.warn('Jupyter Notebook detected. '| 0 | |

|---|---|

| Start | 2012-12-14 00:00:00 |

| End | 2014-08-06 00:00:00 |

| Duration | 600 days 00:00:00 |

| Exposure Time [%] | 51.815981 |

| Equity Final [$] | 10025.487778 |

| Equity Peak [$] | 10030.943649 |

| Return [%] | 0.254878 |

| Buy & Hold Return [%] | 26.176484 |

| Return (Ann.) [%] | 0.155441 |

| Volatility (Ann.) [%] | 0.137324 |

| CAGR [%] | 0.10697 |

| Sharpe Ratio | 1.131934 |

| Sortino Ratio | 1.577773 |

| Calmar Ratio | 1.720393 |

| Alpha [%] | -0.032248 |

| Beta | 0.010969 |

| Max. Drawdown [%] | -0.090352 |

| Avg. Drawdown [%] | -0.020682 |

| Max. Drawdown Duration | 150 days 00:00:00 |

| Avg. Drawdown Duration | 16 days 00:00:00 |

| # Trades | 1 |

| Win Rate [%] | 100.0 |

| Best Trade [%] | 14.15988 |

| Worst Trade [%] | 14.15988 |

| Avg. Trade [%] | 14.15988 |

| Max. Trade Duration | 308 days 00:00:00 |

| Avg. Trade Duration | 308 days 00:00:00 |

| Profit Factor | NaN |

| Expectancy [%] | 14.15988 |

| SQN | NaN |

| Kelly Criterion | NaN |

| _strategy | BreakoutStrategy(entry_n=60,exit_n=15,trailing... |

| _equity_curve | Equity DrawdownPct Drawdown... |

| _trades | Size EntryBar ExitBar EntryPrice ExitPr... |

hm = heatmap.groupby(['entry_n', 'exit_n']).mean().unstack()

hm = hm[::-1]

hm| exit_n | 5 | 10 | 15 | 20 |

|---|---|---|---|---|

| entry_n | ||||

| 120 | 0.300914 | 0.380769 | 0.411729 | 0.404996 |

| 90 | 0.283435 | 0.286116 | 0.416319 | 0.549208 |

| 60 | 0.323398 | 0.451844 | 0.573877 | 0.694695 |

| 30 | -2.478173 | -2.505373 | -2.929729 | -2.522413 |

| 15 | -1.920467 | -2.045167 | -2.291447 | -2.301150 |

| 5 | -1.969672 | -2.044275 | -1.960377 | -1.669571 |

bt_opt.plot()GridPlot(

id = 'p5439', …)

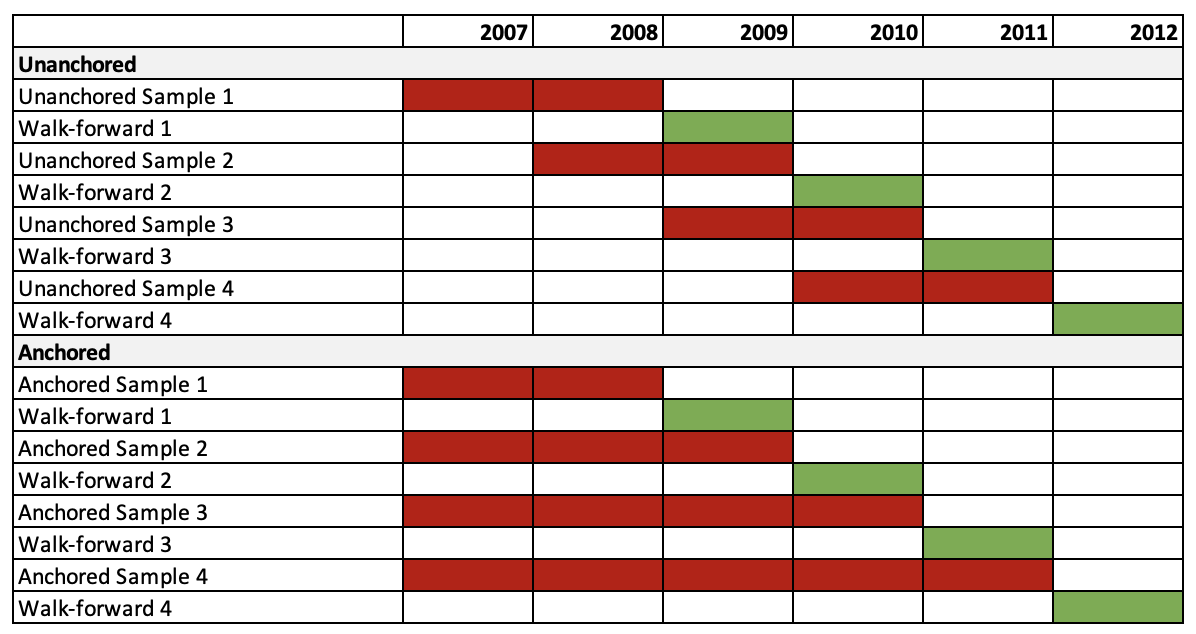

Walk-Forward test & Optimisation

Once we have passed the prelim test, then we can run the walk-forward test to confirm the robustness of the strategy. We will basically test a grid of values for the parameters that we are using in the rules.

Let’s first clarify some terminologies that we will be using in Walk-Forward Test

- In-Period

-

This is the chunk of historical data that will be optimised

- Out-Period

-

This is the chunk of historical data that will be evaluated using optimised parameters from the adjacent in-period

- Fitness Factor

-

This is the criterion used to determine the “best” result, allowing us to select the optimised parametrs

- Anchored/Unanchored test

-

This tells us whether or not the in-period start date shifts with time (Un-anchored), or if the start date is always the same (Anchored)

from strategy.utils import walk_forward, make_walkforward_report

from strategy.BreakoutStrategy import BreakoutStrategy

# Parameters to test

entry_n_parameters = [5, 15, 30, 60, 90, 120]

exit_n_parameters = [1, 3, 5, 10]

exit_rule_trialing_stop_parameters = [1, 3, 4, 99]

opt_stats, walkforward_stats = walk_forward(BreakoutStrategy,

data=SPY,

objective="Sharpe Ratio",

cash=10_000,

chunk_size=100,

training_chunk=10,

validation_chunk=5,

entry_n=entry_n_parameters,

exit_n=exit_n_parameters,

trailing_stop_atr_multiplier=exit_rule_trialing_stop_parameters){'entry_n': [5, 15, 30, 60, 90, 120], 'exit_n': [1, 3, 5, 10], 'trailing_stop_atr_multiplier': [1, 3, 4, 99]}

Training chunk 0: from 0 to 1000

Testing chunk 0: from 1000 to 1500Training chunk 1: from 500 to 1500

Testing chunk 1: from 1500 to 2000Training chunk 2: from 1000 to 2000

Testing chunk 2: from 2000 to 2500Training chunk 3: from 1500 to 2500

Testing chunk 3: from 2500 to 3000Training chunk 4: from 2000 to 3000

Testing chunk 4: from 3000 to 3500Training chunk 5: from 2500 to 3500

Testing chunk 5: from 3500 to 4000show(make_walkforward_report(opt_stats, walkforward_stats))| start | end | entry_n | exit_n | trailing_stop_atr_multiplier | Walkforward_Start | Walkforward_end | # Trades | Return [%] | Return (Ann.) [%] | Sharpe Ratio |

|---|---|---|---|---|---|---|---|---|---|---|

| Loading ITables v2.2.5 from the internet... (need help?) |

stats = make_walkforward_report(opt_stats, walkforward_stats)

walkforward_params = stats.loc[:, ["Walkforward_Start",

"Walkforward_end",

"entry_n",

"exit_n",

"trailing_stop_atr_multiplier"]]

walkforward_params| Walkforward_Start | Walkforward_end | entry_n | exit_n | trailing_stop_atr_multiplier | |

|---|---|---|---|---|---|

| 0 | 2011-12-19 | 2013-12-13 | 60 | 3 | 3 |

| 1 | 2013-12-16 | 2015-12-09 | 90 | 1 | 1 |

| 2 | 2015-12-10 | 2017-12-04 | 120 | 1 | 99 |

| 3 | 2017-12-05 | 2019-11-29 | 60 | 1 | 1 |

| 4 | 2019-12-02 | 2021-11-23 | 90 | 1 | 99 |

| 5 | 2021-11-24 | 2023-11-20 | 120 | 1 | 1 |

# Full optimisation Strategy

# Parameters to test

entry_n_parameters = [5, 15, 30, 60, 90, 120]

exit_n_parameters = [1, 3, 5, 10]

exit_rule_trialing_stop_parameters = [1, 3, 4, 99]

data = SPY

data.set_index(data.index.tz_localize(tz=None), inplace=True)

selection = data.loc["2011-12-19":]

bt_opt = Backtest(selection,

BreakoutStrategy,

cash=10_000,

finalize_trades=True)

stats_opt = bt_opt.optimize(

entry_n=entry_n_parameters,

exit_n=exit_n_parameters,

trailing_stop_atr_multiplier=exit_rule_trialing_stop_parameters,

maximize='Sharpe Ratio',

max_tries=200,

random_state=42,

return_heatmap=False)

print(stats_opt._strategy)

bt_opt = Backtest(selection,

BreakoutStrategy,

cash=10_000,

finalize_trades=True)

stats_opt = bt_opt.run(entry_n=5,

exit_n=1,

trailing_stop_atr_multiplier=99)

pd.DataFrame(stats_opt)/Users/raylai/Library/Caches/org.R-project.R/R/reticulate/uv/cache/archive-v0/n27kI_pu2kgd7cyXmF2Fh/lib/python3.11/site-packages/numpy/lib/_function_base_impl.py:552: RuntimeWarning: Mean of empty slice.

avg = a.mean(axis, **keepdims_kw)

/Users/raylai/Library/Caches/org.R-project.R/R/reticulate/uv/cache/archive-v0/n27kI_pu2kgd7cyXmF2Fh/lib/python3.11/site-packages/numpy/_core/_methods.py:137: RuntimeWarning: invalid value encountered in divide

ret = um.true_divide(

/Users/raylai/Library/Caches/org.R-project.R/R/reticulate/uv/cache/archive-v0/n27kI_pu2kgd7cyXmF2Fh/lib/python3.11/site-packages/backtesting/_stats.py:157: RuntimeWarning: Degrees of freedom <= 0 for slice

cov_matrix = np.cov(equity_log_returns, market_log_returns)

/Users/raylai/Library/Caches/org.R-project.R/R/reticulate/uv/cache/archive-v0/n27kI_pu2kgd7cyXmF2Fh/lib/python3.11/site-packages/numpy/lib/_function_base_impl.py:2894: RuntimeWarning: divide by zero encountered in divide

c *= np.true_divide(1, fact)

/Users/raylai/Library/Caches/org.R-project.R/R/reticulate/uv/cache/archive-v0/n27kI_pu2kgd7cyXmF2Fh/lib/python3.11/site-packages/numpy/lib/_function_base_impl.py:2894: RuntimeWarning: invalid value encountered in multiply

c *= np.true_divide(1, fact)

/Users/raylai/Library/Caches/org.R-project.R/R/reticulate/uv/cache/archive-v0/n27kI_pu2kgd7cyXmF2Fh/lib/python3.11/site-packages/backtesting/_plotting.py:55: UserWarning: Jupyter Notebook detected. Setting Bokeh output to notebook. This may not work in Jupyter clients without JavaScript support, such as old IDEs. Reset with `backtesting.set_bokeh_output(notebook=False)`.

warnings.warn('Jupyter Notebook detected. '

/Users/raylai/Library/Caches/org.R-project.R/R/reticulate/uv/cache/archive-v0/n27kI_pu2kgd7cyXmF2Fh/lib/python3.11/site-packages/backtesting/_plotting.py:55: UserWarning: Jupyter Notebook detected. Setting Bokeh output to notebook. This may not work in Jupyter clients without JavaScript support, such as old IDEs. Reset with `backtesting.set_bokeh_output(notebook=False)`.

warnings.warn('Jupyter Notebook detected. '

/Users/raylai/Library/Caches/org.R-project.R/R/reticulate/uv/cache/archive-v0/n27kI_pu2kgd7cyXmF2Fh/lib/python3.11/site-packages/backtesting/_plotting.py:55: UserWarning: Jupyter Notebook detected. Setting Bokeh output to notebook. This may not work in Jupyter clients without JavaScript support, such as old IDEs. Reset with `backtesting.set_bokeh_output(notebook=False)`.

warnings.warn('Jupyter Notebook detected. '

/Users/raylai/Library/Caches/org.R-project.R/R/reticulate/uv/cache/archive-v0/n27kI_pu2kgd7cyXmF2Fh/lib/python3.11/site-packages/backtesting/_plotting.py:55: UserWarning: Jupyter Notebook detected. Setting Bokeh output to notebook. This may not work in Jupyter clients without JavaScript support, such as old IDEs. Reset with `backtesting.set_bokeh_output(notebook=False)`.

warnings.warn('Jupyter Notebook detected. '

/Users/raylai/Library/Caches/org.R-project.R/R/reticulate/uv/cache/archive-v0/n27kI_pu2kgd7cyXmF2Fh/lib/python3.11/site-packages/backtesting/_plotting.py:55: UserWarning: Jupyter Notebook detected. Setting Bokeh output to notebook. This may not work in Jupyter clients without JavaScript support, such as old IDEs. Reset with `backtesting.set_bokeh_output(notebook=False)`.

warnings.warn('Jupyter Notebook detected. '

/Users/raylai/Library/Caches/org.R-project.R/R/reticulate/uv/cache/archive-v0/n27kI_pu2kgd7cyXmF2Fh/lib/python3.11/site-packages/backtesting/_plotting.py:55: UserWarning: Jupyter Notebook detected. Setting Bokeh output to notebook. This may not work in Jupyter clients without JavaScript support, such as old IDEs. Reset with `backtesting.set_bokeh_output(notebook=False)`.

warnings.warn('Jupyter Notebook detected. '

/Users/raylai/Library/Caches/org.R-project.R/R/reticulate/uv/cache/archive-v0/n27kI_pu2kgd7cyXmF2Fh/lib/python3.11/site-packages/backtesting/_plotting.py:55: UserWarning: Jupyter Notebook detected. Setting Bokeh output to notebook. This may not work in Jupyter clients without JavaScript support, such as old IDEs. Reset with `backtesting.set_bokeh_output(notebook=False)`.

warnings.warn('Jupyter Notebook detected. '

/Users/raylai/Library/Caches/org.R-project.R/R/reticulate/uv/cache/archive-v0/n27kI_pu2kgd7cyXmF2Fh/lib/python3.11/site-packages/backtesting/_plotting.py:55: UserWarning: Jupyter Notebook detected. Setting Bokeh output to notebook. This may not work in Jupyter clients without JavaScript support, such as old IDEs. Reset with `backtesting.set_bokeh_output(notebook=False)`.

warnings.warn('Jupyter Notebook detected. 'BreakoutStrategy(entry_n=5,exit_n=1,trailing_stop_atr_multiplier=99)| 0 | |

|---|---|

| Start | 2011-12-19 00:00:00 |

| End | 2025-02-27 00:00:00 |

| Duration | 4819 days 00:00:00 |

| Exposure Time [%] | 99.397046 |

| Equity Final [$] | 10491.678424 |

| Equity Peak [$] | 10507.710214 |

| Return [%] | 4.916784 |

| Buy & Hold Return [%] | 473.348476 |

| Return (Ann.) [%] | 0.365312 |

| Volatility (Ann.) [%] | 0.484519 |

| CAGR [%] | 0.251308 |

| Sharpe Ratio | 0.753969 |

| Sortino Ratio | 1.050367 |

| Calmar Ratio | 0.338704 |

| Alpha [%] | -8.036503 |

| Beta | 0.027365 |

| Max. Drawdown [%] | -1.078559 |

| Avg. Drawdown [%] | -0.044021 |

| Max. Drawdown Duration | 709 days 00:00:00 |

| Avg. Drawdown Duration | 18 days 00:00:00 |

| # Trades | 1 |

| Win Rate [%] | 100.0 |

| Best Trade [%] | 475.596319 |

| Worst Trade [%] | 475.596319 |

| Avg. Trade [%] | 475.596319 |

| Max. Trade Duration | 4788 days 00:00:00 |

| Avg. Trade Duration | 4788 days 00:00:00 |

| Profit Factor | NaN |

| Expectancy [%] | 475.596319 |

| SQN | NaN |

| Kelly Criterion | NaN |

| _strategy | BreakoutStrategy(entry_n=5,exit_n=1,trailing_s... |

| _equity_curve | Equity DrawdownPct Drawdown... |

| _trades | Size EntryBar ExitBar EntryPrice ExitP... |

Now, we have to re-code the strategy such that it adapts to the optimised walk-forward parameters. (Note: This part NEEDS to be re-factored s the current way is very inefficient)

Show the code

# Walkaway strategy for comparison

class BreakoutStrategyWalkaway(BreakoutStrategy):

def init(self):

self.highest_close_entry_5 = self.I(HighestInNBars, self.data.High, 5)

self.highest_close_entry_30 = self.I(HighestInNBars, self.data.High, 30)

self.highest_close_entry_60 = self.I(HighestInNBars, self.data.High, 60)

self.highest_close_entry_90 = self.I(HighestInNBars, self.data.High, 90)

self.lowest_close_entry_5 = self.I(LowestInNBars, self.data.Low, 5)

self.lowest_close_entry_30 = self.I(LowestInNBars, self.data.Low, 30)

self.lowest_close_entry_60 = self.I(LowestInNBars, self.data.Low, 60)

self.lowest_close_entry_90 = self.I(LowestInNBars, self.data.Low, 90)

self.highest_close_exit_1 = self.I(HighestInNBars, self.data.High, 1)

self.highest_close_exit_5 = self.I(HighestInNBars, self.data.High, 5)

self.highest_close_exit_10 = self.I(HighestInNBars, self.data.High, 10)

self.lowest_close_exit_1 = self.I(LowestInNBars, self.data.Low, 1)

self.lowest_close_exit_5 = self.I(LowestInNBars, self.data.Low, 5)

self.lowest_close_exit_10 = self.I(LowestInNBars, self.data.Low, 10)

self.atr = self.I(talib.ATR,

self.data.High,

self.data.Low,

self.data.Close,

timeperiod=14)

self.risk_unit = self.equity * self.risk_per_trade

def update_trailing_stop(self, long_exit_ind, short_exit_ind, trailing_stop_multiplier):

# Use fixed ATR trailing stop

for trade in self.trades:

if trade.is_long:

trailing_sl = long_exit_ind[-1] - trailing_stop_multiplier * self.atr[-1]

trailing_sl = max(trailing_sl, 0)

trade.sl = max(trade.sl, trailing_sl)

else: # short

trailing_sl = short_exit_ind[-1] + trailing_stop_multiplier * self.atr[-1]

trailing_sl = max(trailing_sl, 0)

trade.sl = min(trade.sl, trailing_sl)

def next(self):

long_entry_ind = None

if (self.data.index[-1] < pd.Timestamp("2013-12-13")):

long_entry_ind = self.highest_close_entry_90

elif (self.data.index[-1] < pd.Timestamp("2015-12-09")):

long_entry_ind = self.highest_close_entry_90

elif (self.data.index[-1] < pd.Timestamp("2017-12-04")):

long_entry_ind = self.highest_close_entry_30

elif (self.data.index[-1] < pd.Timestamp("2019-11-29")):

long_entry_ind = self.highest_close_entry_5

elif (self.data.index[-1] < pd.Timestamp("2021-11-23")):

long_entry_ind = self.highest_close_entry_90

elif (self.data.index[-1] < pd.Timestamp("2023-11-20")):

long_entry_ind = self.highest_close_entry_60

else:

long_entry_ind = self.highest_close_entry_60

short_entry_ind = None

if (self.data.index[-1] < pd.Timestamp("2013-12-13")):

short_entry_ind = self.highest_close_entry_90

elif (self.data.index[-1] < pd.Timestamp("2015-12-09")):

short_entry_ind = self.highest_close_entry_90

elif (self.data.index[-1] < pd.Timestamp("2017-12-04")):

short_entry_ind = self.highest_close_entry_30

elif (self.data.index[-1] < pd.Timestamp("2019-11-29")):

short_entry_ind = self.highest_close_entry_5

elif (self.data.index[-1] < pd.Timestamp("2021-11-23")):

short_entry_ind = self.highest_close_entry_90

elif (self.data.index[-1] < pd.Timestamp("2023-11-20")):

short_entry_ind = self.highest_close_entry_60

else:

short_entry_ind = self.highest_close_entry_60

long_exit_ind = None

if (self.data.index[-1] < pd.Timestamp("2013-12-13")):

long_exit_ind = self.lowest_close_exit_1

elif (self.data.index[-1] < pd.Timestamp("2015-12-09")):

long_exit_ind = self.lowest_close_exit_5

elif (self.data.index[-1] < pd.Timestamp("2017-12-04")):

long_exit_ind = self.lowest_close_exit_1

elif (self.data.index[-1] < pd.Timestamp("2019-11-29")):

long_exit_ind = self.lowest_close_exit_10

elif (self.data.index[-1] < pd.Timestamp("2021-11-23")):

long_exit_ind = self.lowest_close_exit_5

elif (self.data.index[-1] < pd.Timestamp("2023-11-20")):

long_exit_ind = self.lowest_close_exit_5

else:

long_exit_ind = self.lowest_close_exit_5

short_exit_ind = None

if (self.data.index[-1] < pd.Timestamp("2013-12-13")):

short_exit_ind = self.lowest_close_exit_1

elif (self.data.index[-1] < pd.Timestamp("2015-12-09")):

short_exit_ind = self.lowest_close_exit_5

elif (self.data.index[-1] < pd.Timestamp("2017-12-04")):

short_exit_ind = self.lowest_close_exit_1

elif (self.data.index[-1] < pd.Timestamp("2019-11-29")):

short_exit_ind = self.lowest_close_exit_10

elif (self.data.index[-1] < pd.Timestamp("2021-11-23")):

short_exit_ind = self.lowest_close_exit_5

elif (self.data.index[-1] < pd.Timestamp("2023-11-20")):

short_exit_ind = self.lowest_close_exit_5

else:

short_exit_ind = self.lowest_close_exit_5

trailing_stop_multiplier = None

if (self.data.index[-1] < pd.Timestamp("2013-12-13")):

trailing_stop_multiplier = 4

elif (self.data.index[-1] < pd.Timestamp("2015-12-09")):

trailing_stop_multiplier = 99

elif (self.data.index[-1] < pd.Timestamp("2017-12-04")):

trailing_stop_multiplier = 99

elif (self.data.index[-1] < pd.Timestamp("2019-11-29")):

trailing_stop_multiplier = 99

elif (self.data.index[-1] < pd.Timestamp("2021-11-23")):

trailing_stop_multiplier = 4

elif (self.data.index[-1] < pd.Timestamp("2023-11-20")):

trailing_stop_multiplier = 4

else:

trailing_stop_multiplier = 4

assert long_entry_ind is not None

assert short_entry_ind is not None

assert long_exit_ind is not None

assert short_exit_ind is not None

assert trailing_stop_multiplier is not None

if not self.position:

# Get entry price - Entry at market

last_close = self.data.Close[-1]

last_atr = self.atr[-1]

if last_close > long_entry_ind[-1]:

initial_sl = long_exit_ind[-1] - self.initial_stop_atr_multiplier * last_atr

initial_sl = max(0, initial_sl)

size = self.get_position_size(last_close, initial_sl)

# size = 1

tp = self.get_tp_level(last_close, size, 2)

if (initial_sl > 0 and tp > 0):

order = self.buy(size=size, sl=initial_sl)

elif last_close > short_entry_ind[-1] == -1:

initial_sl = short_exit_ind[-1] + self.initial_stop_atr_multiplier * last_atr

initial_sl = max(0, initial_sl)

size = self.get_position_size(last_close, initial_sl)

# size = 1

tp = self.get_tp_level(last_close, size, False, 2)

if (initial_sl > 0 and tp > 0 and initial_sl > last_close):

order = self.sell(size=size, sl=initial_sl)

else:

self.update_trailing_stop(long_exit_ind, short_exit_ind, trailing_stop_multiplier)

if self.exit_rule() == 1:

self.position.close()data = SPY

data.set_index(data.index.tz_localize(tz=None), inplace=True)

selection = data.loc["2011-12-19":]

bt = Backtest(selection,

BreakoutStrategyWalkaway,

cash=10_000,

finalize_trades=True)

stats = bt.run()

pd.DataFrame(stats)| 0 | |

|---|---|

| Start | 2011-12-19 00:00:00 |

| End | 2025-02-27 00:00:00 |

| Duration | 4819 days 00:00:00 |

| Exposure Time [%] | 66.716913 |

| Equity Final [$] | 20280.917357 |

| Equity Peak [$] | 20710.199932 |

| Return [%] | 102.809174 |

| Buy & Hold Return [%] | 427.013937 |

| Return (Ann.) [%] | 5.518872 |

| Volatility (Ann.) [%] | 9.025592 |

| CAGR [%] | 3.766826 |

| Sharpe Ratio | 0.611469 |

| Sortino Ratio | 0.895833 |

| Calmar Ratio | 0.303781 |

| Alpha [%] | -31.782907 |

| Beta | 0.315194 |

| Max. Drawdown [%] | -18.16725 |

| Avg. Drawdown [%] | -1.205641 |

| Max. Drawdown Duration | 931 days 00:00:00 |

| Avg. Drawdown Duration | 31 days 00:00:00 |

| # Trades | 13 |

| Win Rate [%] | 53.846154 |

| Best Trade [%] | 99.228841 |

| Worst Trade [%] | -8.066754 |

| Avg. Trade [%] | 6.723912 |

| Max. Trade Duration | 2254 days 00:00:00 |

| Avg. Trade Duration | 247 days 00:00:00 |

| Profit Factor | 6.025399 |

| Expectancy [%] | 9.102068 |

| SQN | 1.164099 |

| Kelly Criterion | 0.473604 |

| _strategy | BreakoutStrategyWalkaway |

| _equity_curve | Equity DrawdownPct Drawdown... |

| _trades | Size EntryBar ExitBar EntryPrice Exit... |

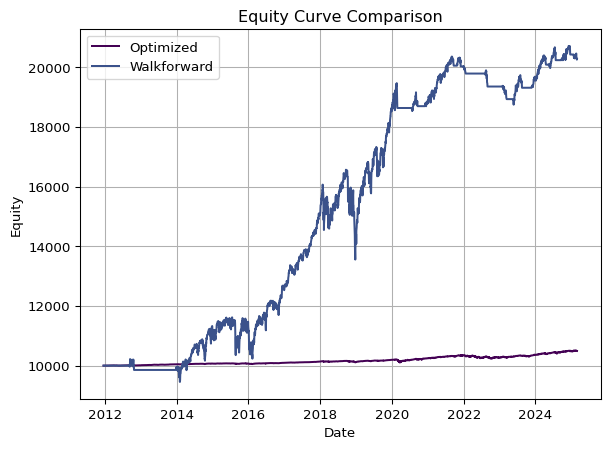

We can see the difference between the most optimised equity curve and the walk-forward equity curve

from strategy.utils import plot_equity_curves

plot_equity_curves(stats_opt._equity_curve, stats._equity_curve,

labels=["Optimized", "Walkforward"])

stats_opt.loc["Win Rate [%]"]100.0| Win Rate | Expectancy | Return % | Sharpe ratio | |

|---|---|---|---|---|

| Optimised | 100.000000 | 475.596319 | 4.916784 | 0.753969 |

| Walkforward | 53.846154 | 9.102068 | 102.809174 | 0.611469 |

Note: This is a weird result because of the position sizing algorithm. Since the most optimised trade in terms of sharpe ratio is to buy and hold, hence there is only 1 trade, and only 1% of capital is committed at entry.

Therefore, it is better to compare the expectancy instead of the equity curve, but the function itself is correct.

Learnings

Setting up this template with all the robust test is kind of a pain. Here are still some areas need to be improved

In prelim test, there are still to many code to change. Need to further re-factor.

In walk-forward test, to compute the walk-forward equity curve, it is too complicated and involved too many extra coding. Need to find a way to embed the date-wise parameters into the original class

Position sizing algorithm - This gives wrong results in equity curve comparison. From Kevin Davey’s book Ch16, he mentioned at the beginning of strategy development, he always use single contract / single unit entry to make sure the strategies are comparable.

As of now, we will end here. For the next step, I will start to work on the trending strategy with what we have here, and to smoothen the steps bit by bit.