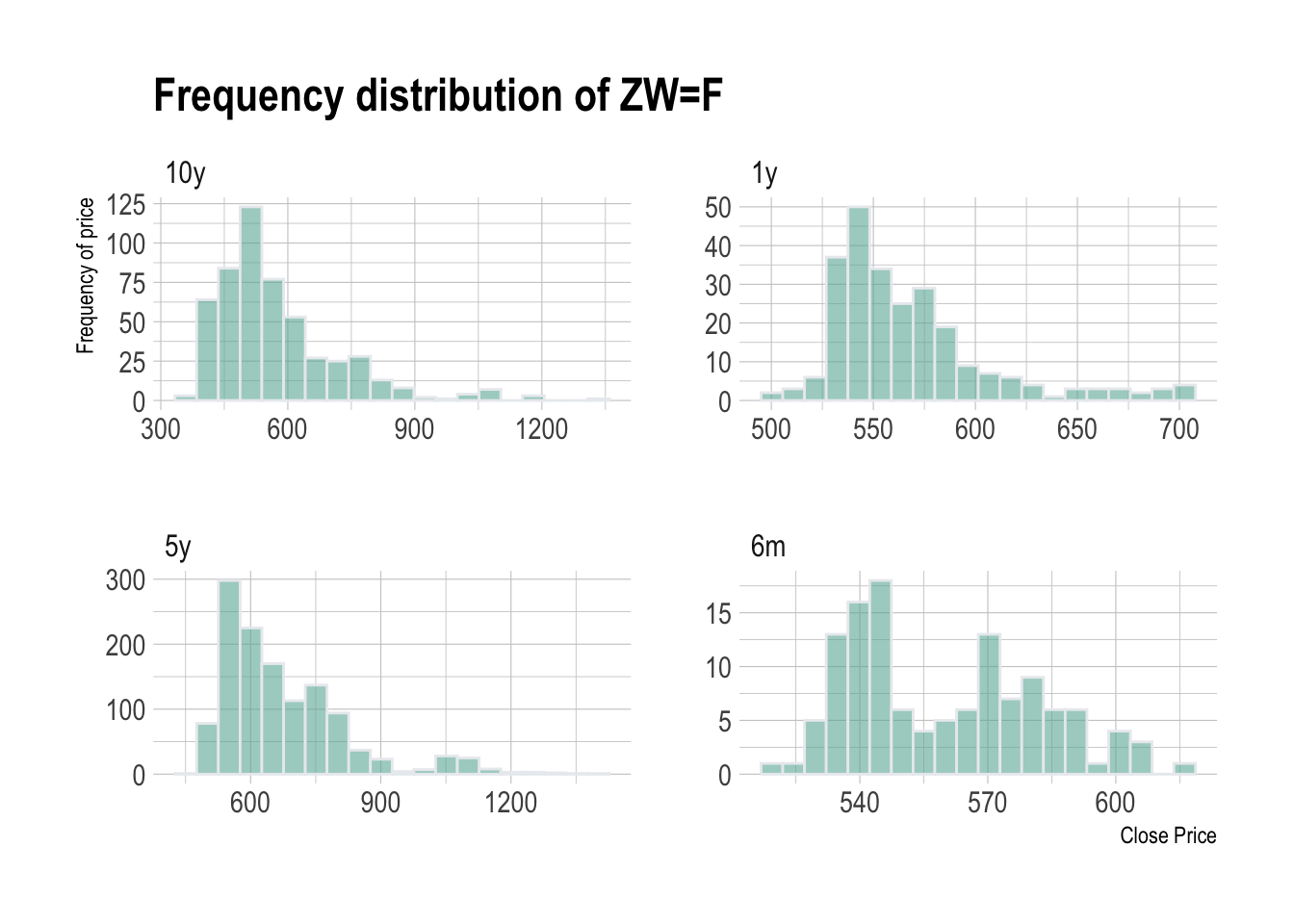

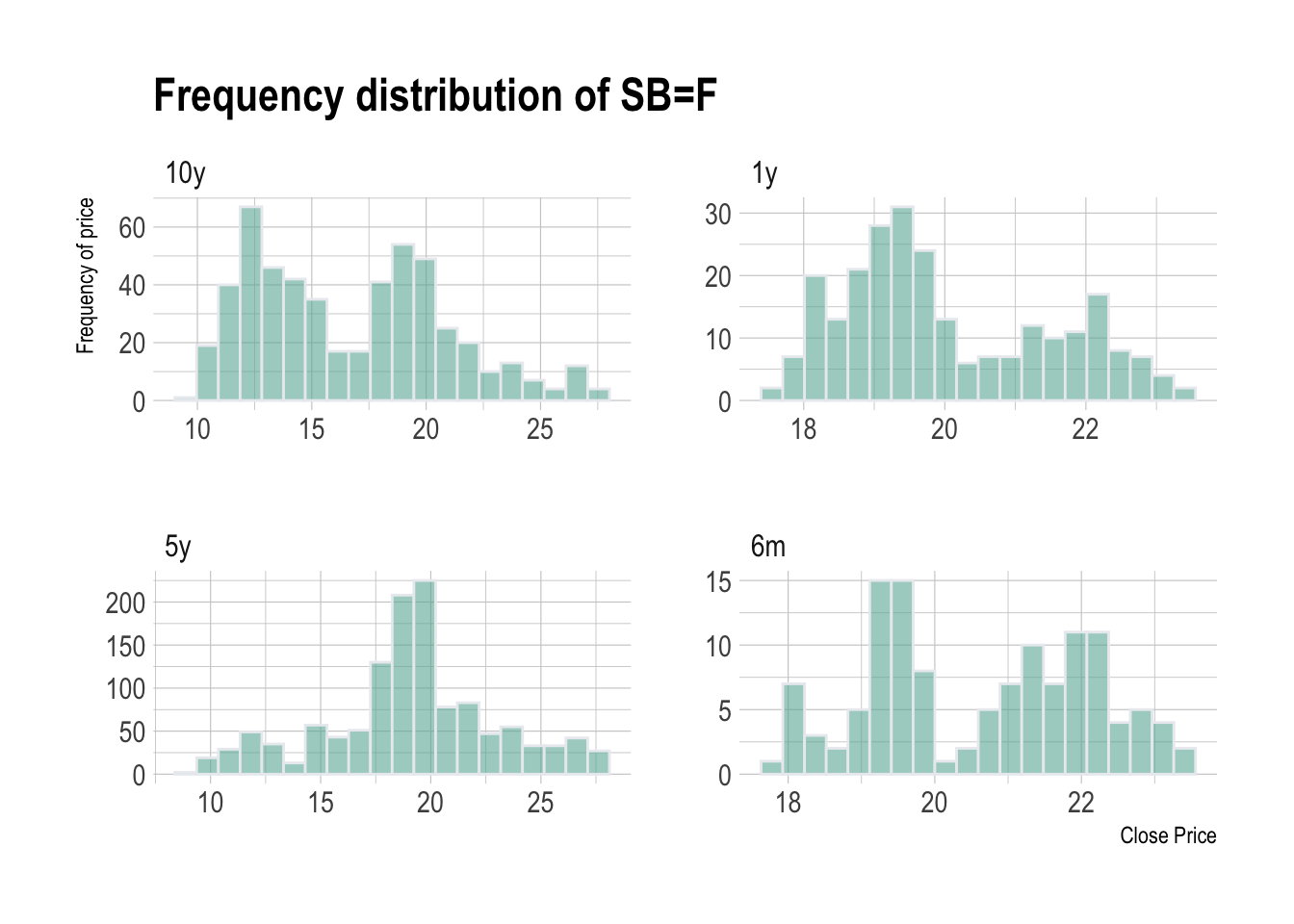

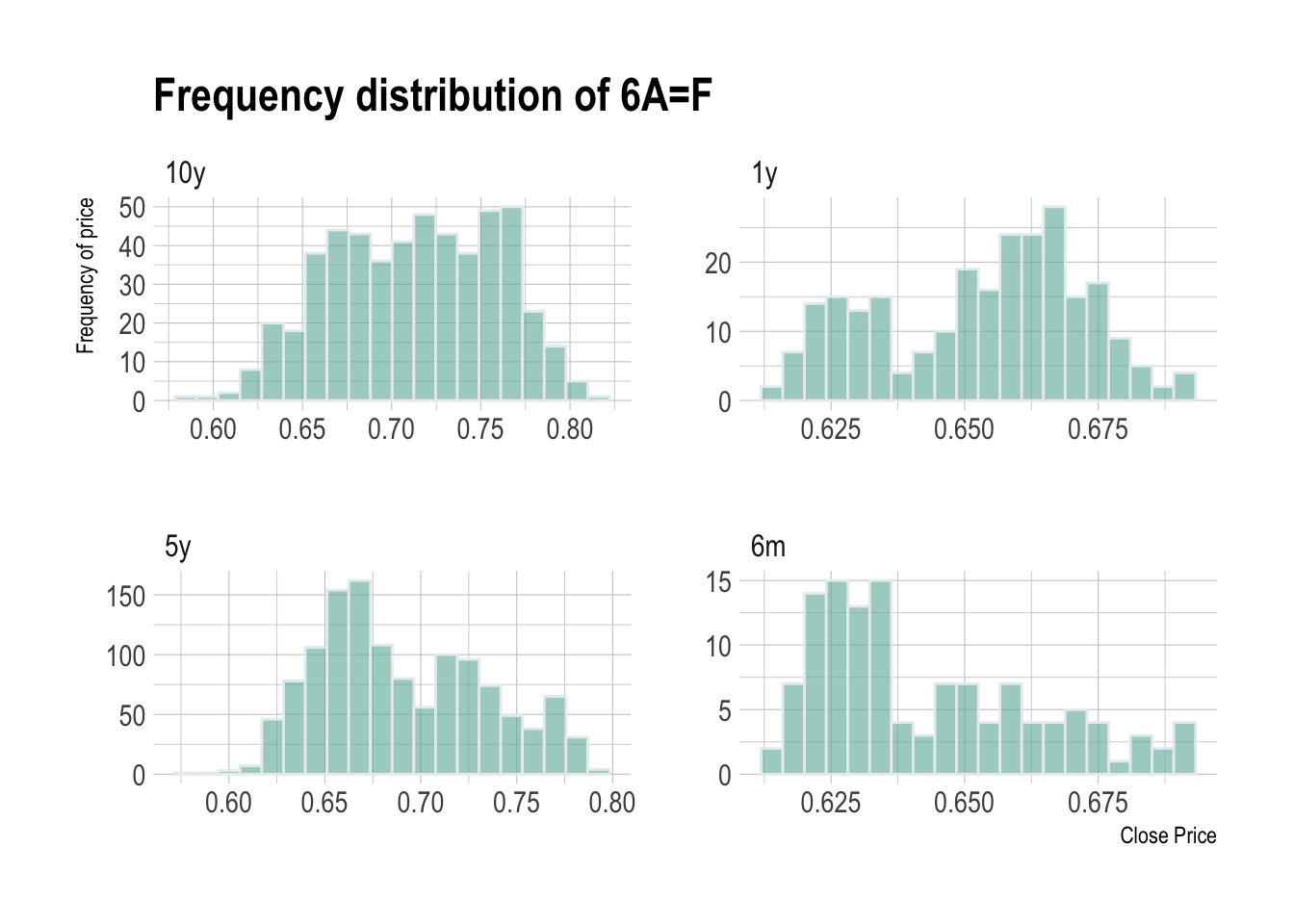

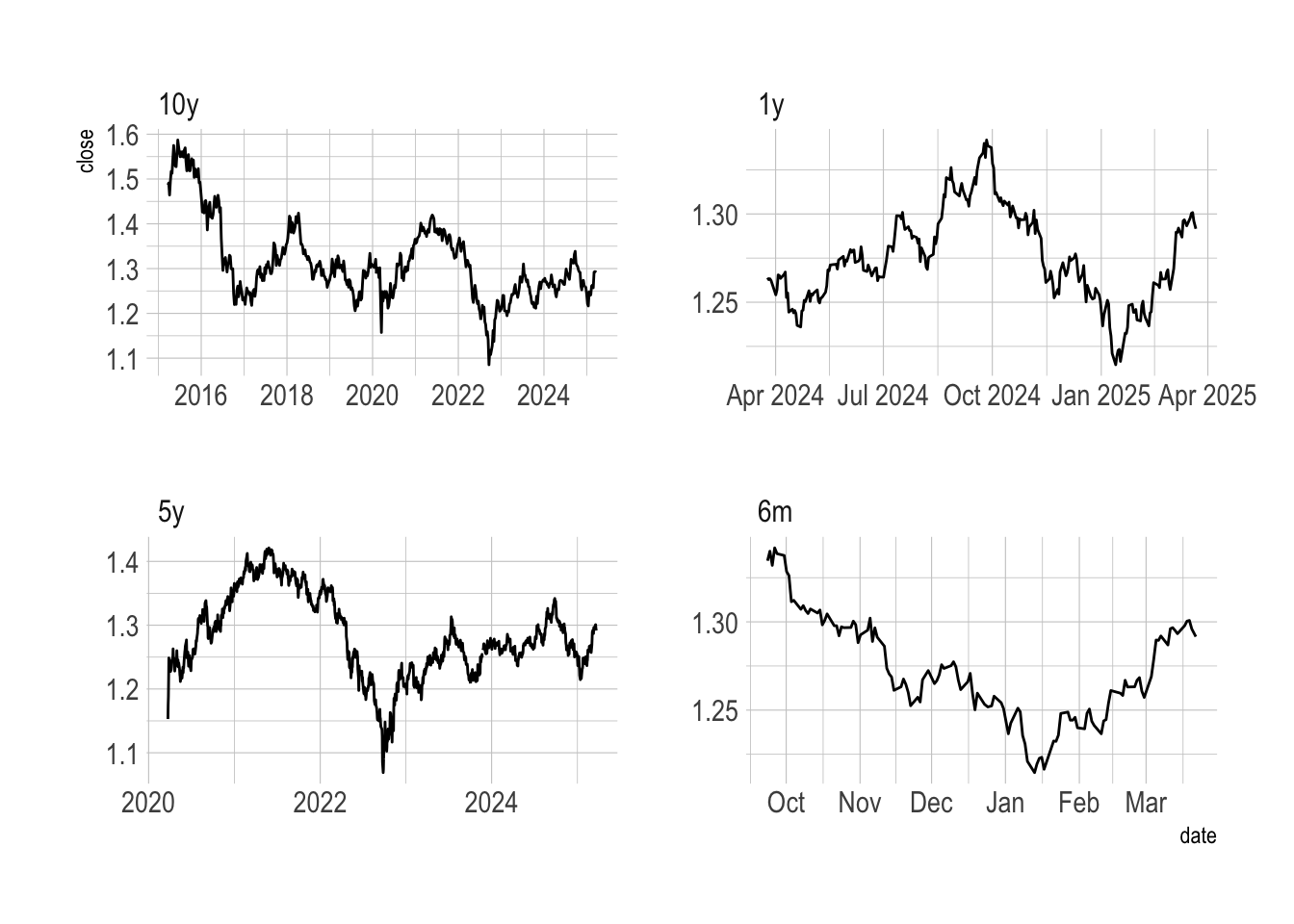

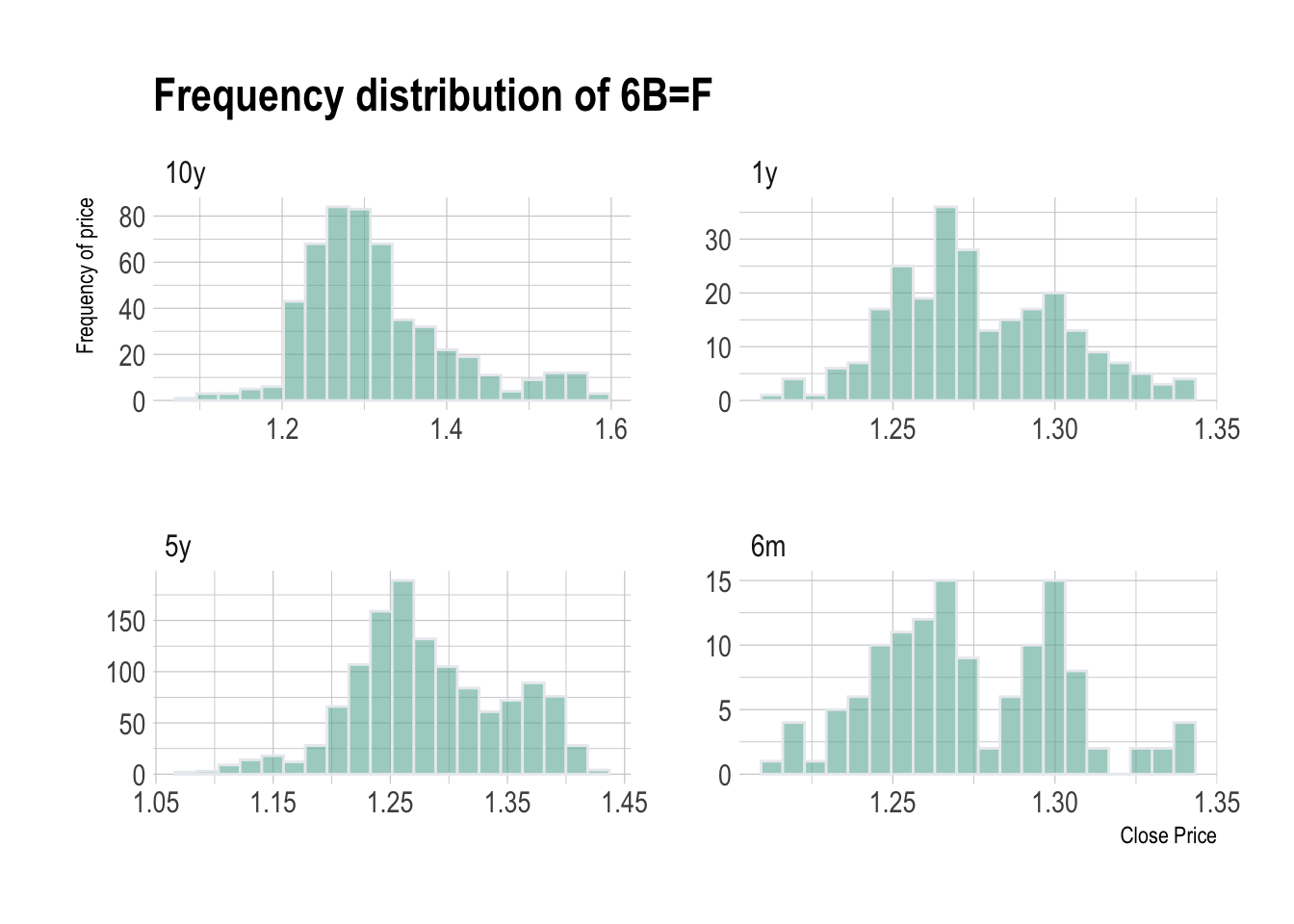

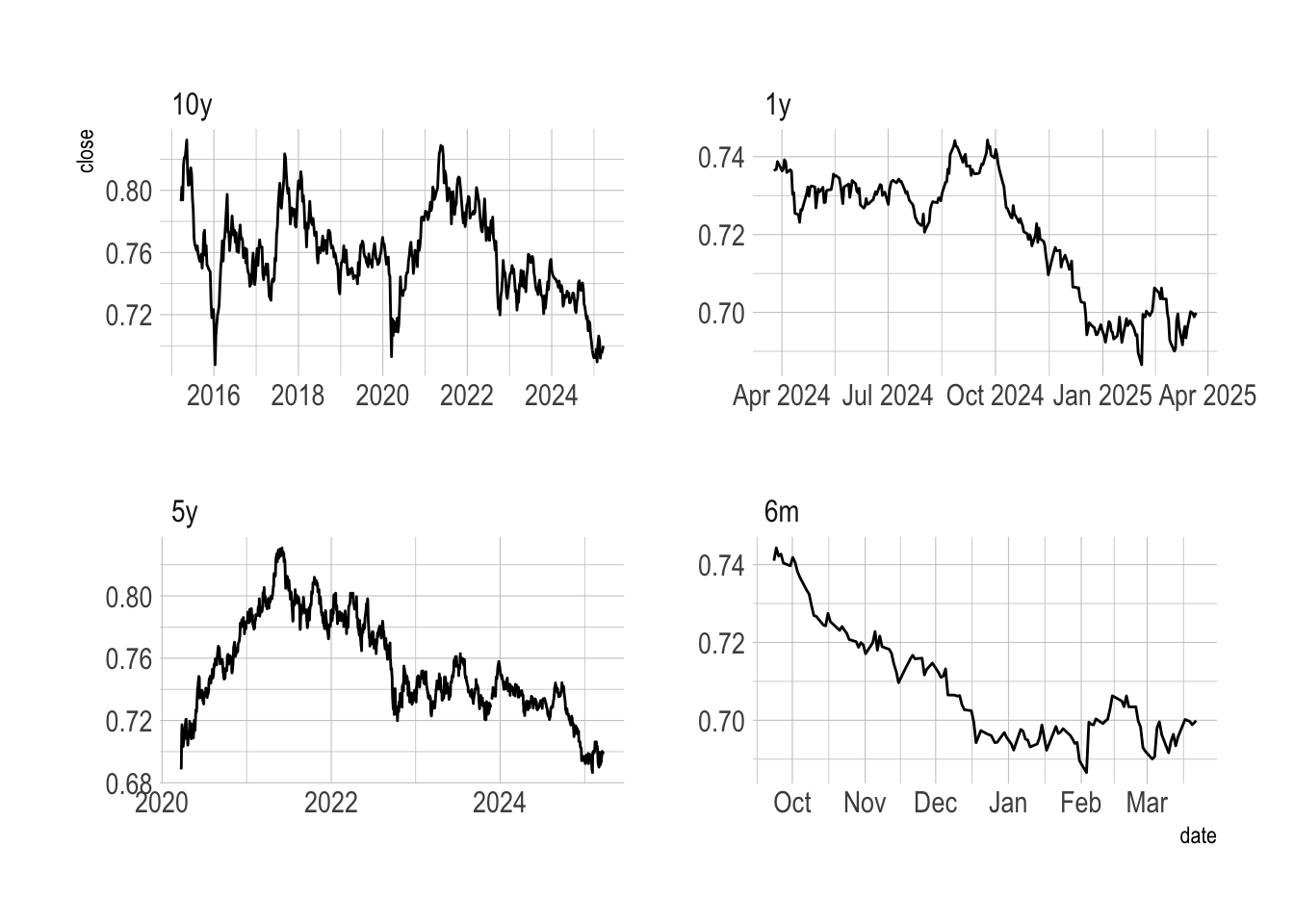

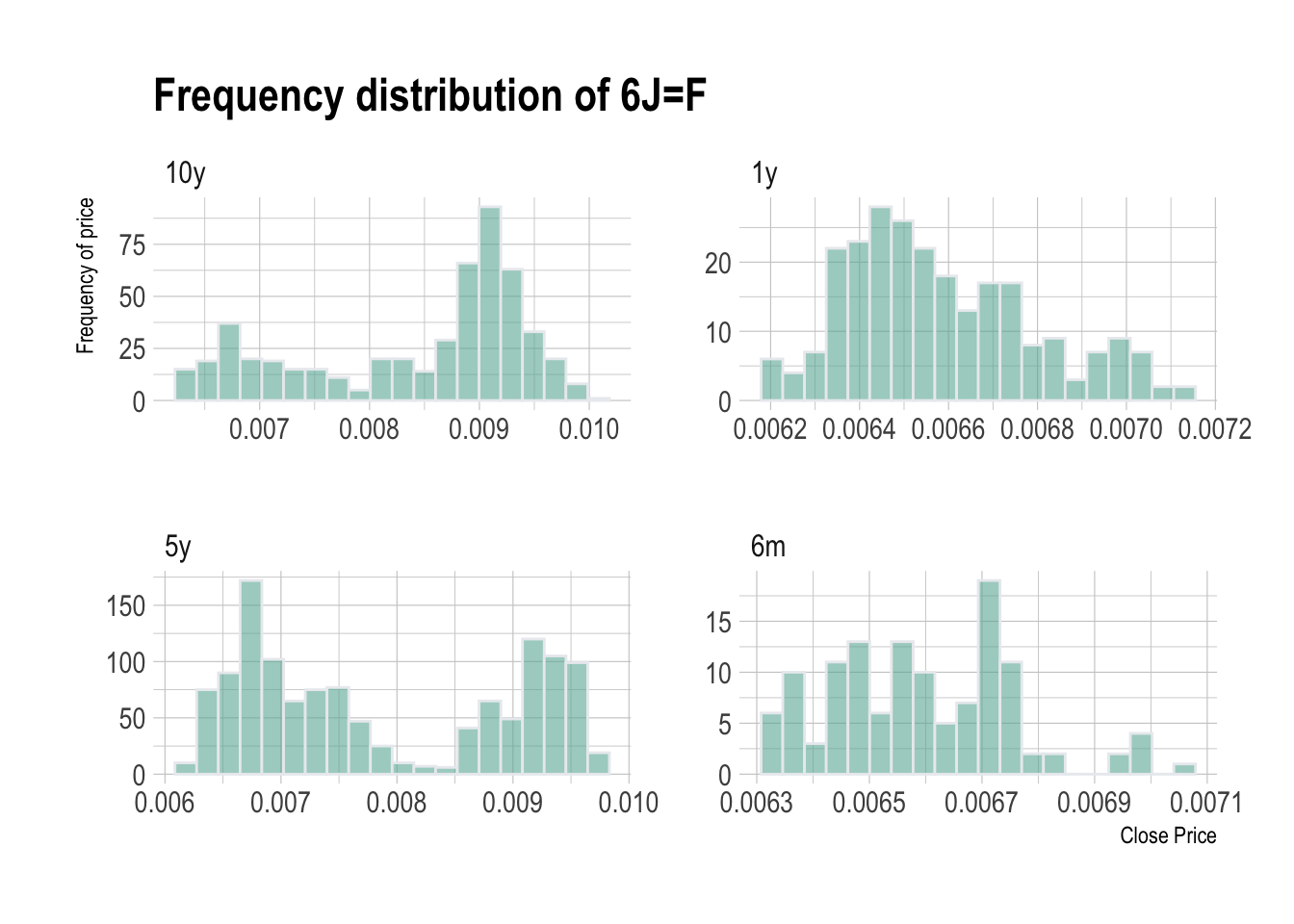

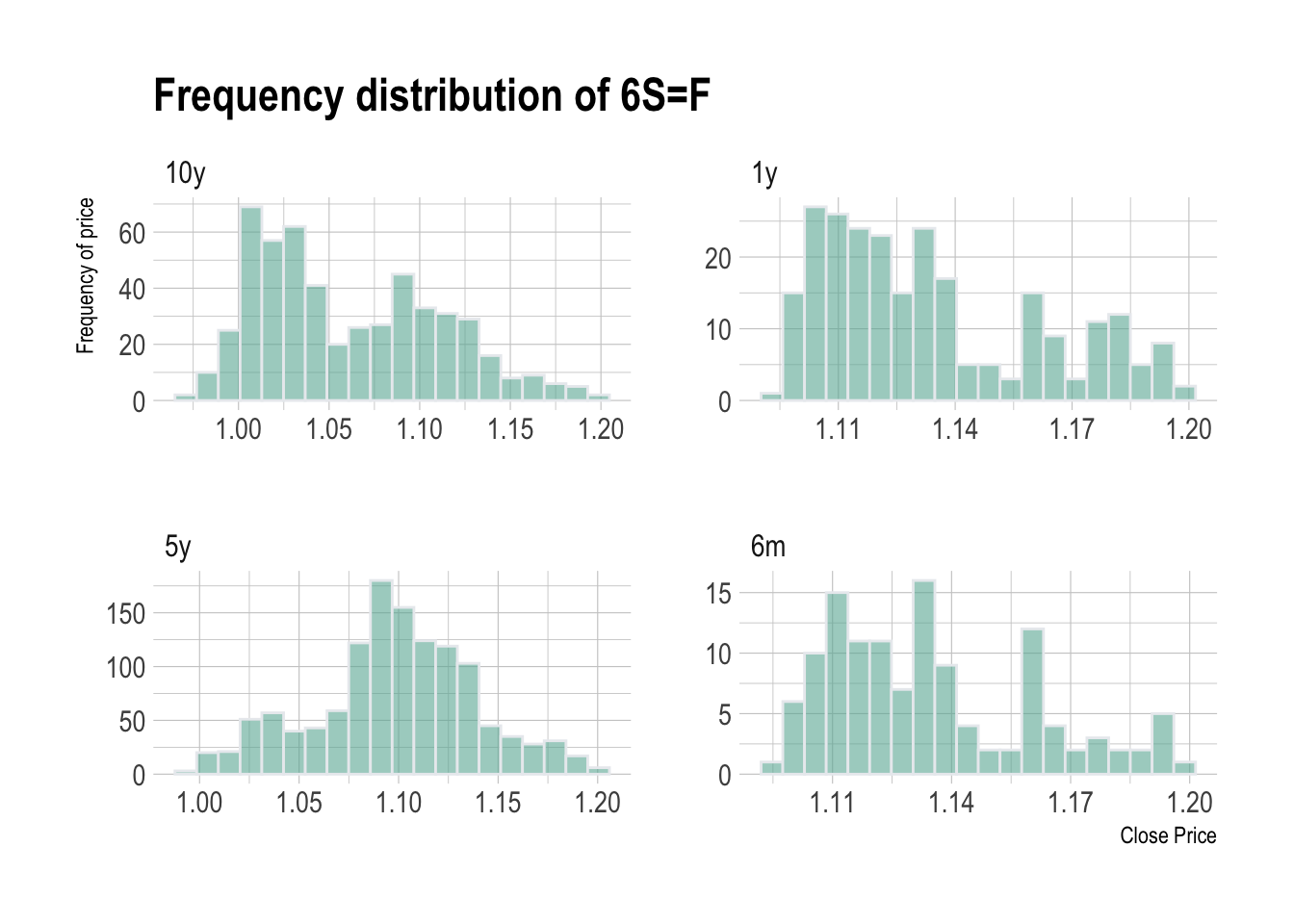

1 Understanding distribution of price of Selected ETFs

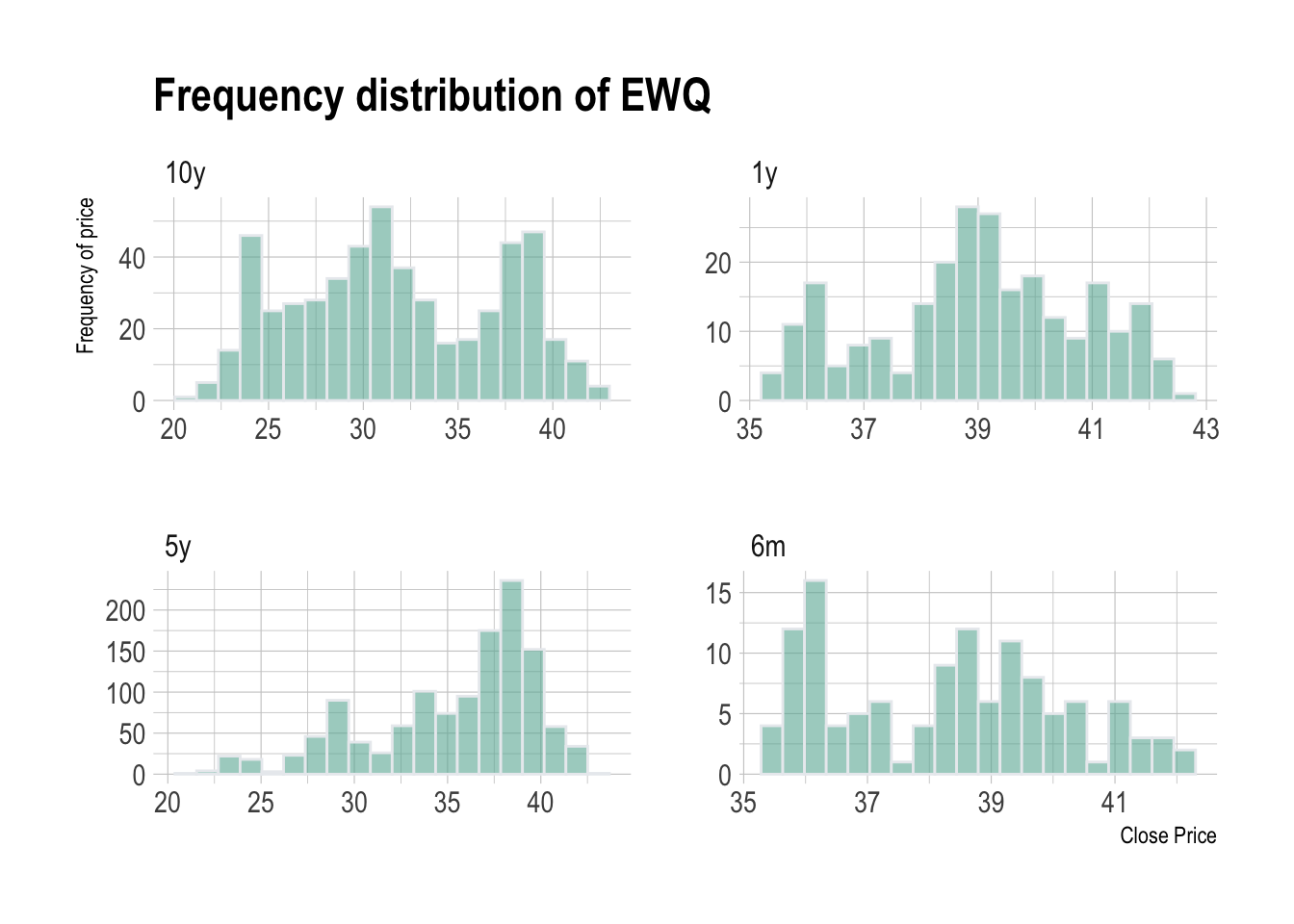

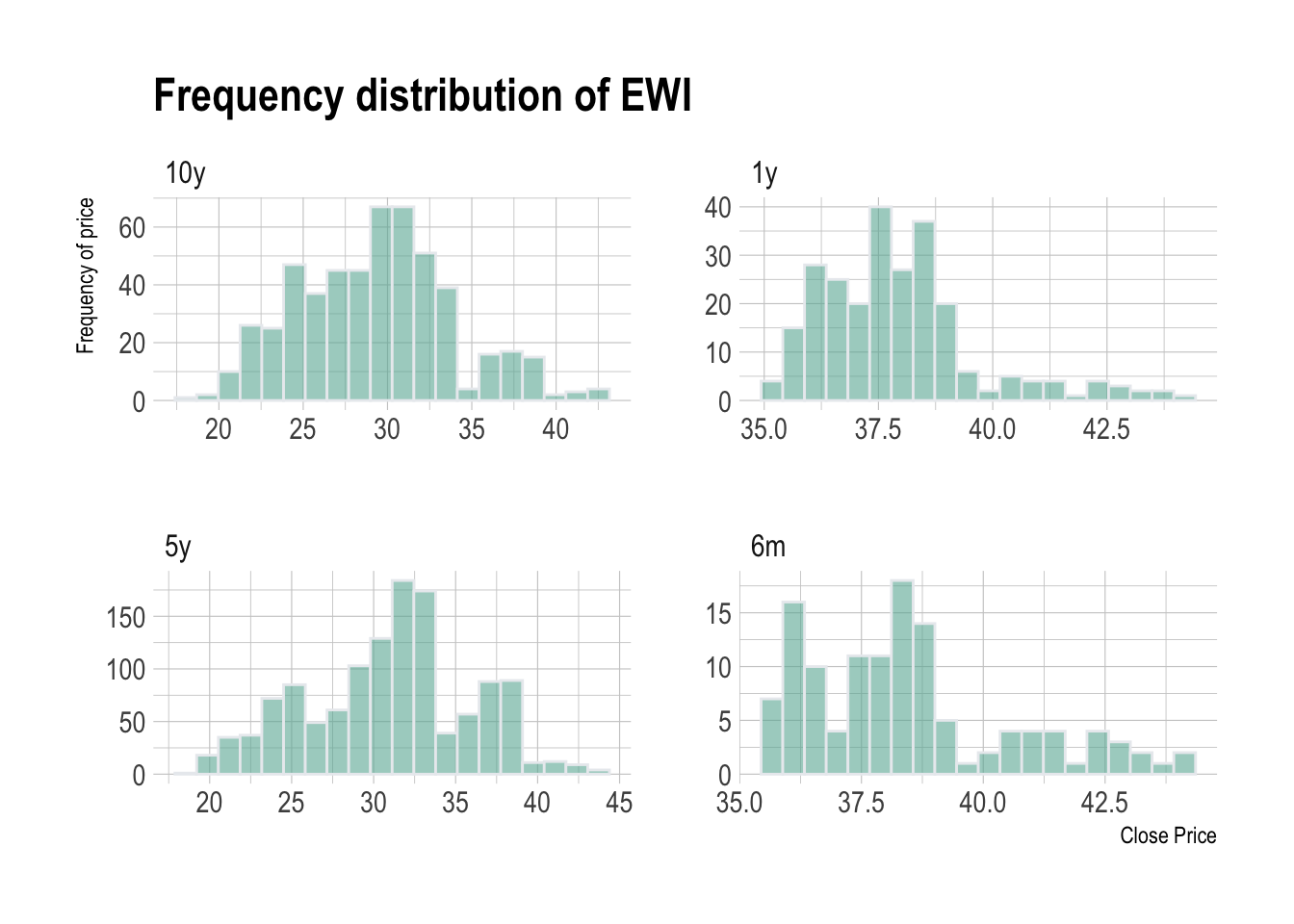

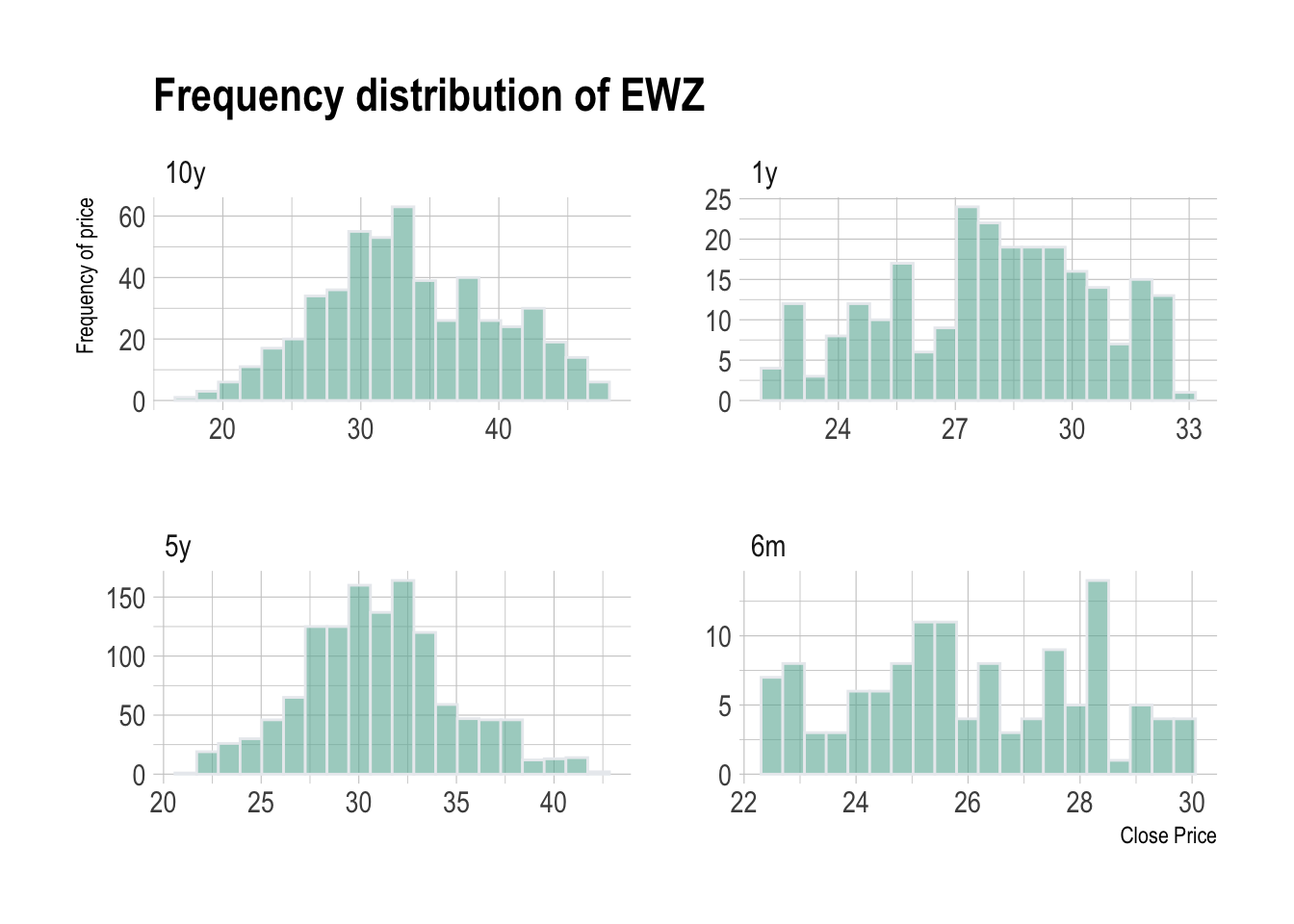

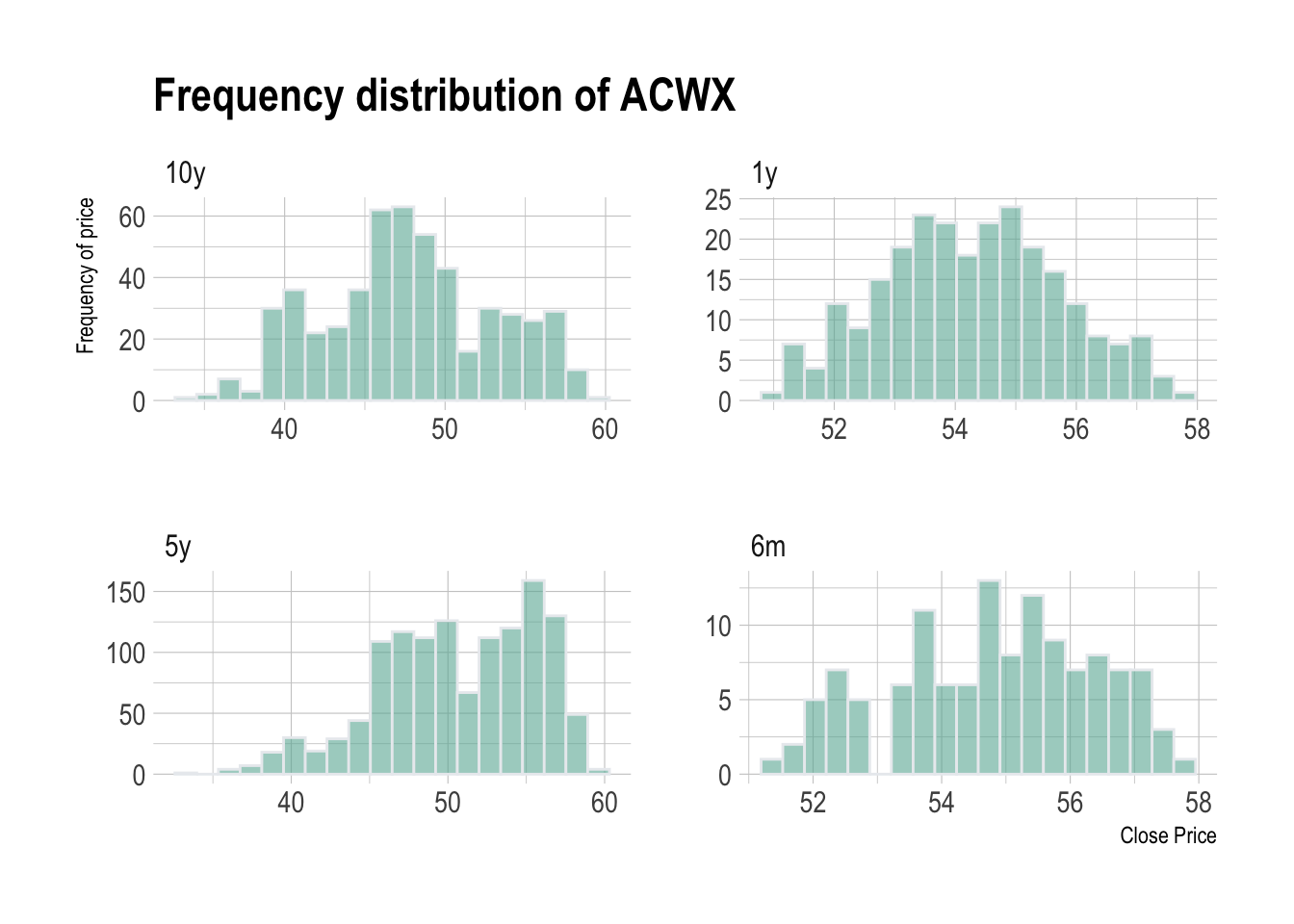

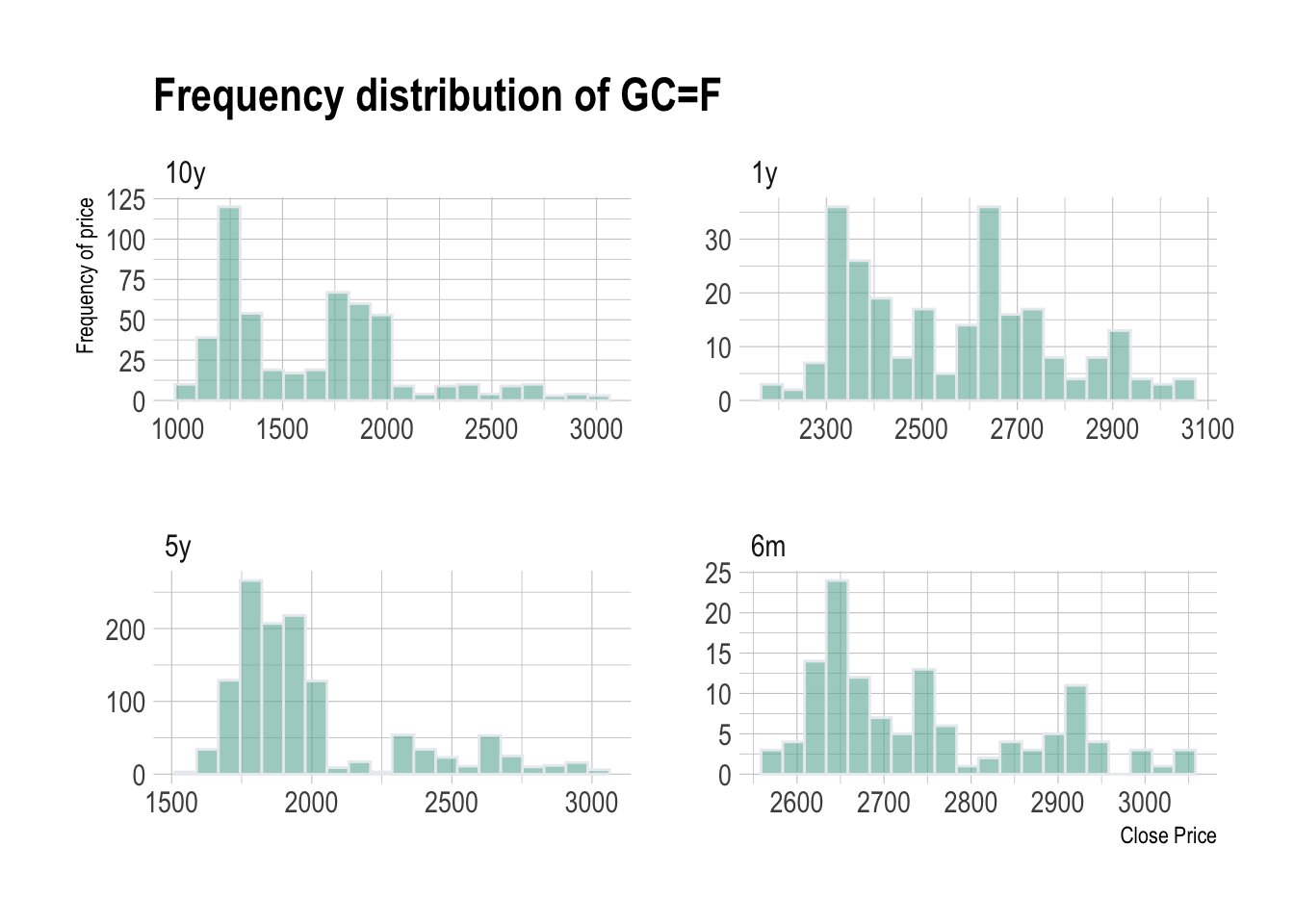

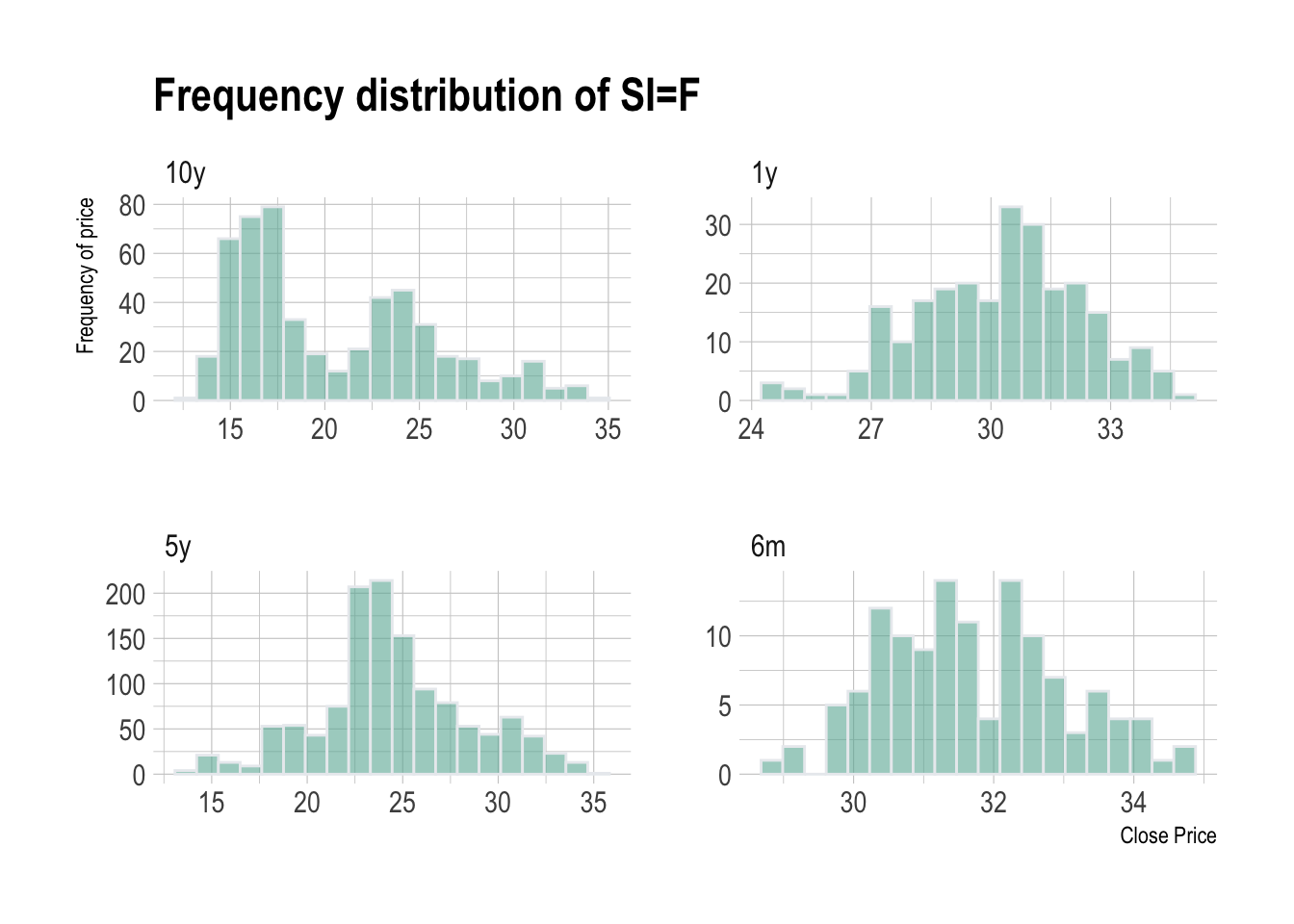

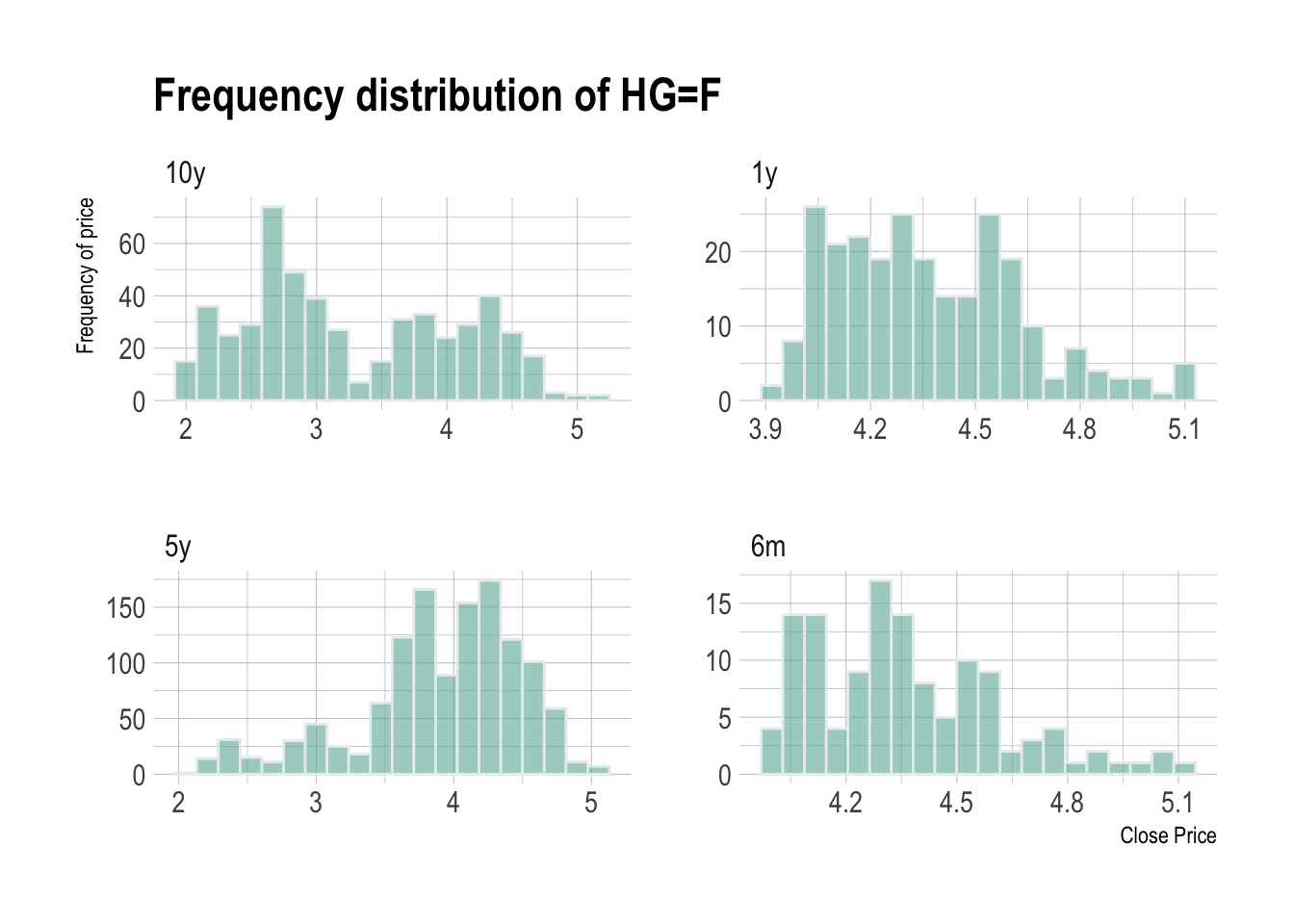

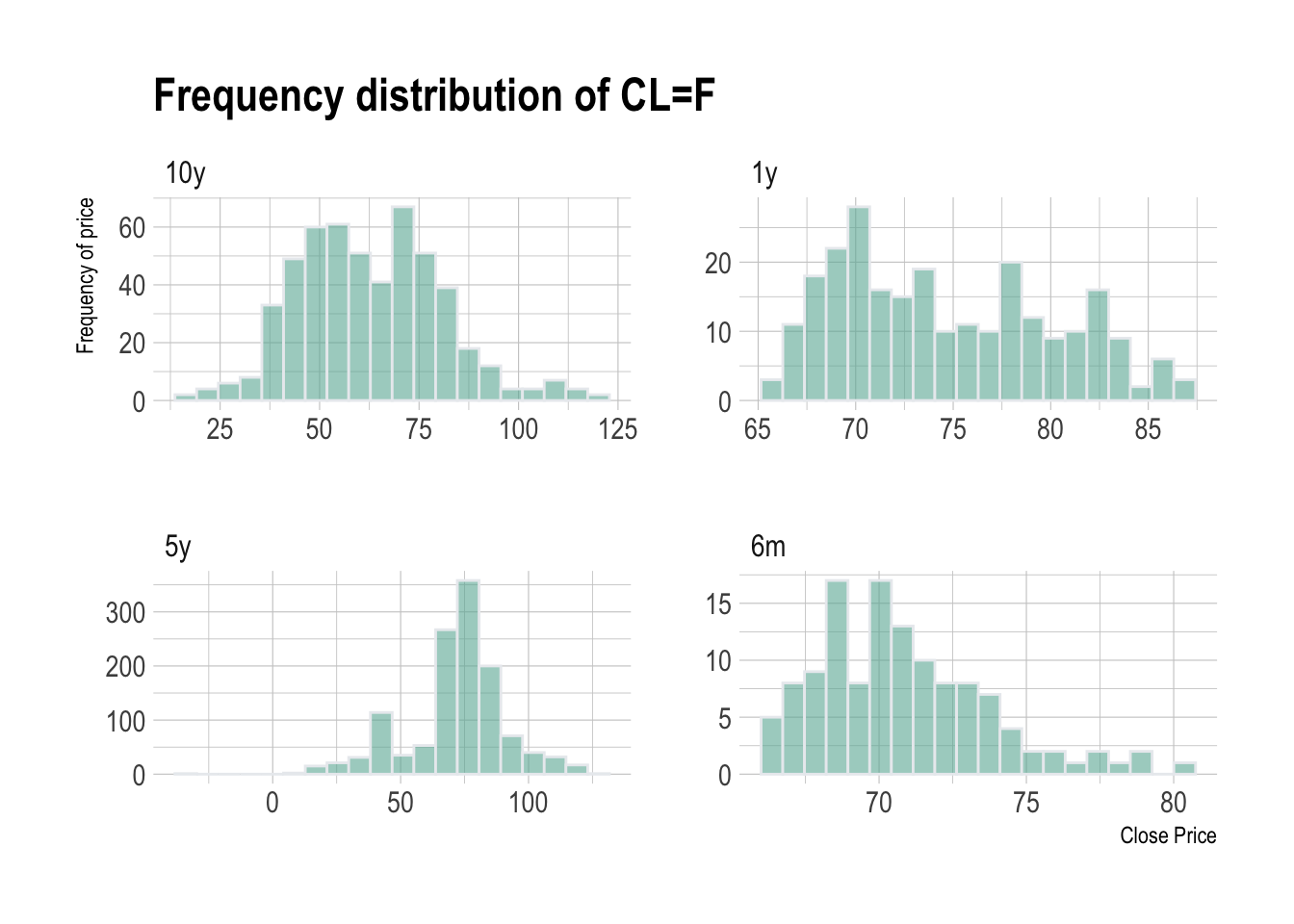

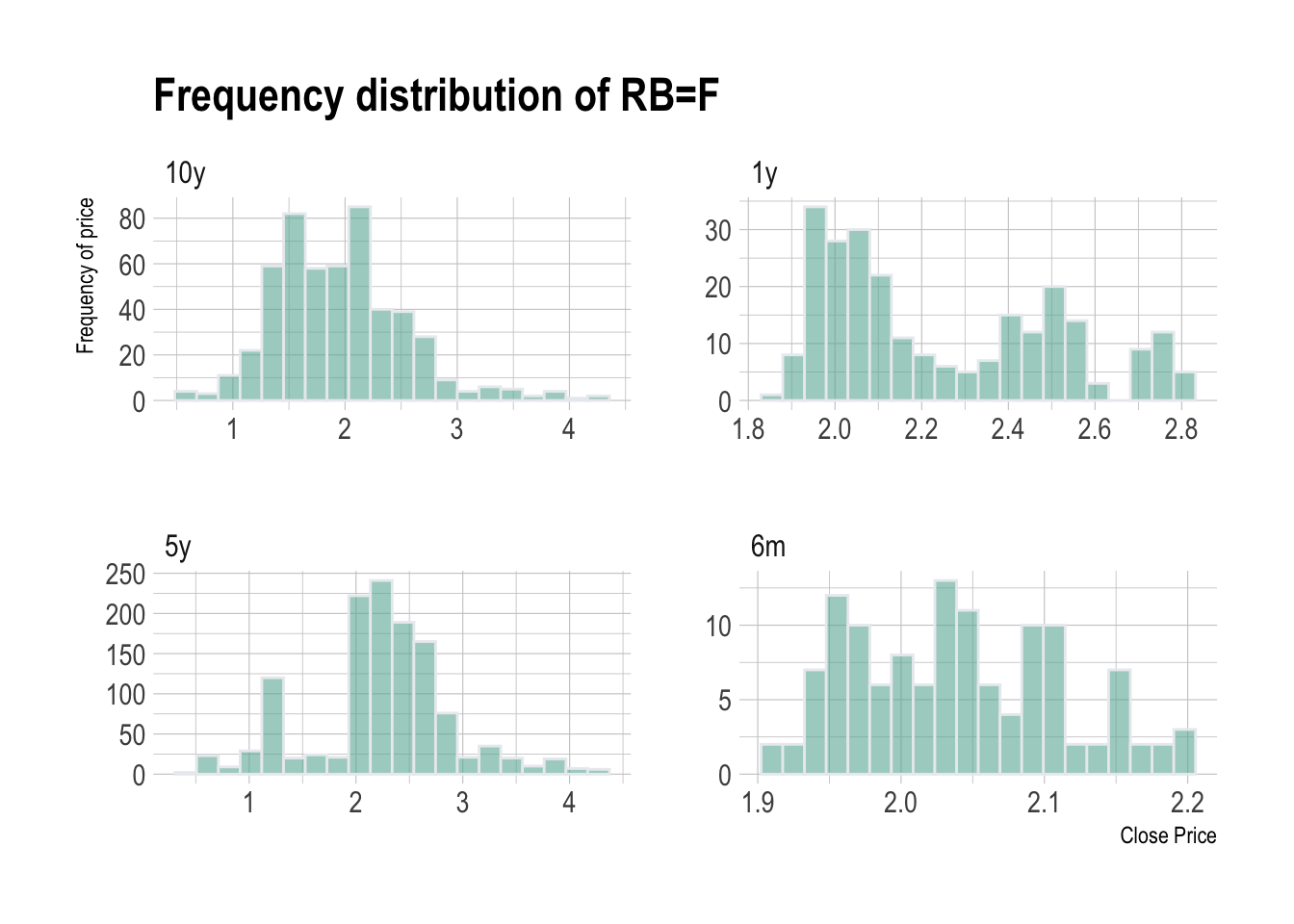

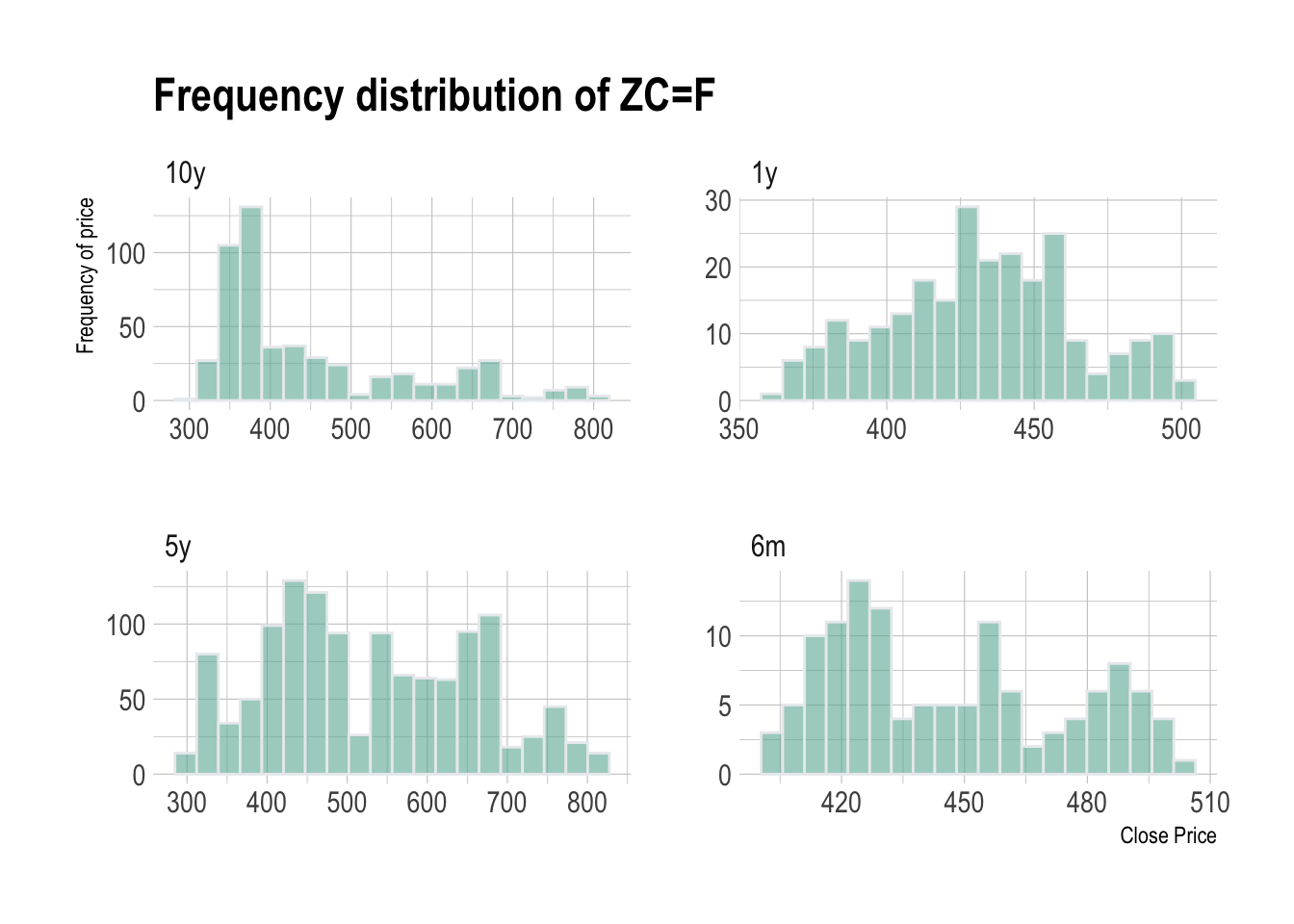

The measurement of distribution of price is very important in price analysis, as it can tell us at what range the asset class is trading with certain confidence interval. We can also examine whether the market is range-bound or trending by examining the skewness of the distribution.

The objective of doing price distribution analysis is to know what to expect.

If QQQ today is $500, we would have a higher level of confidence that it will fall between $200 to $700, but less confidence that it will fall $400 to $600.

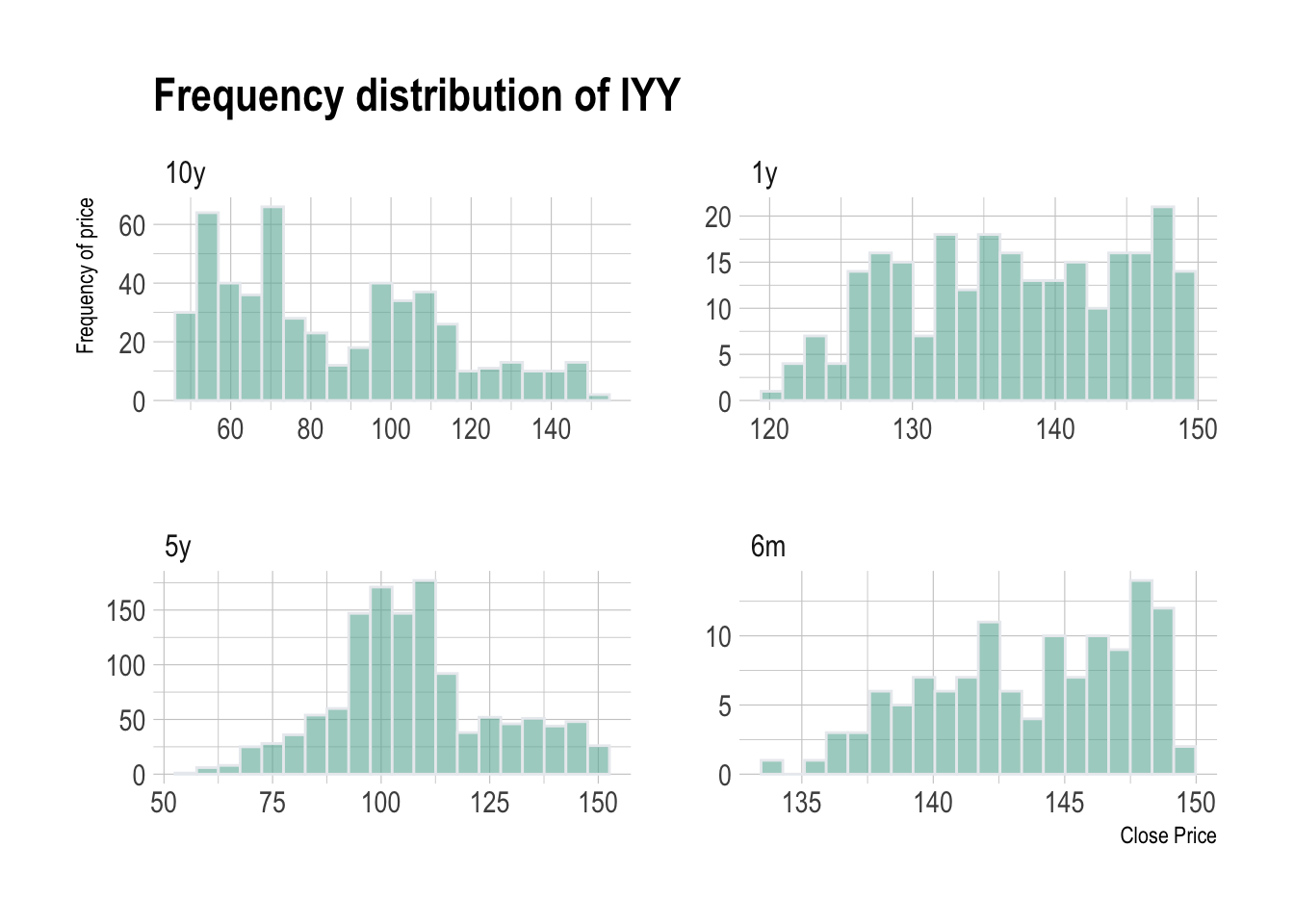

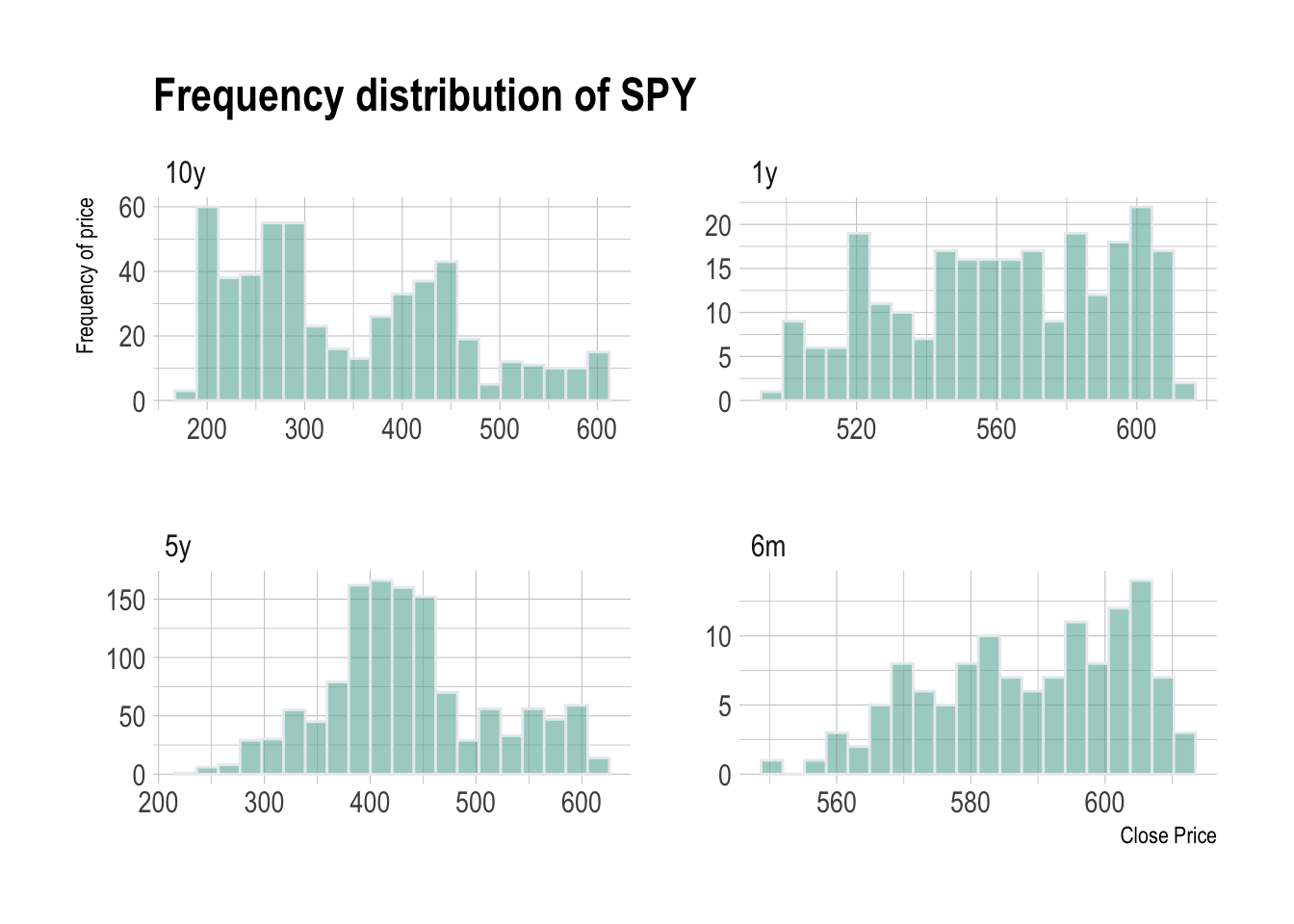

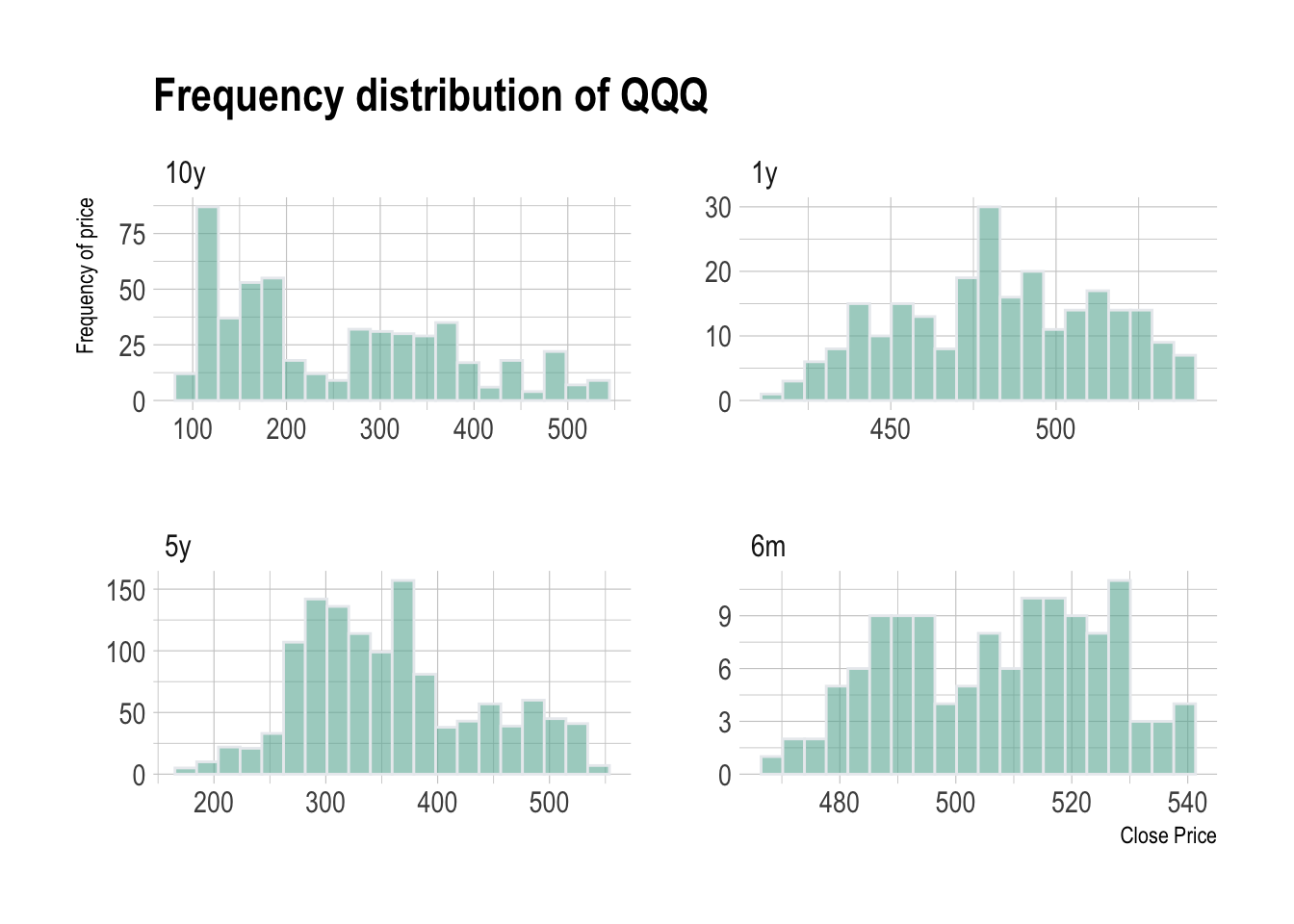

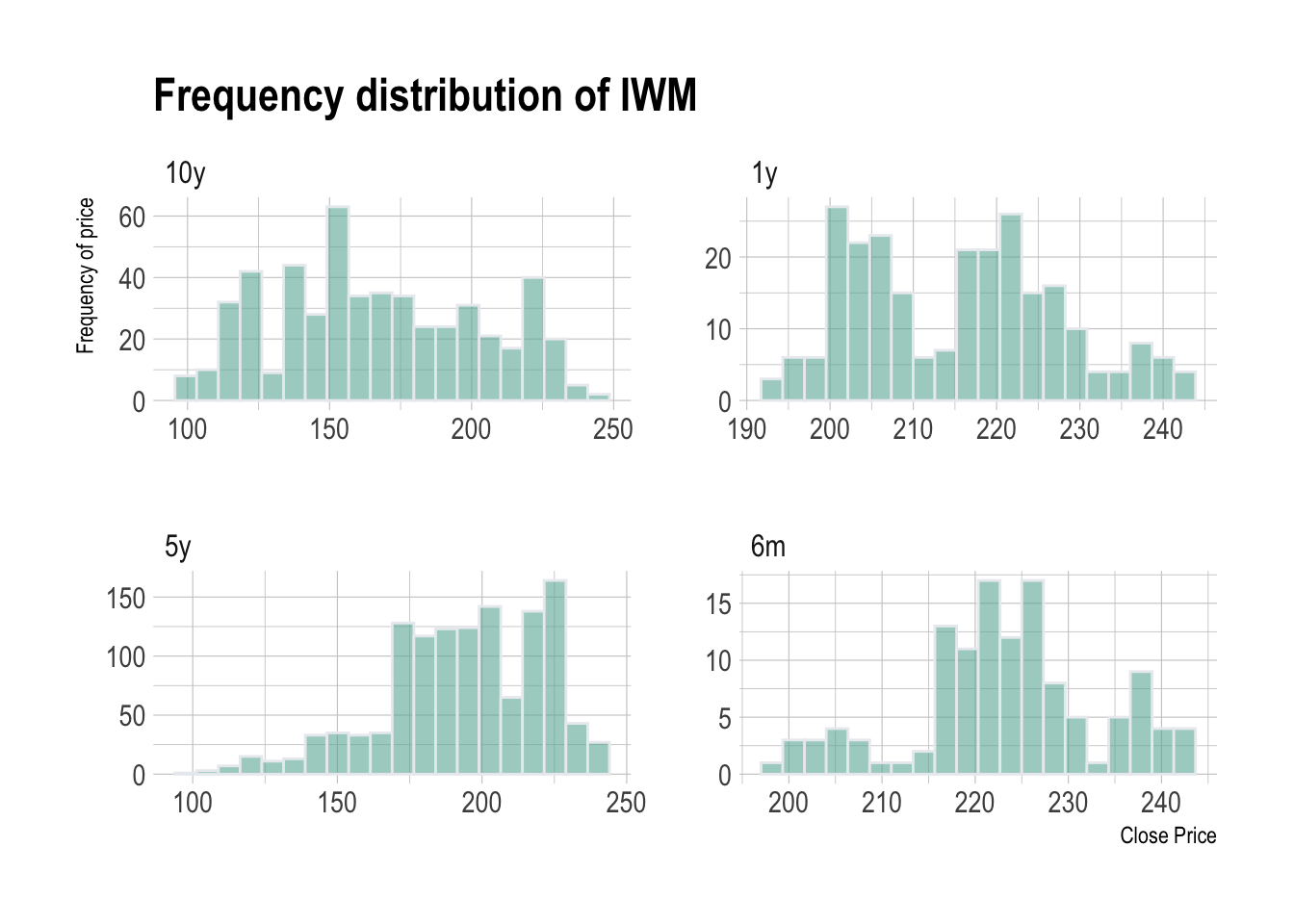

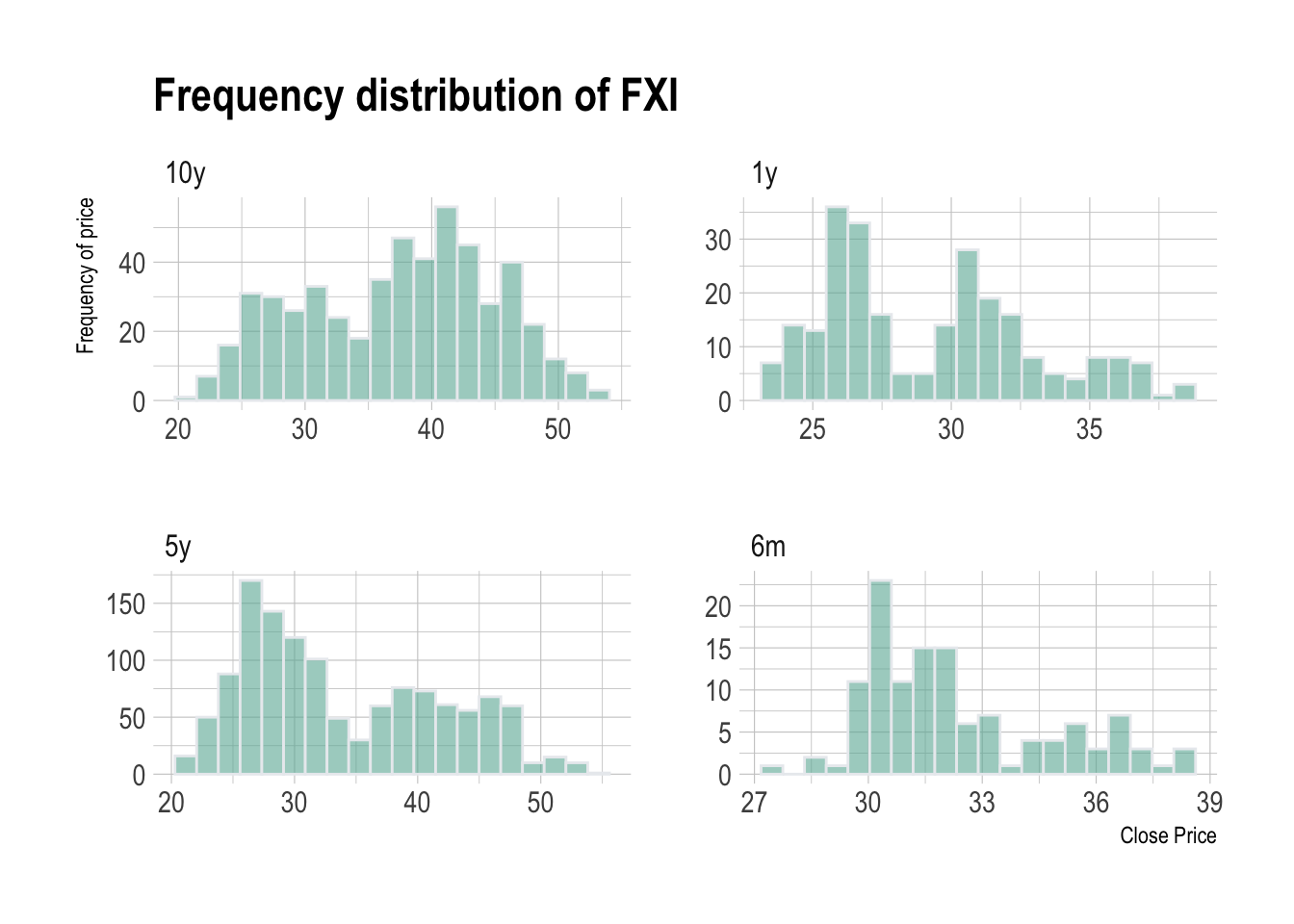

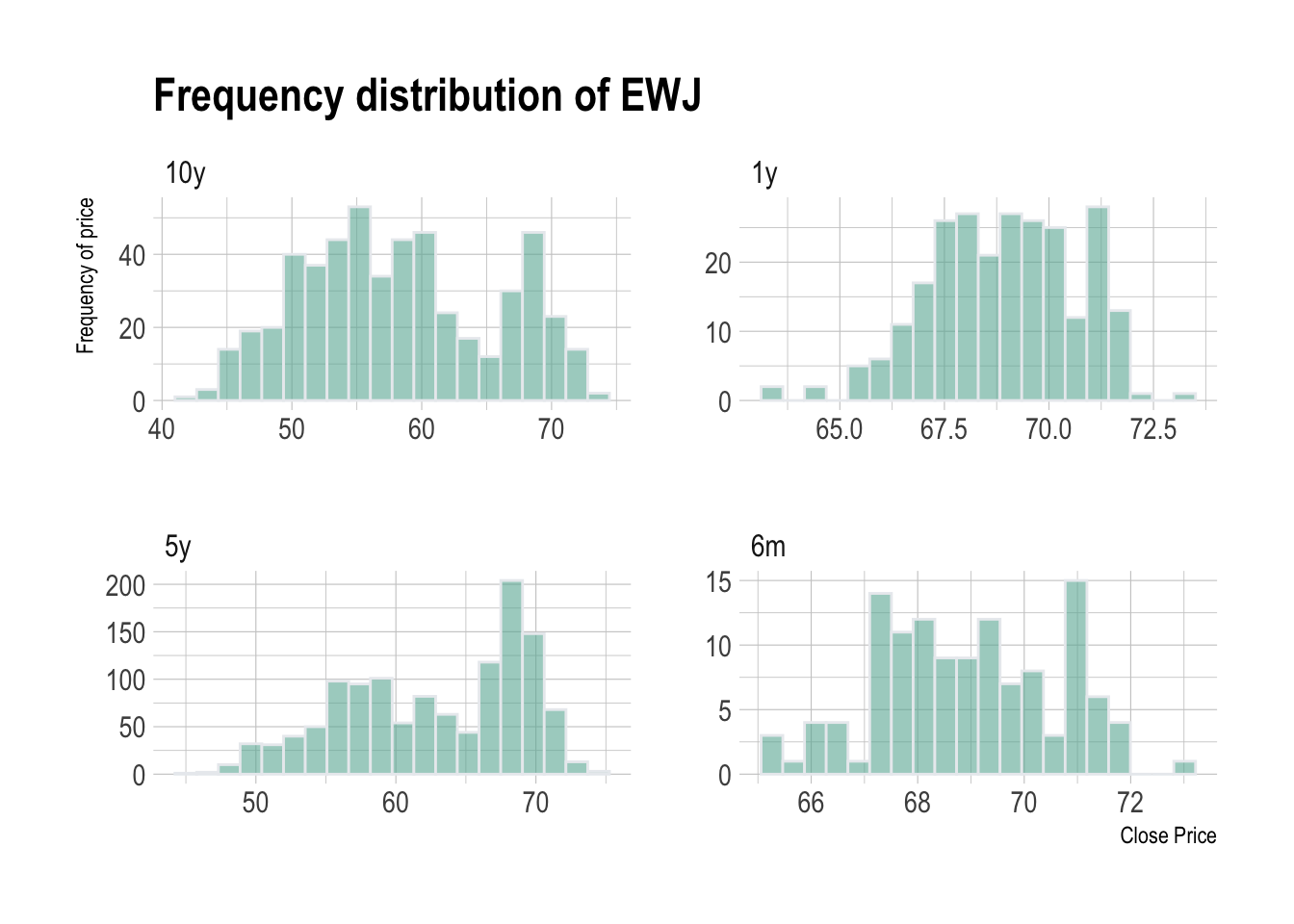

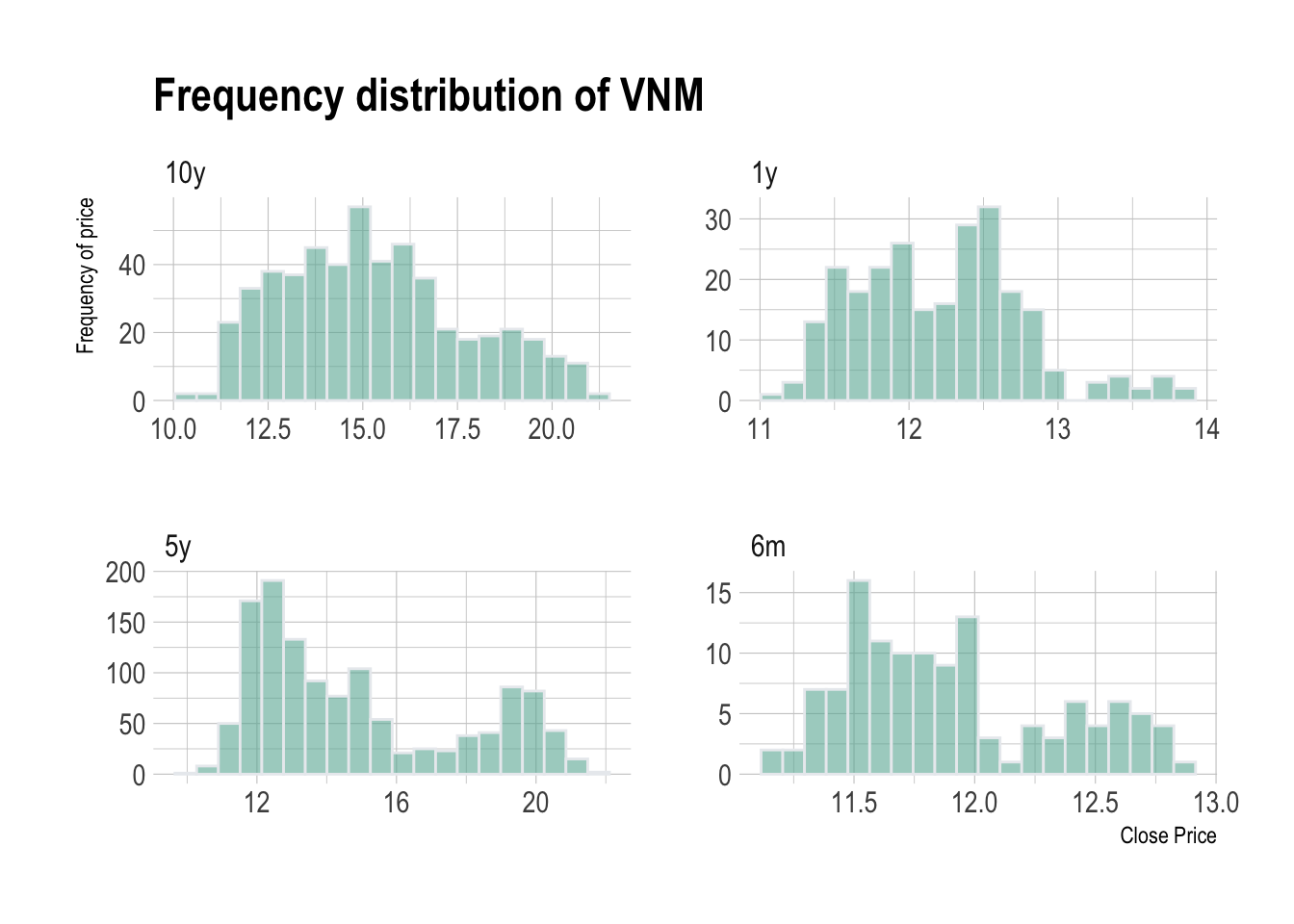

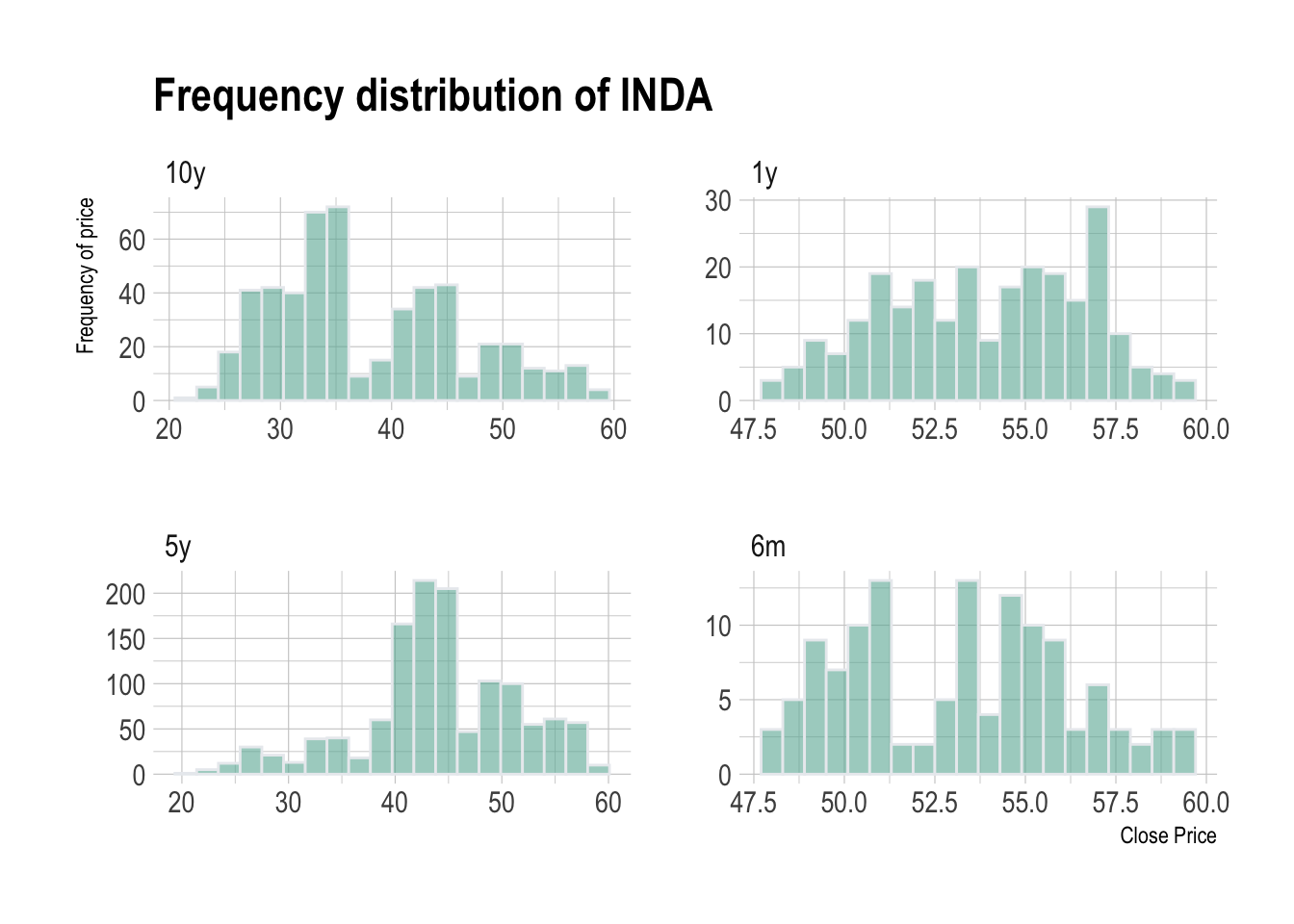

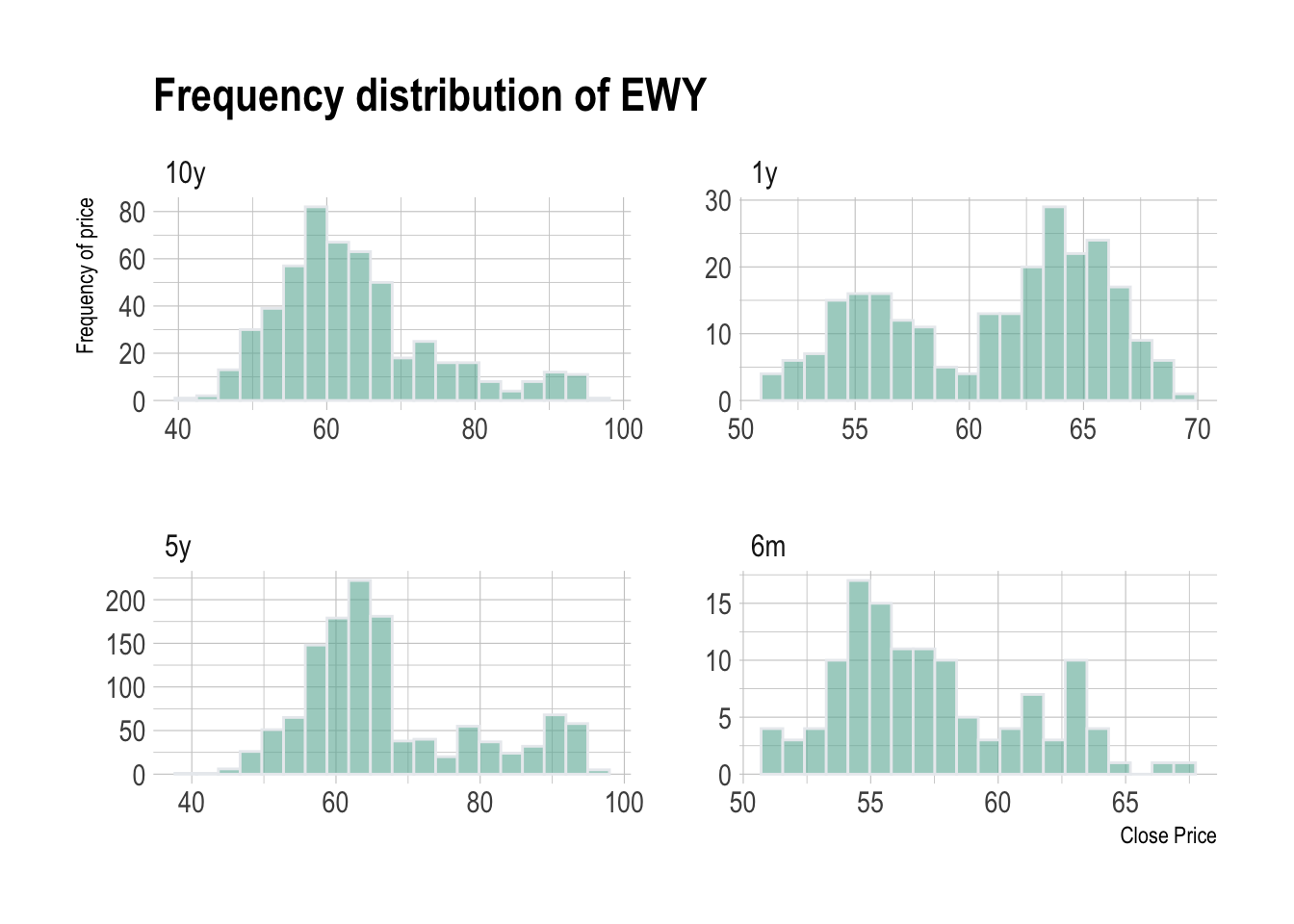

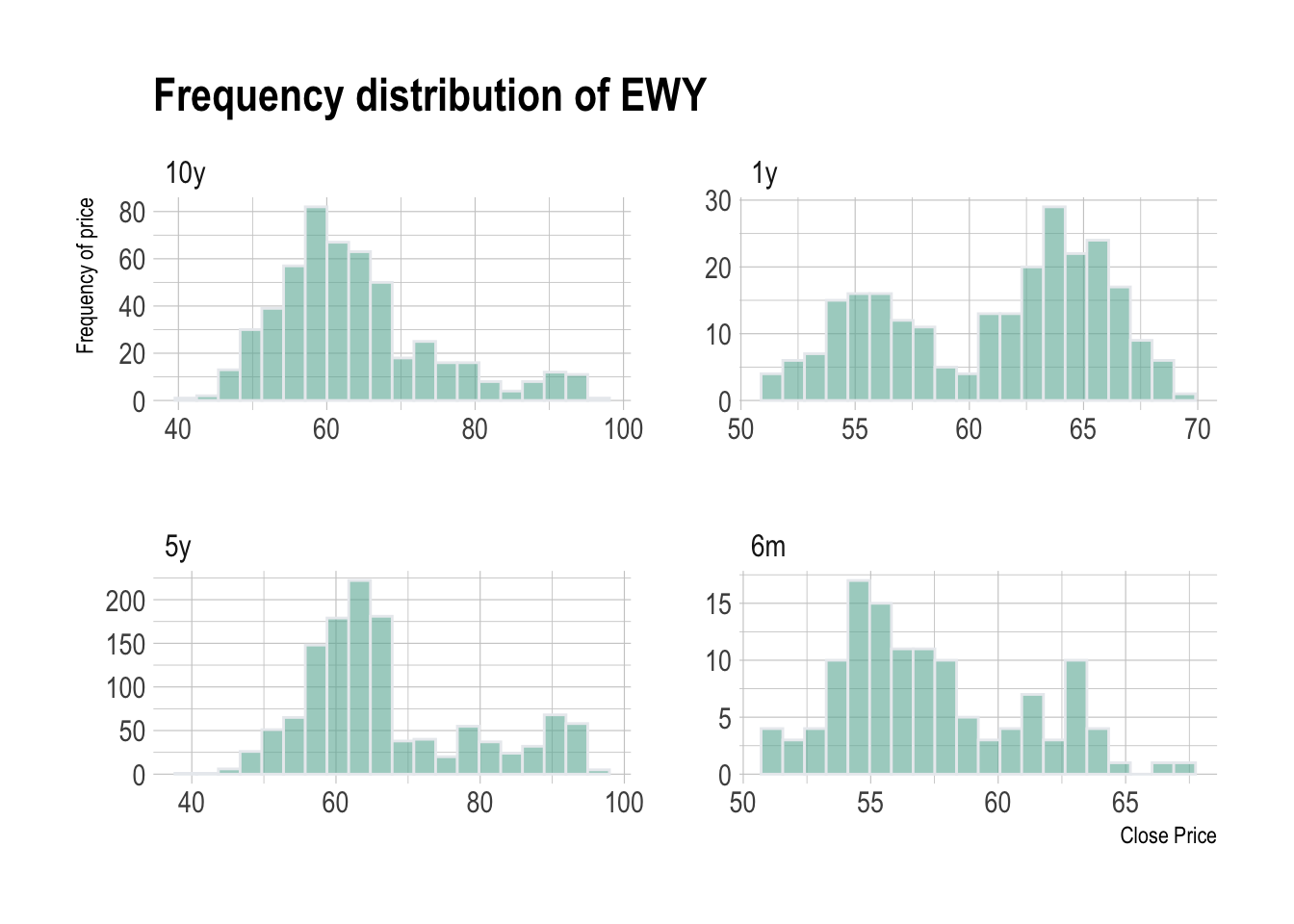

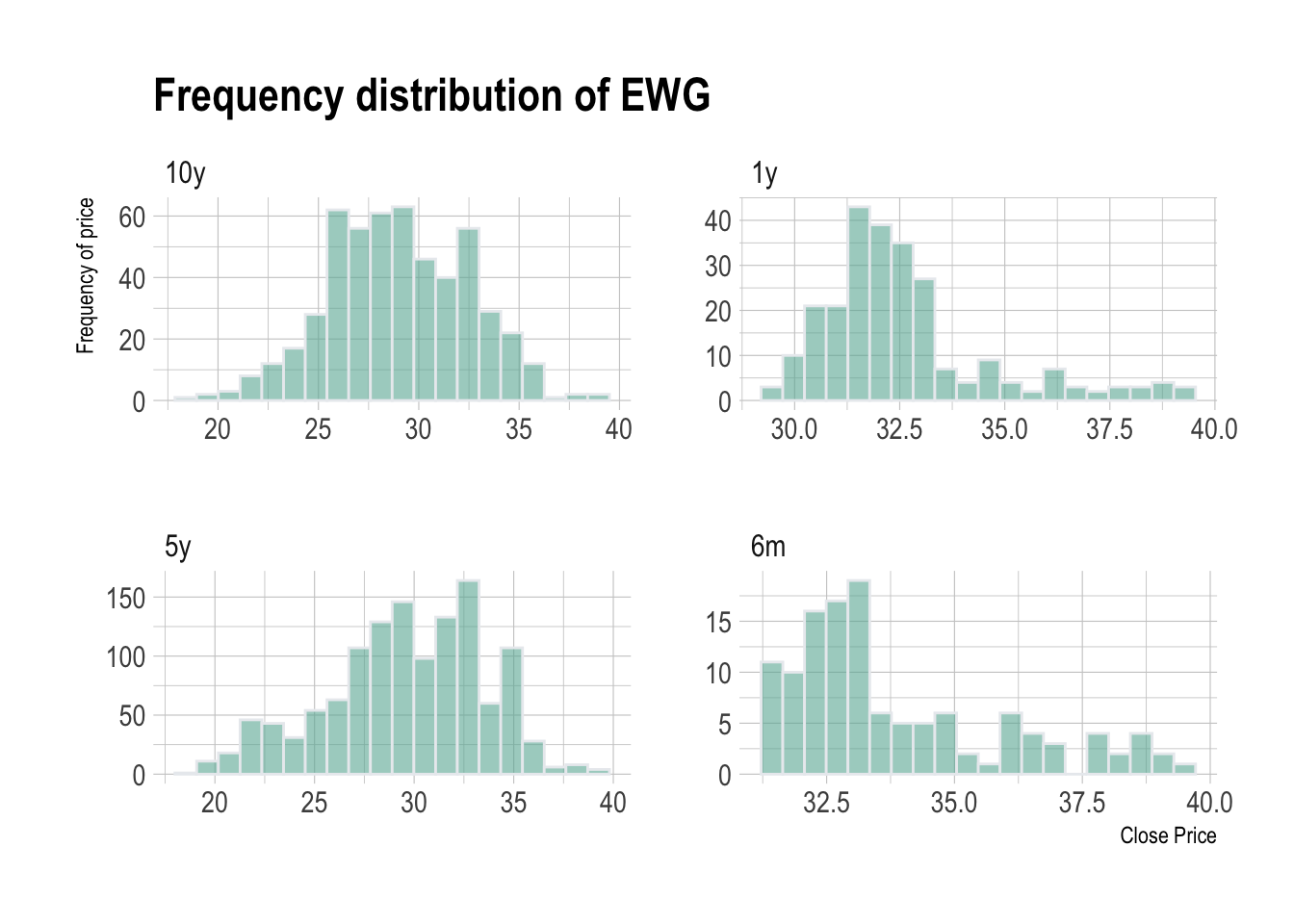

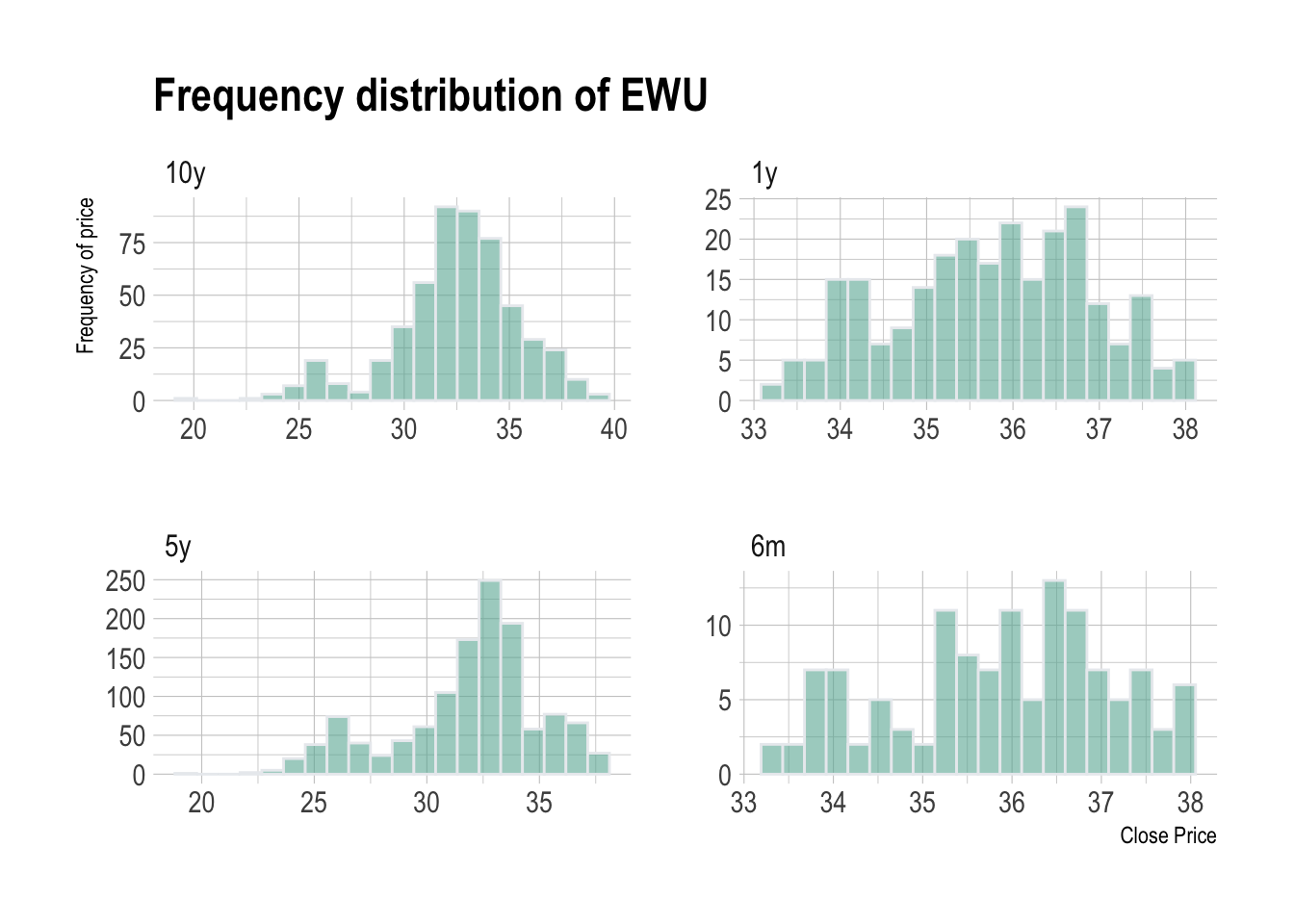

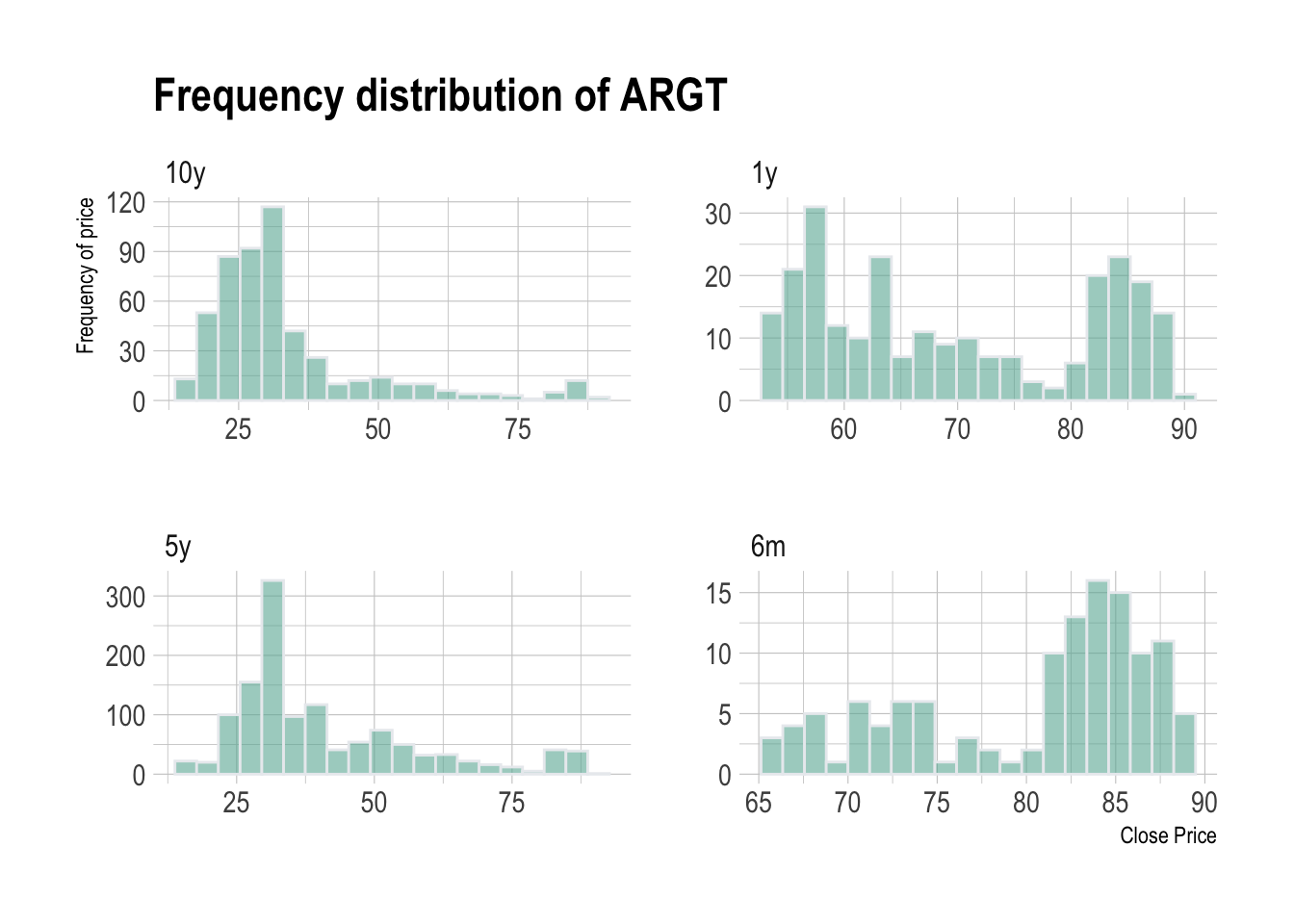

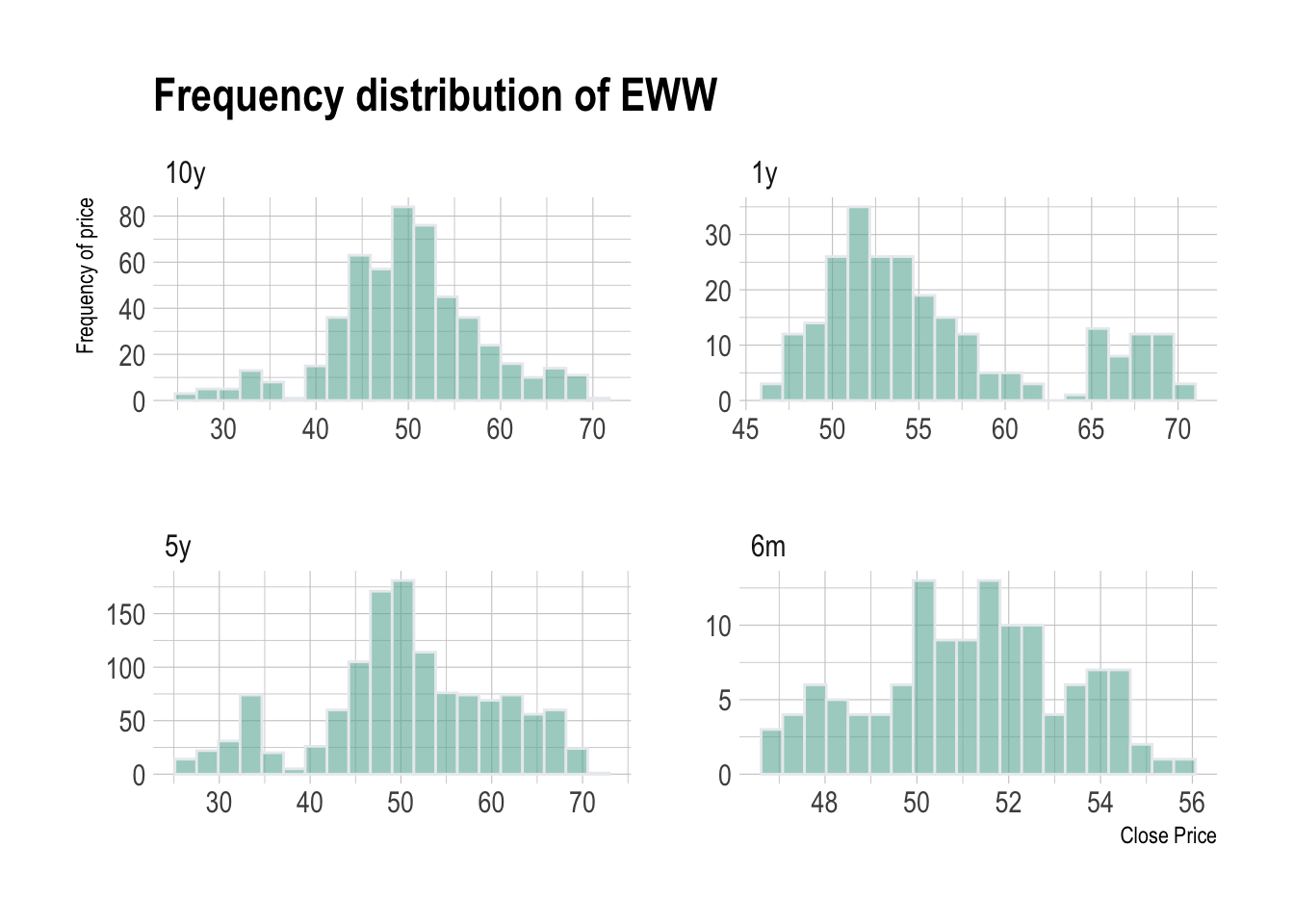

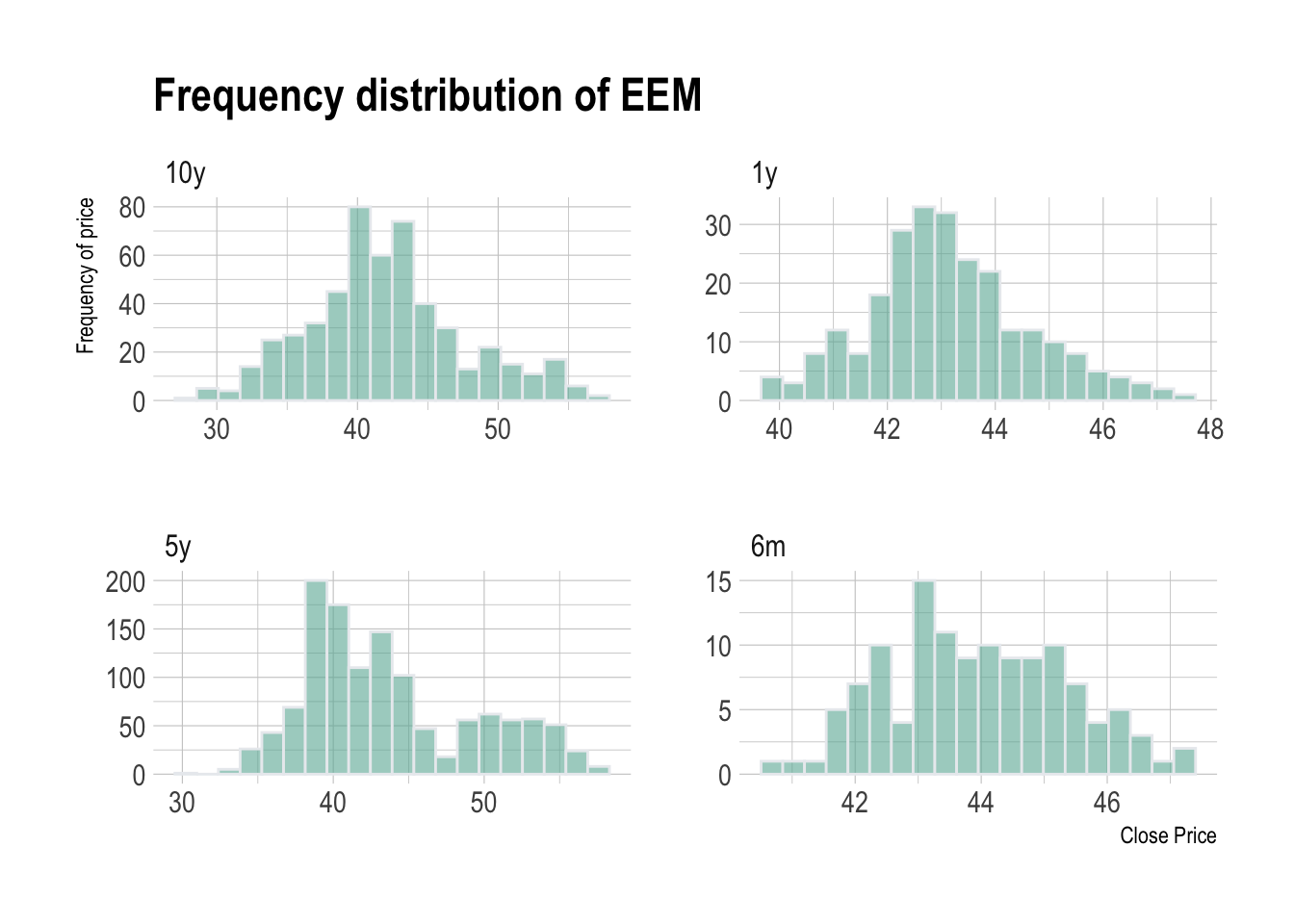

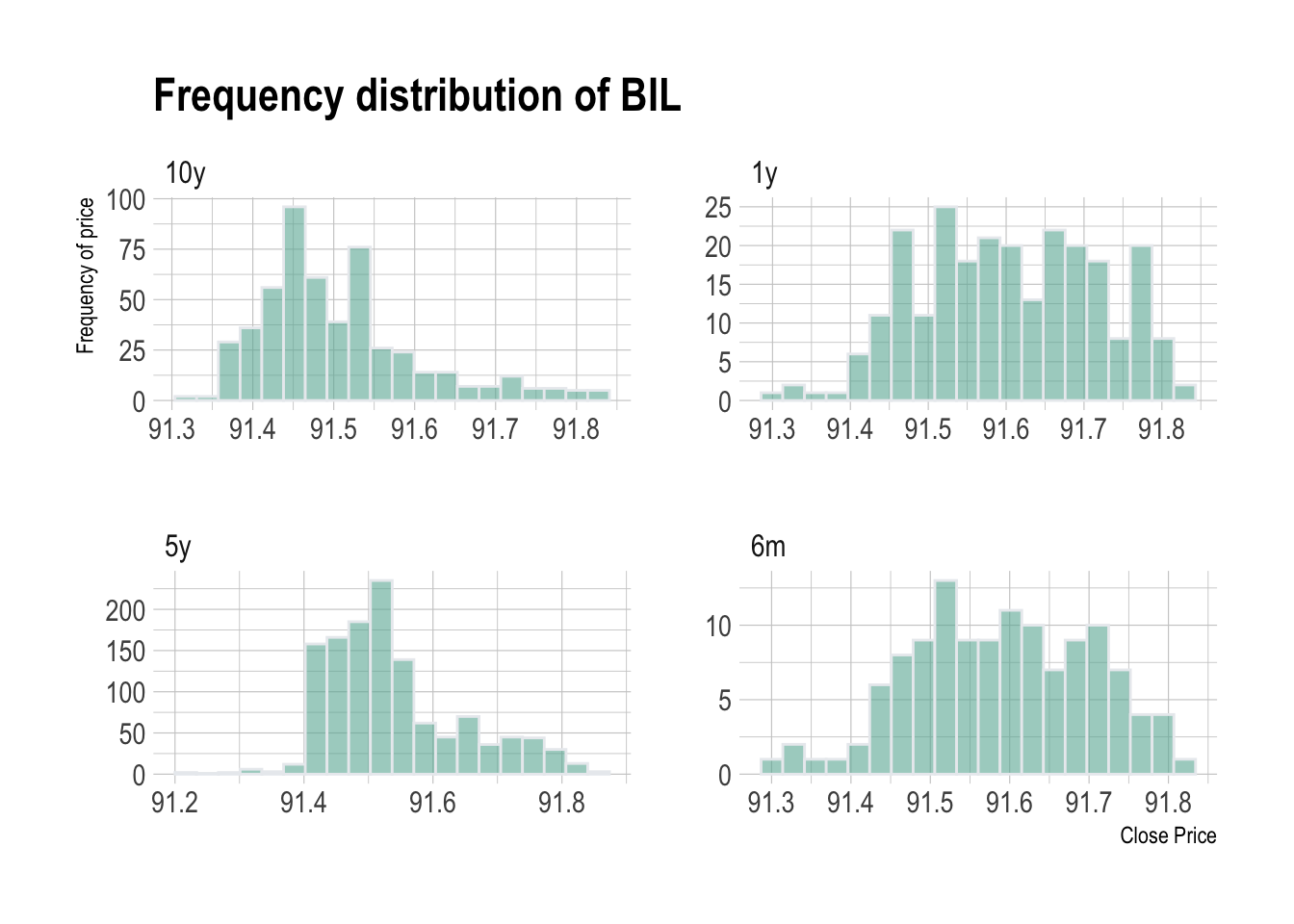

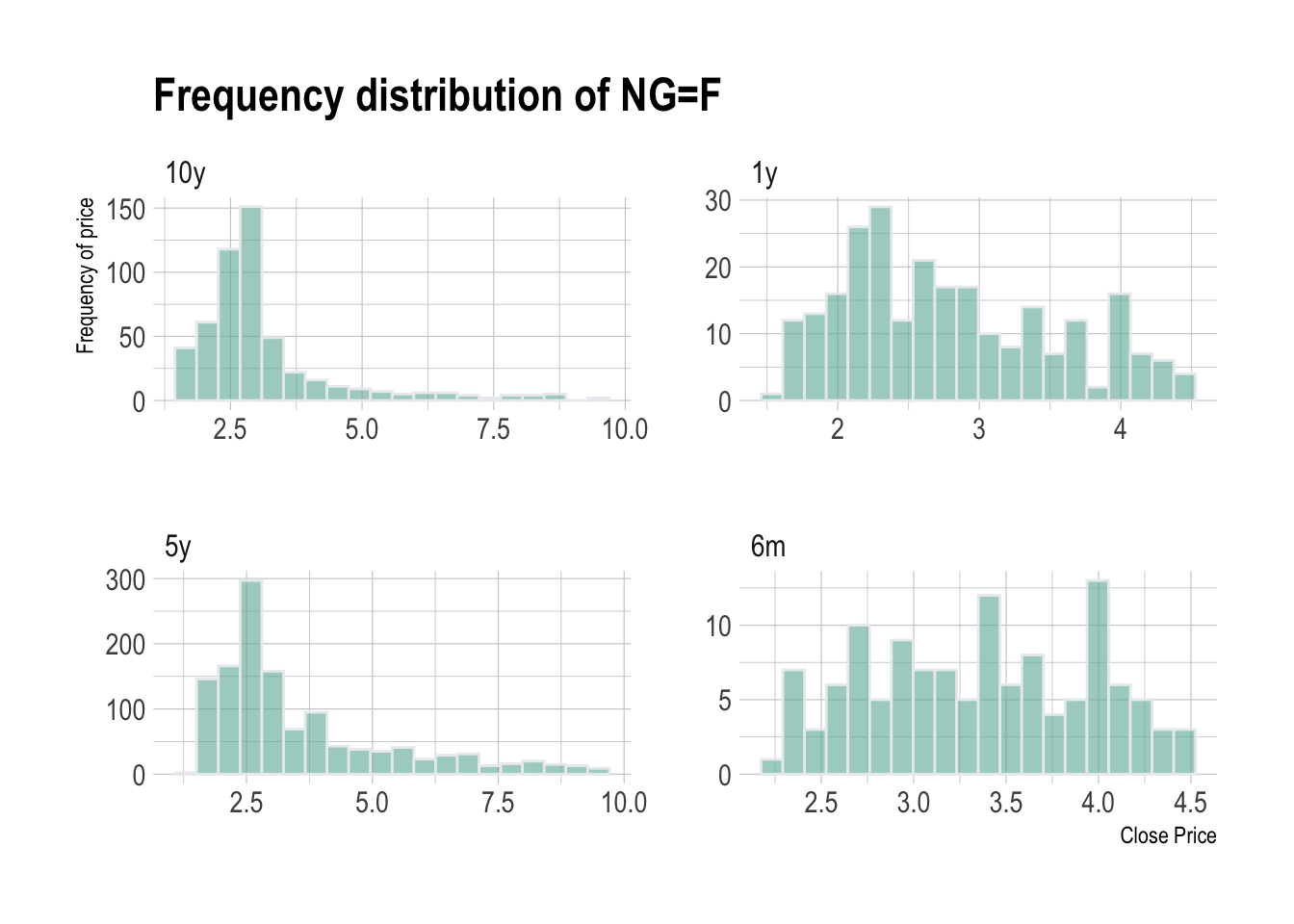

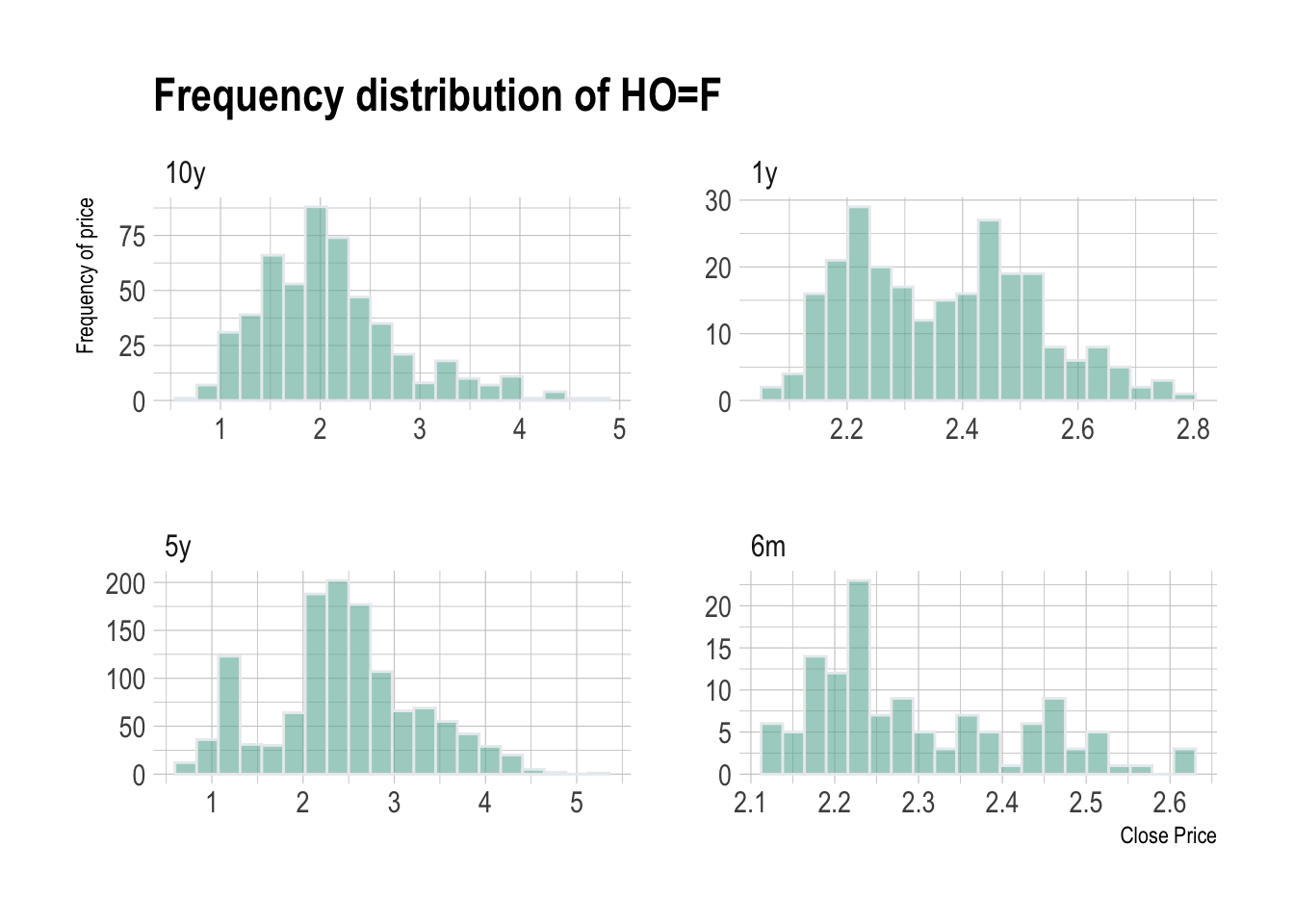

We can also know which prices are mostly traded at different timeframe, and usually these prices will be close to support or resistance. The most frequent occurrences are at the price where supply and demand are balanced, also known as equilibrium.

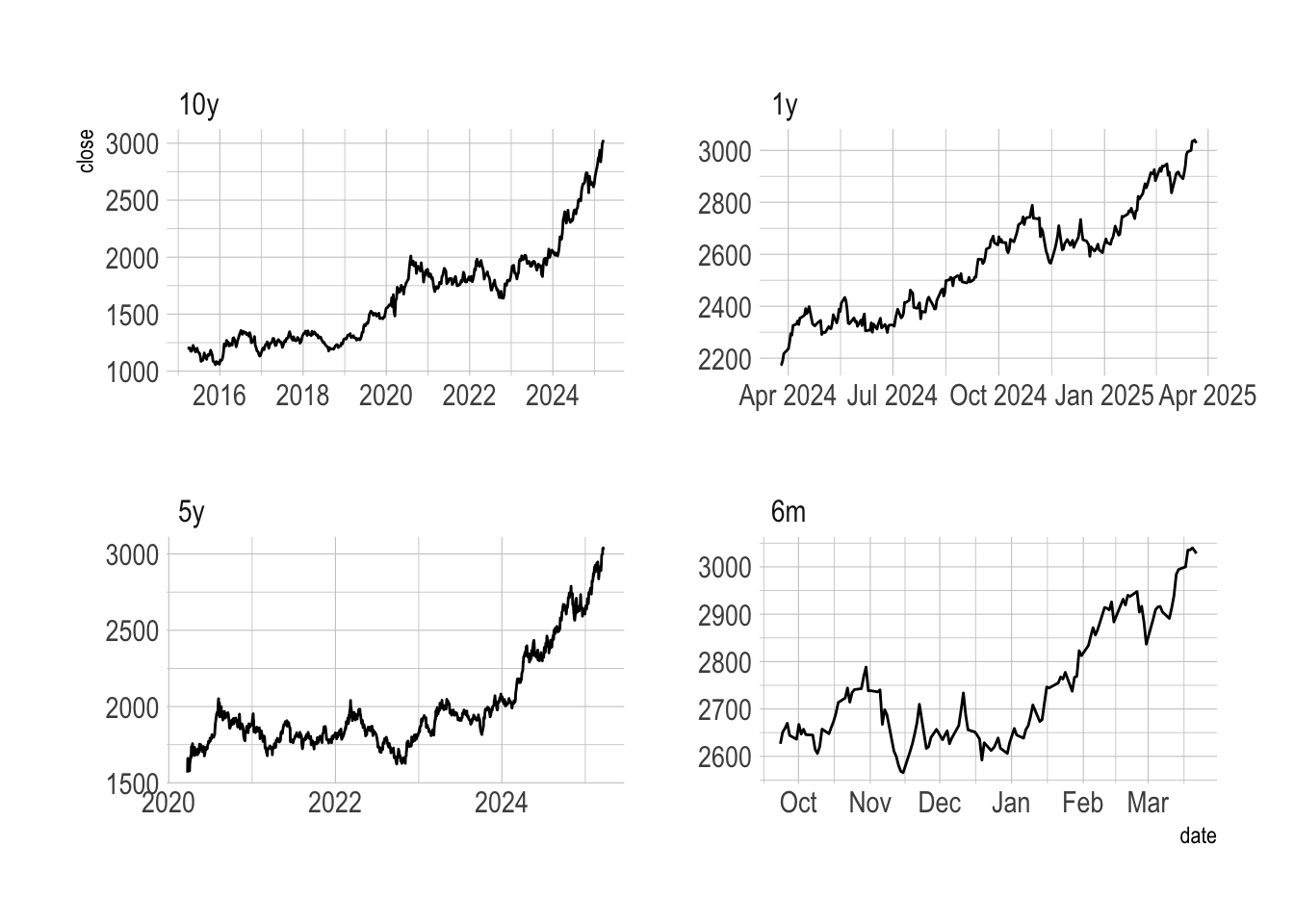

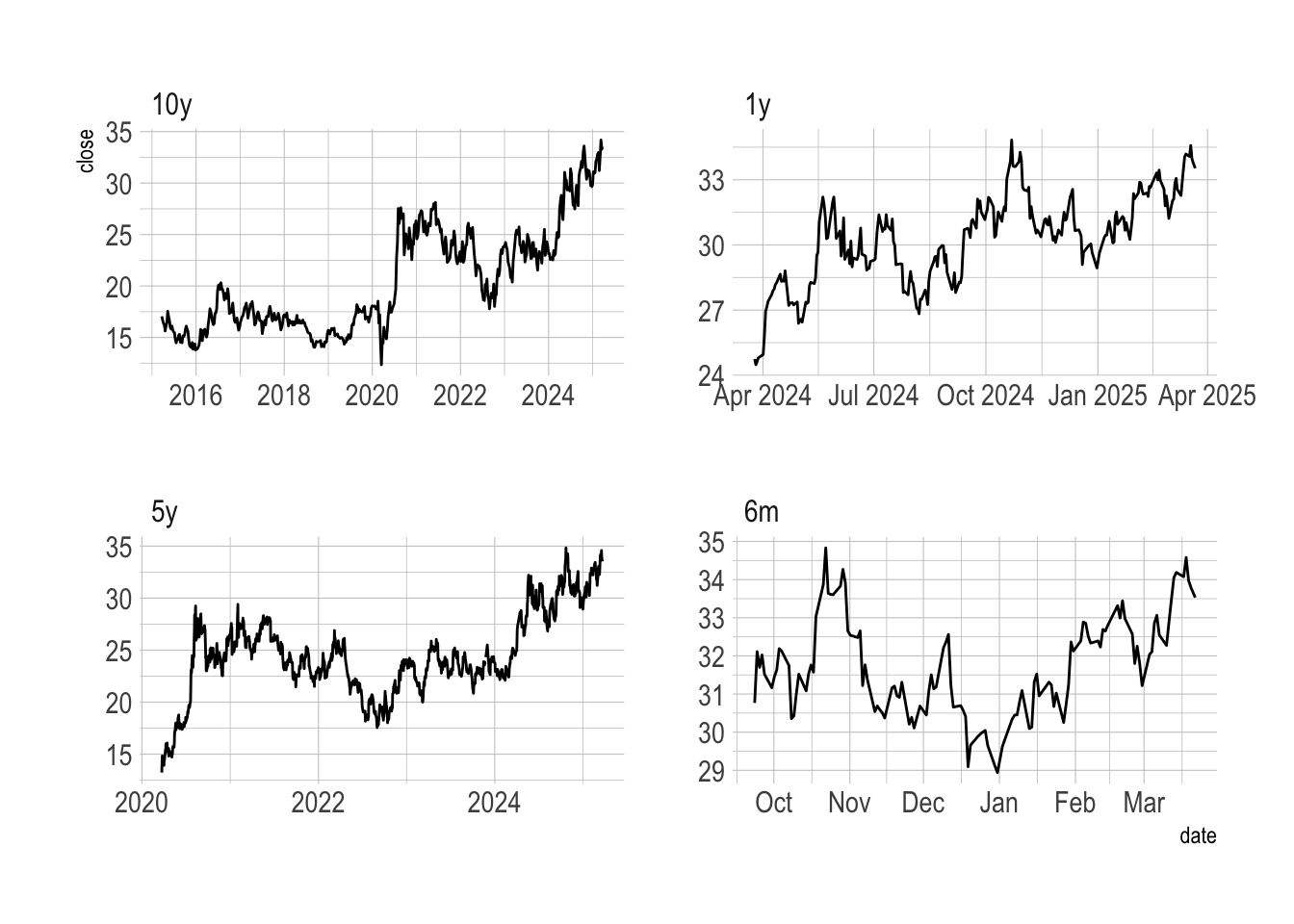

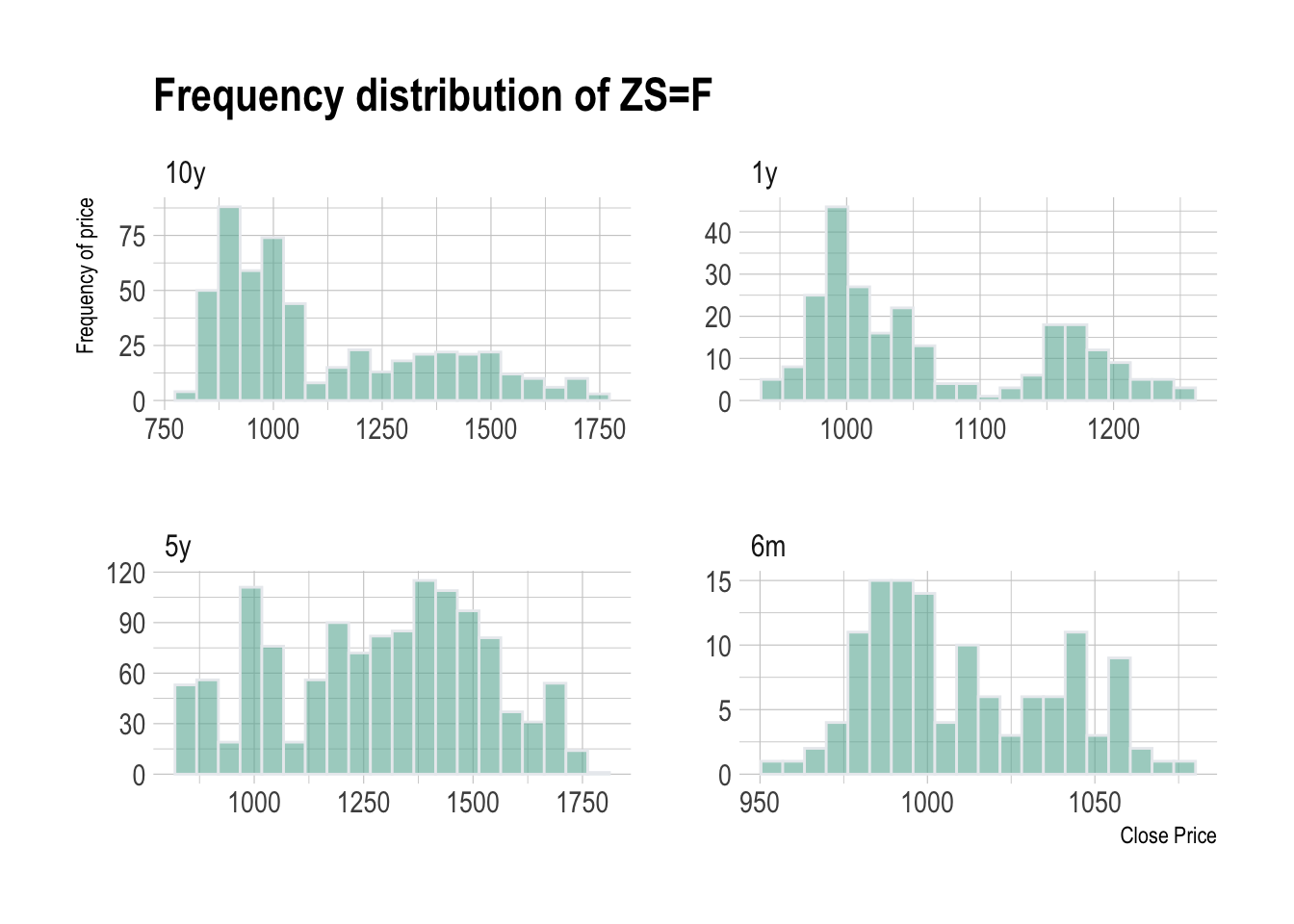

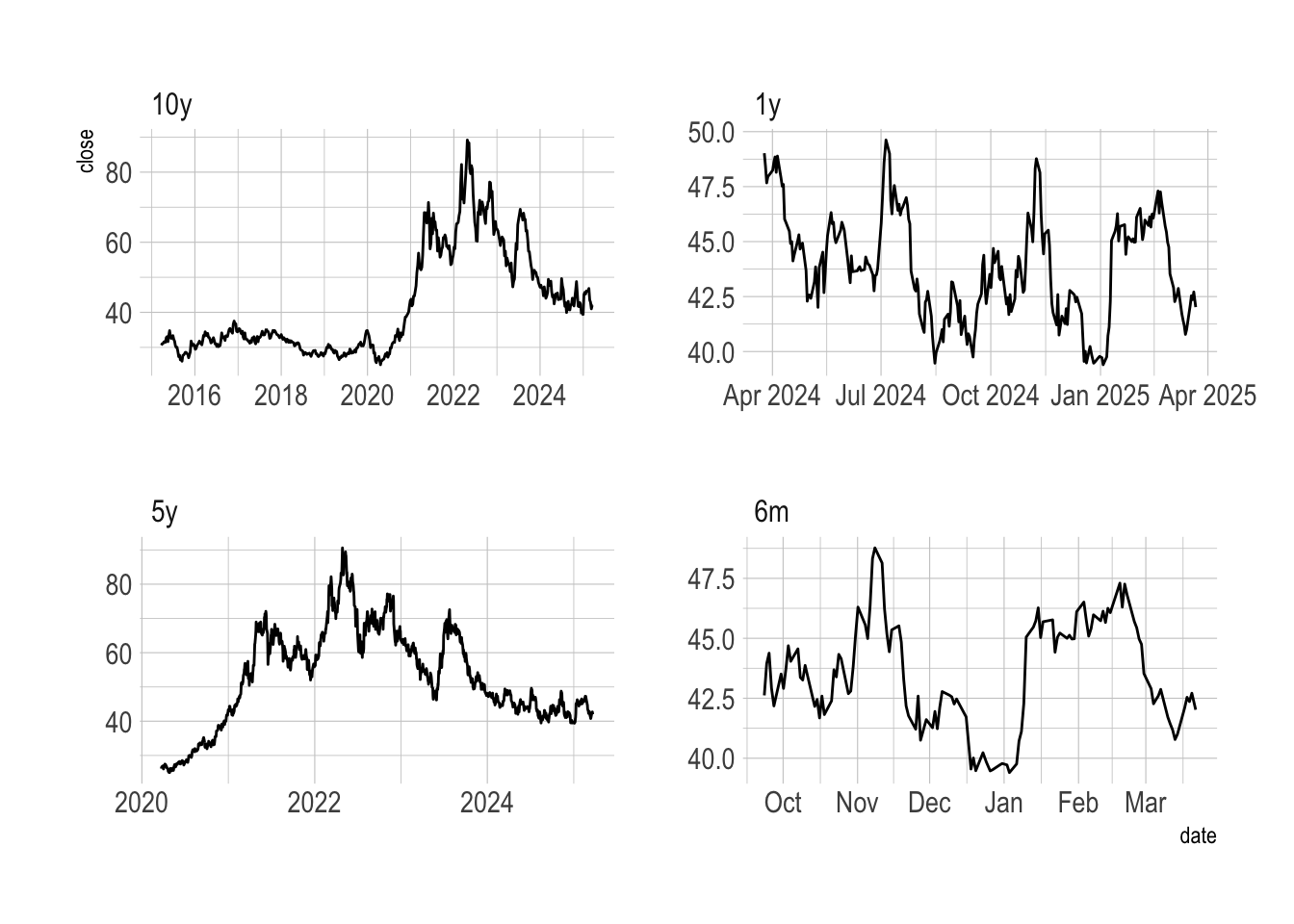

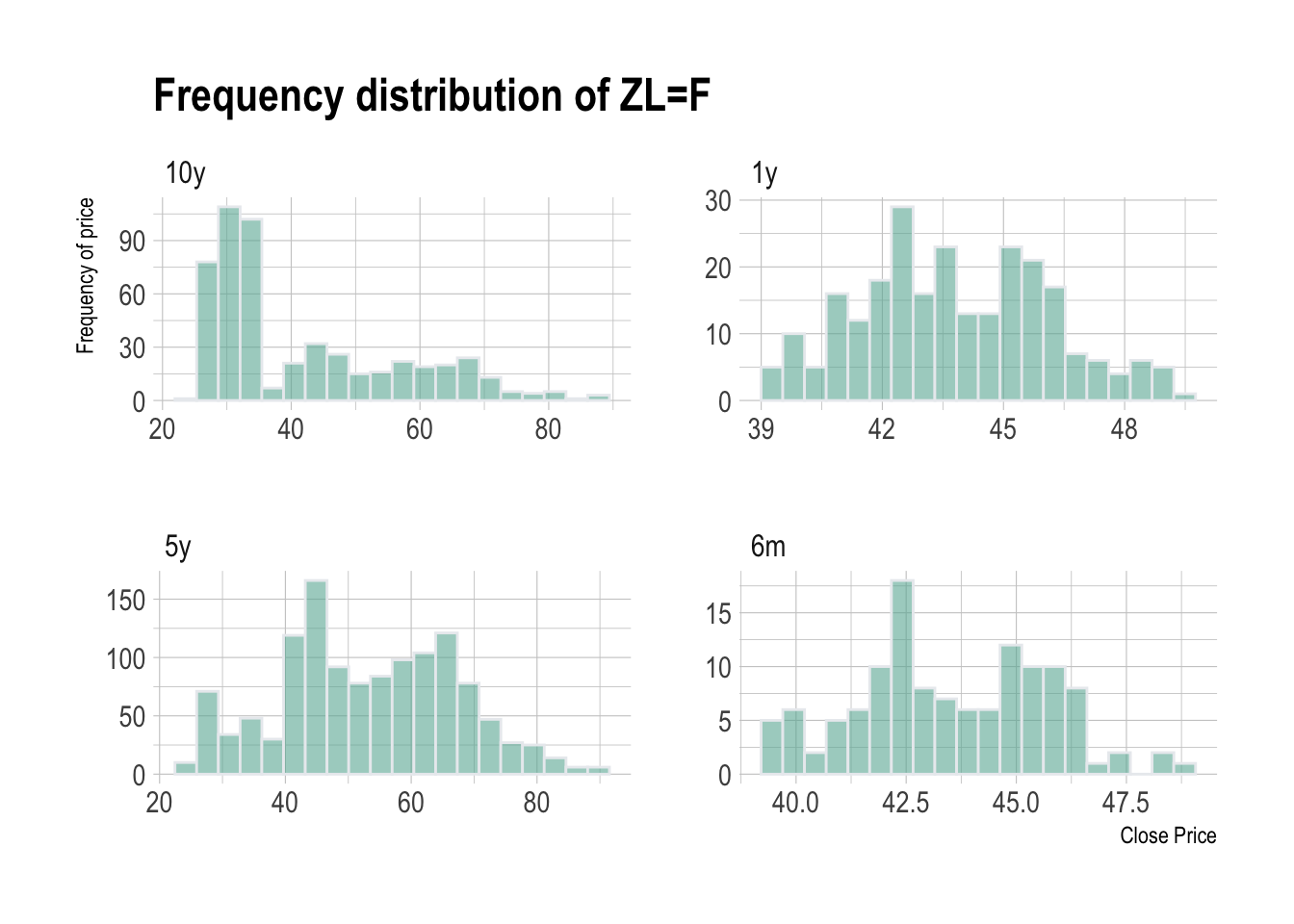

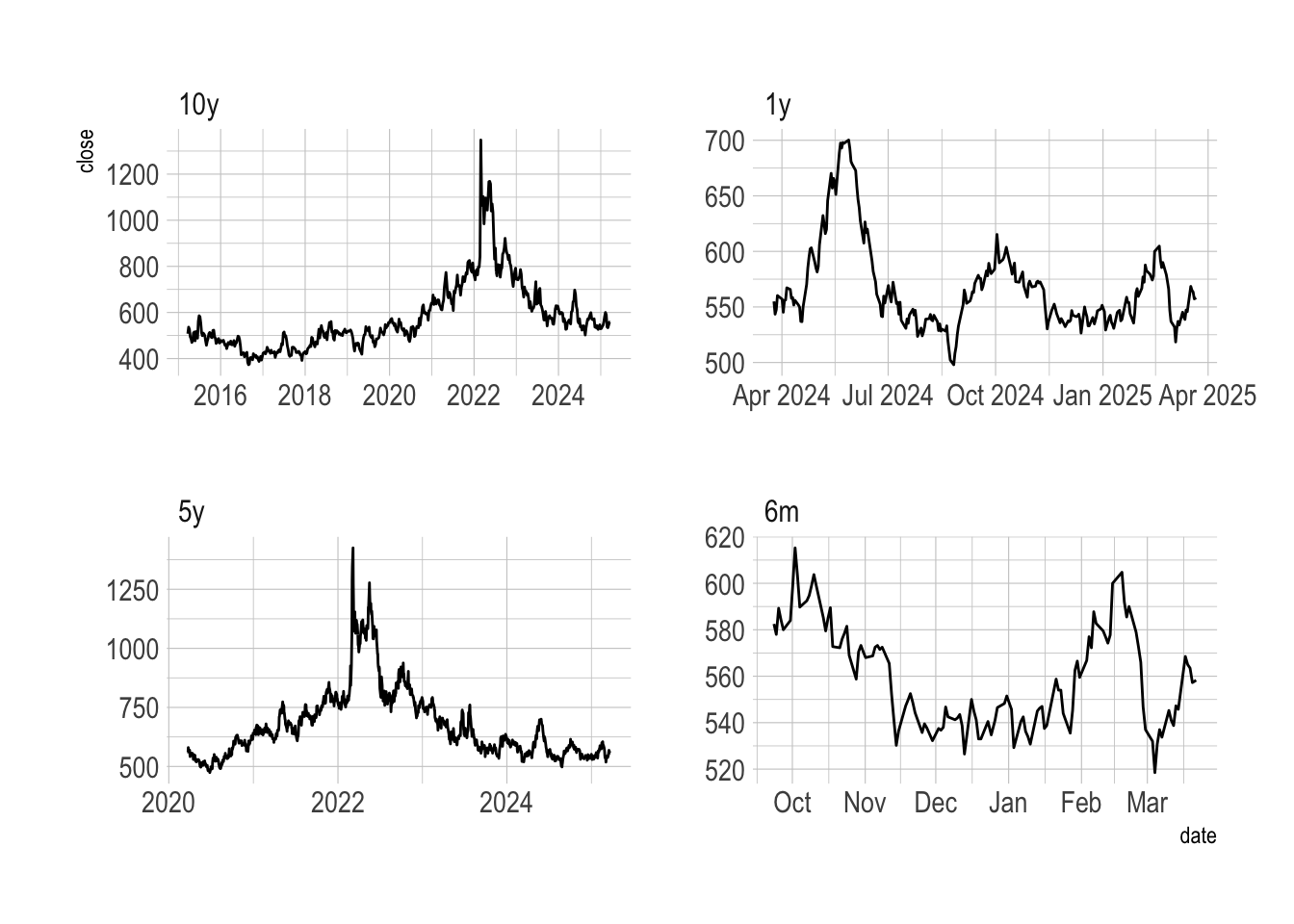

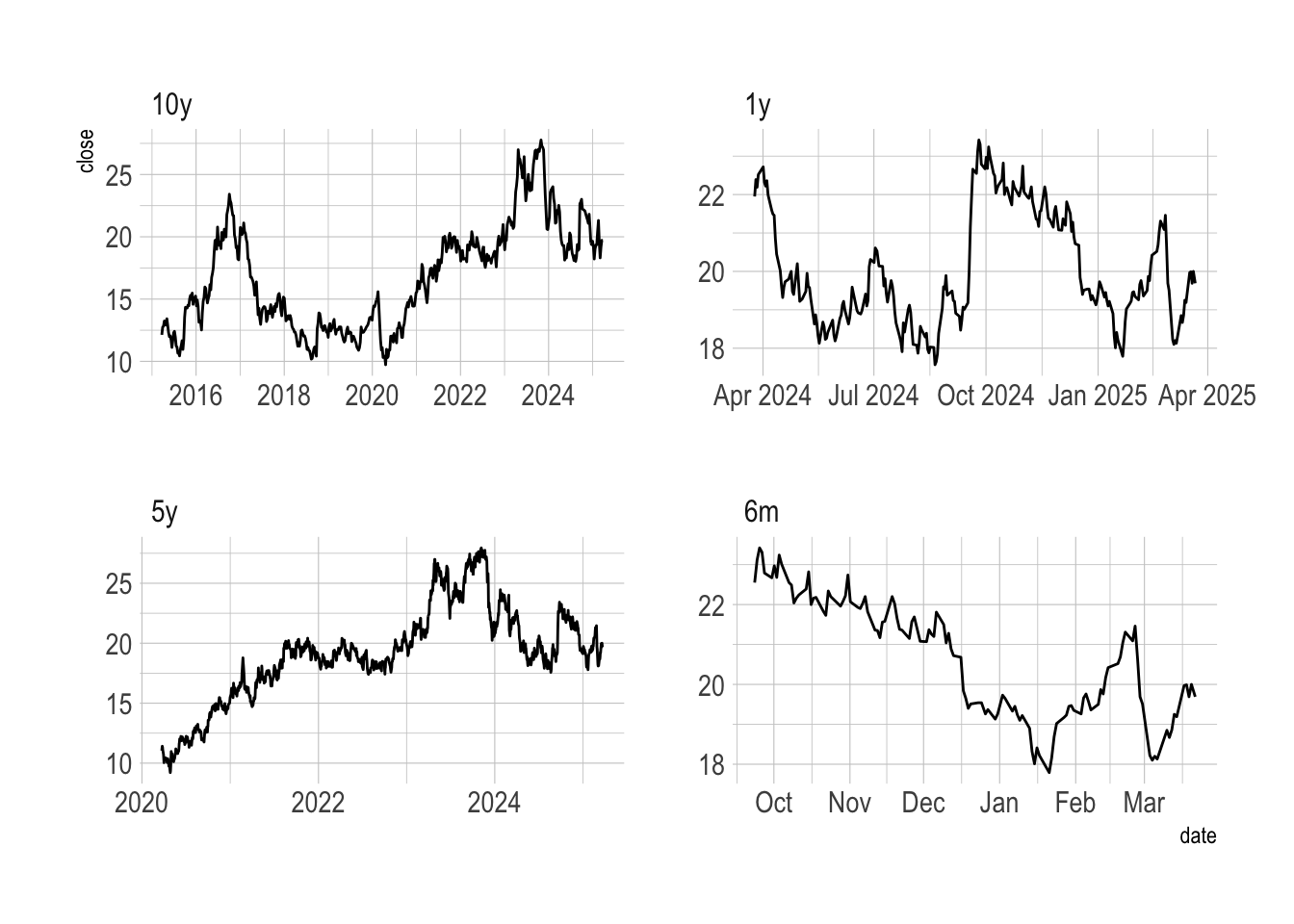

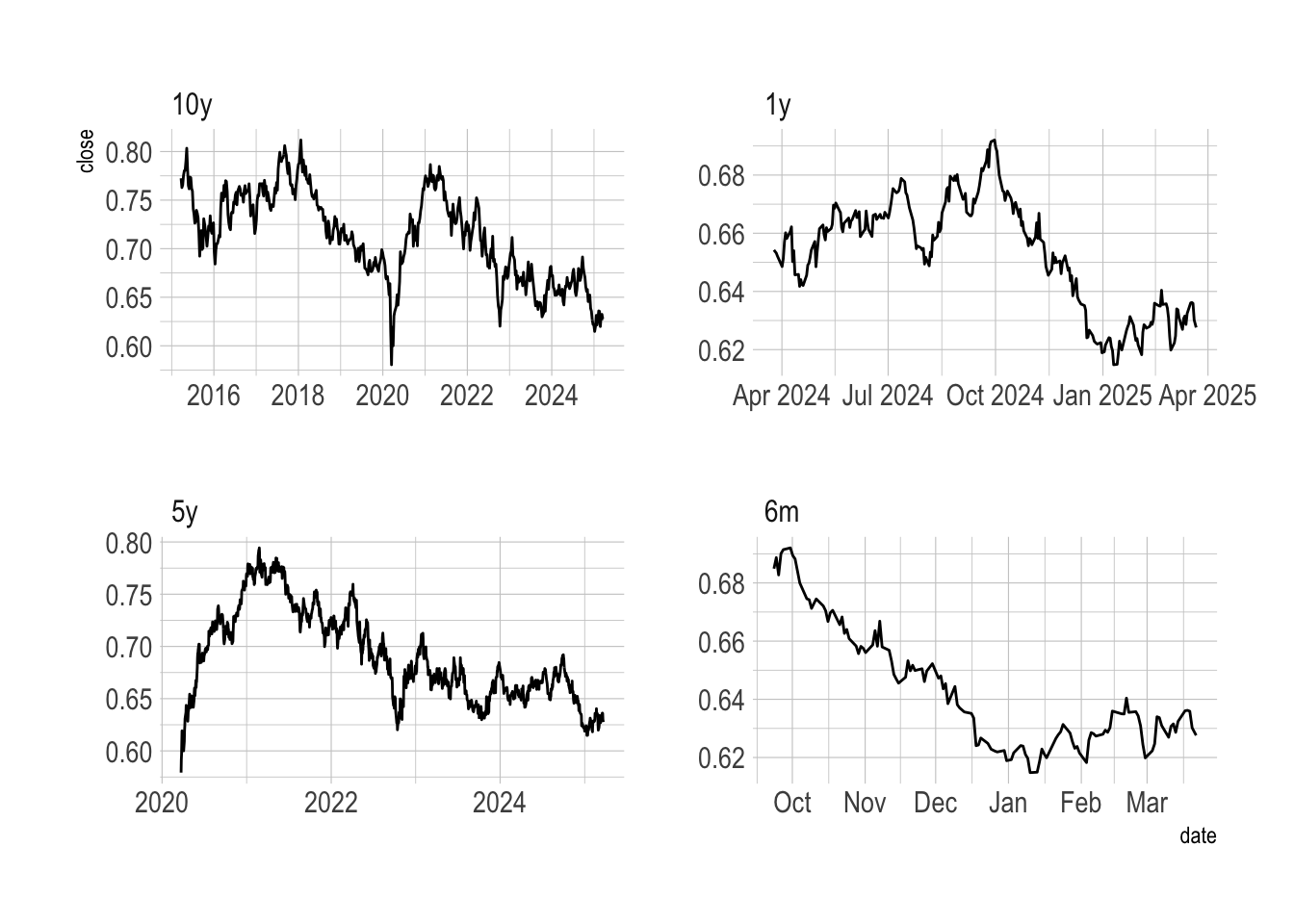

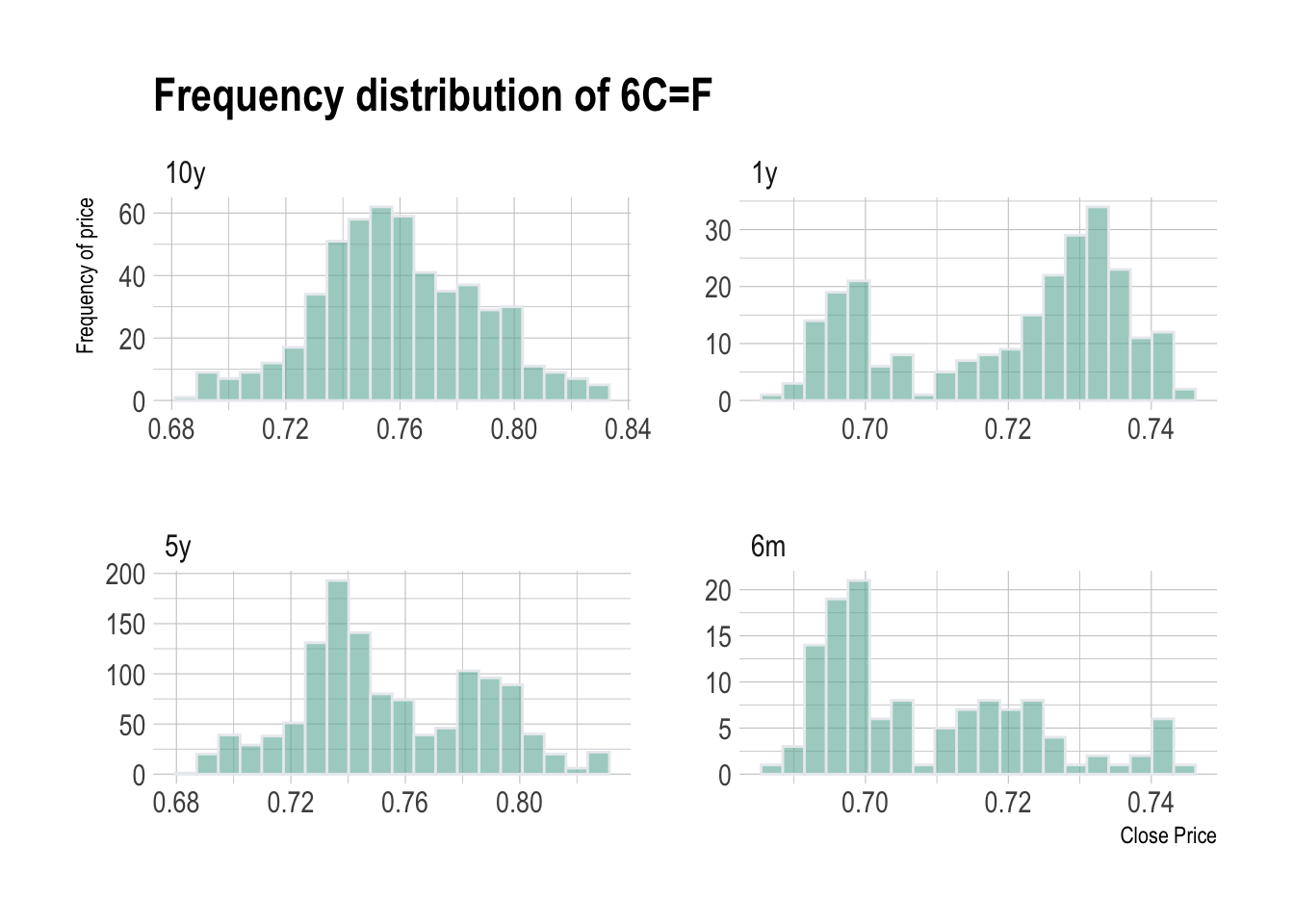

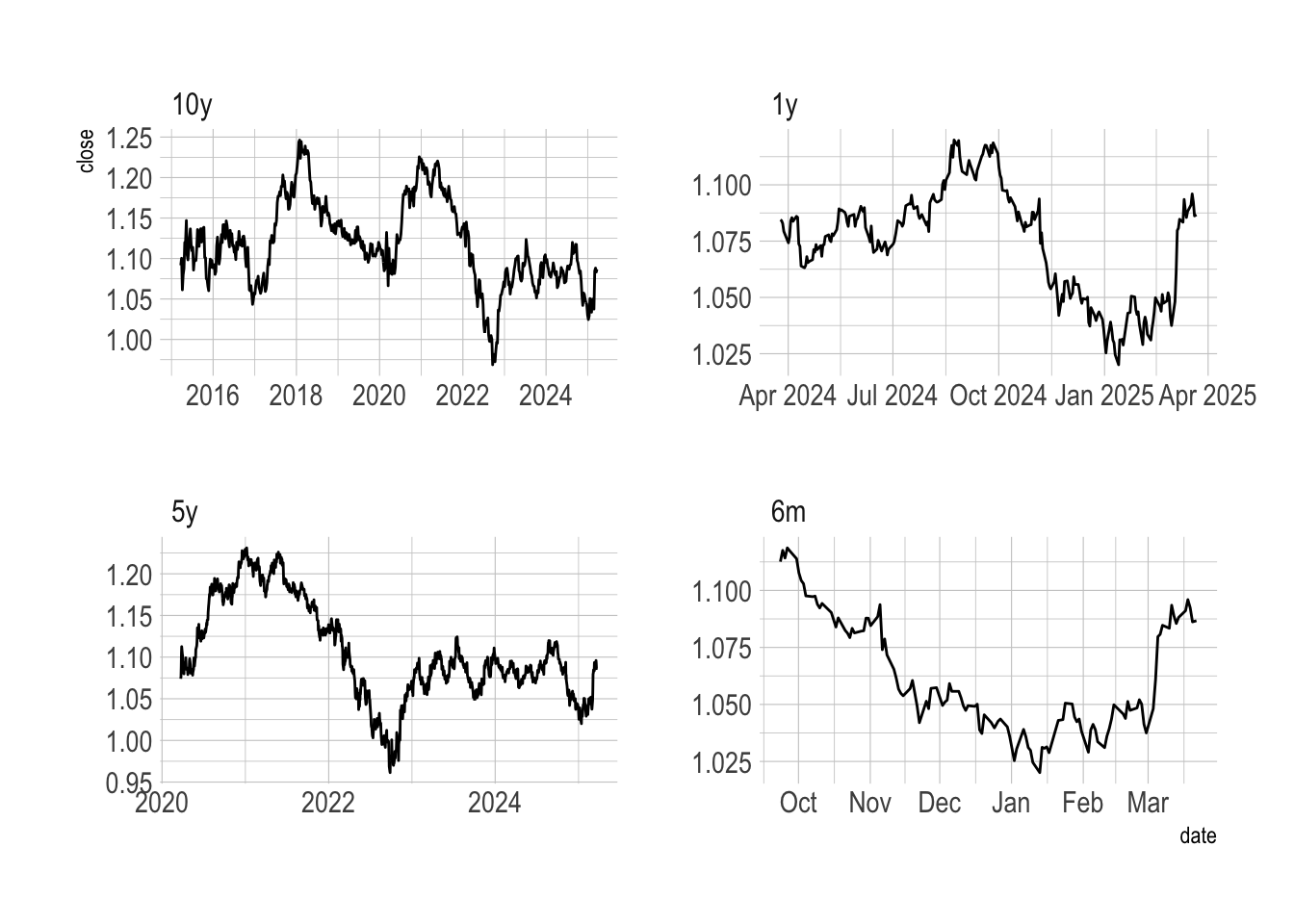

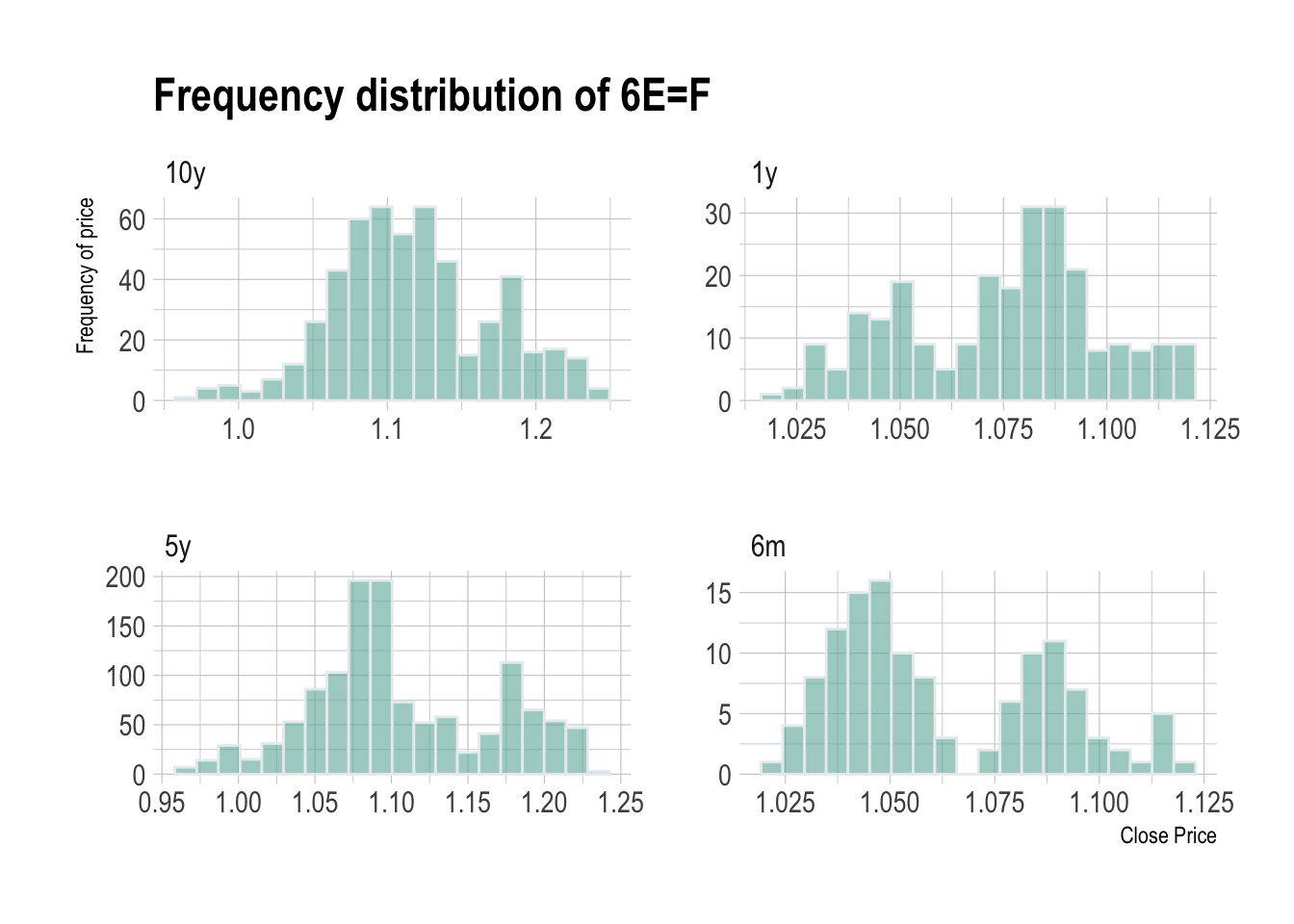

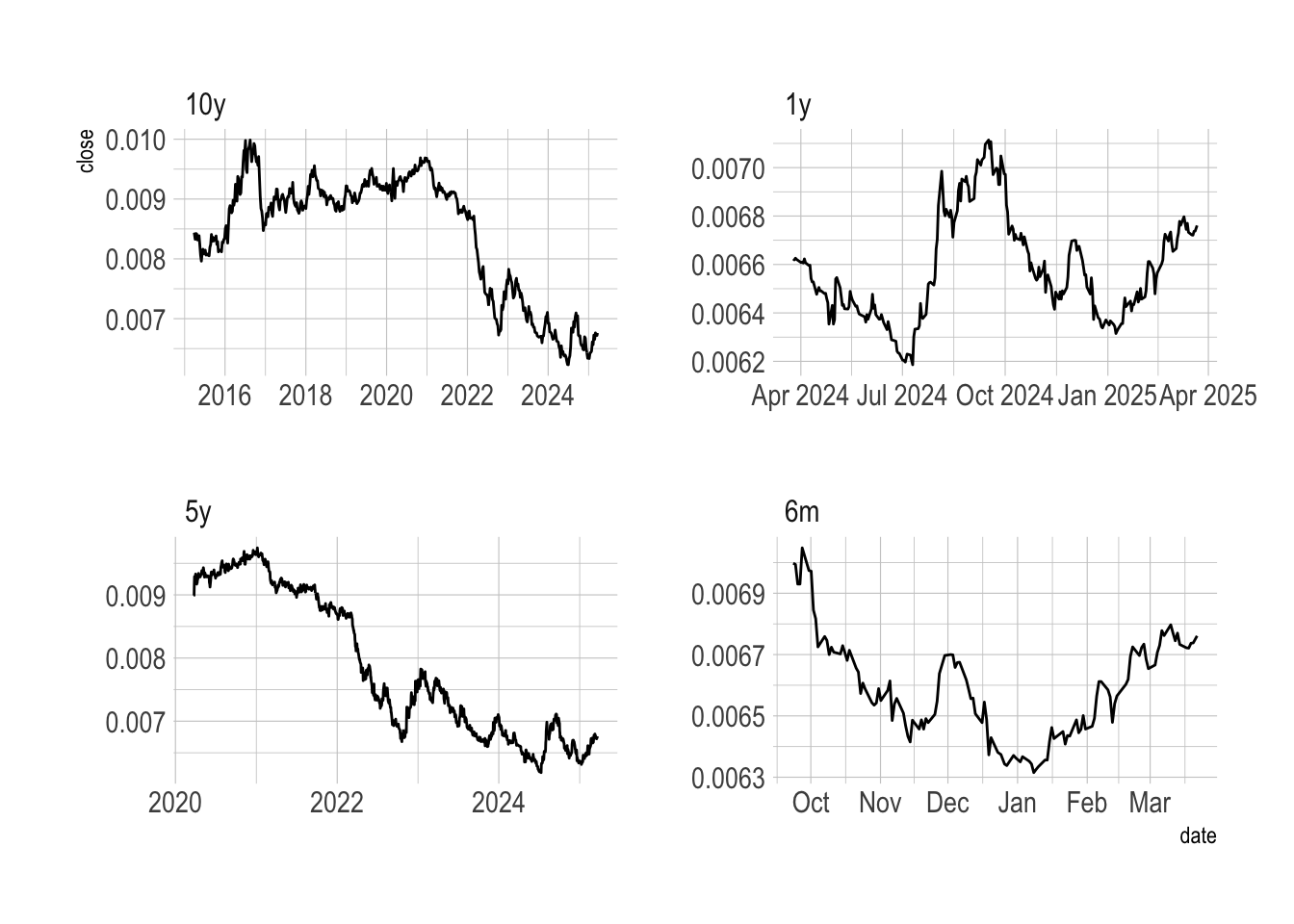

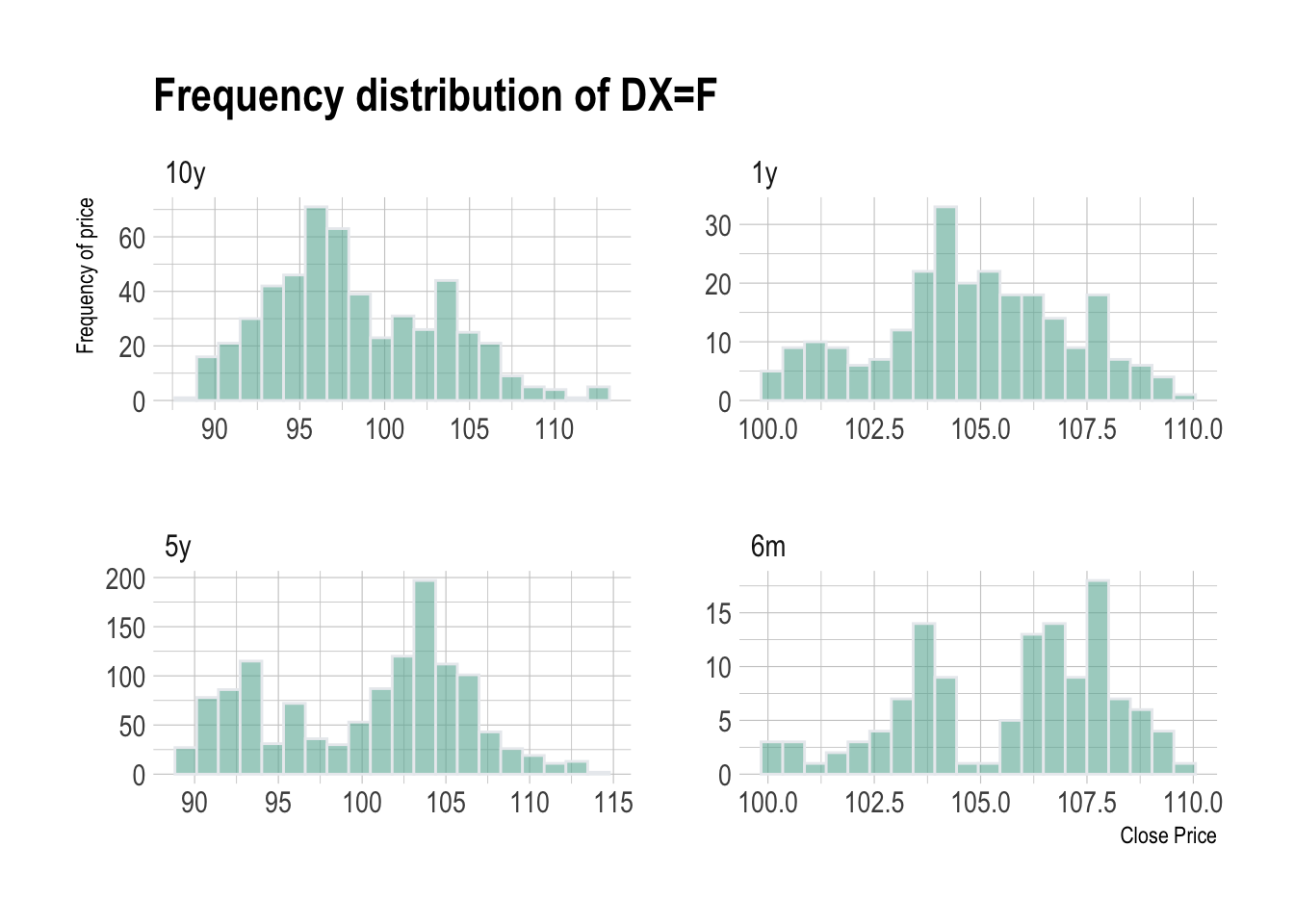

This post aims to use this techniques to analyse my selected universe of trading for my algo strategies. I am trying to replicate the methodology on Trading Systems and Methods, 5th Edition (Ch. 2). To start simple, I will collect the data and plot the histogram of the following:

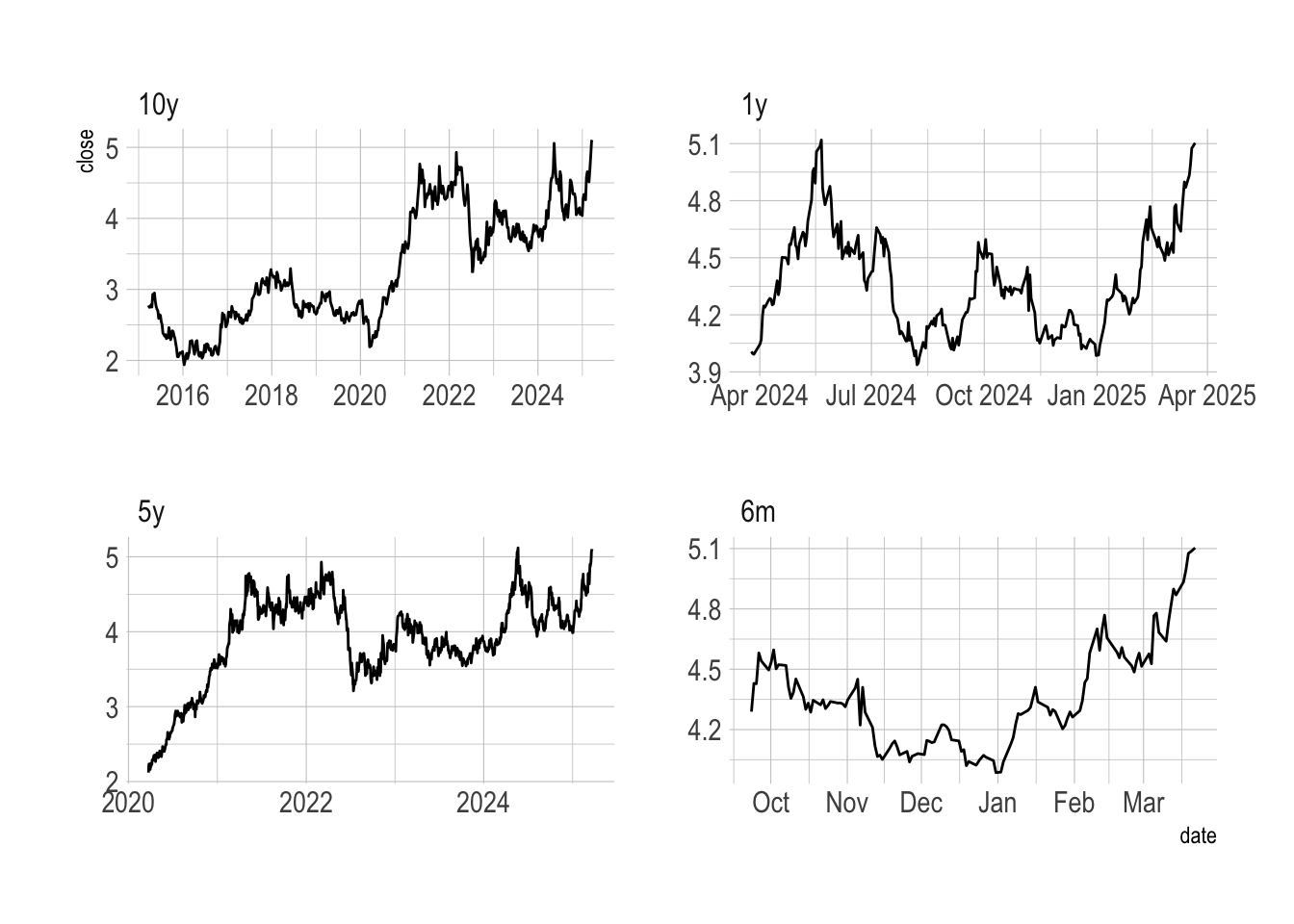

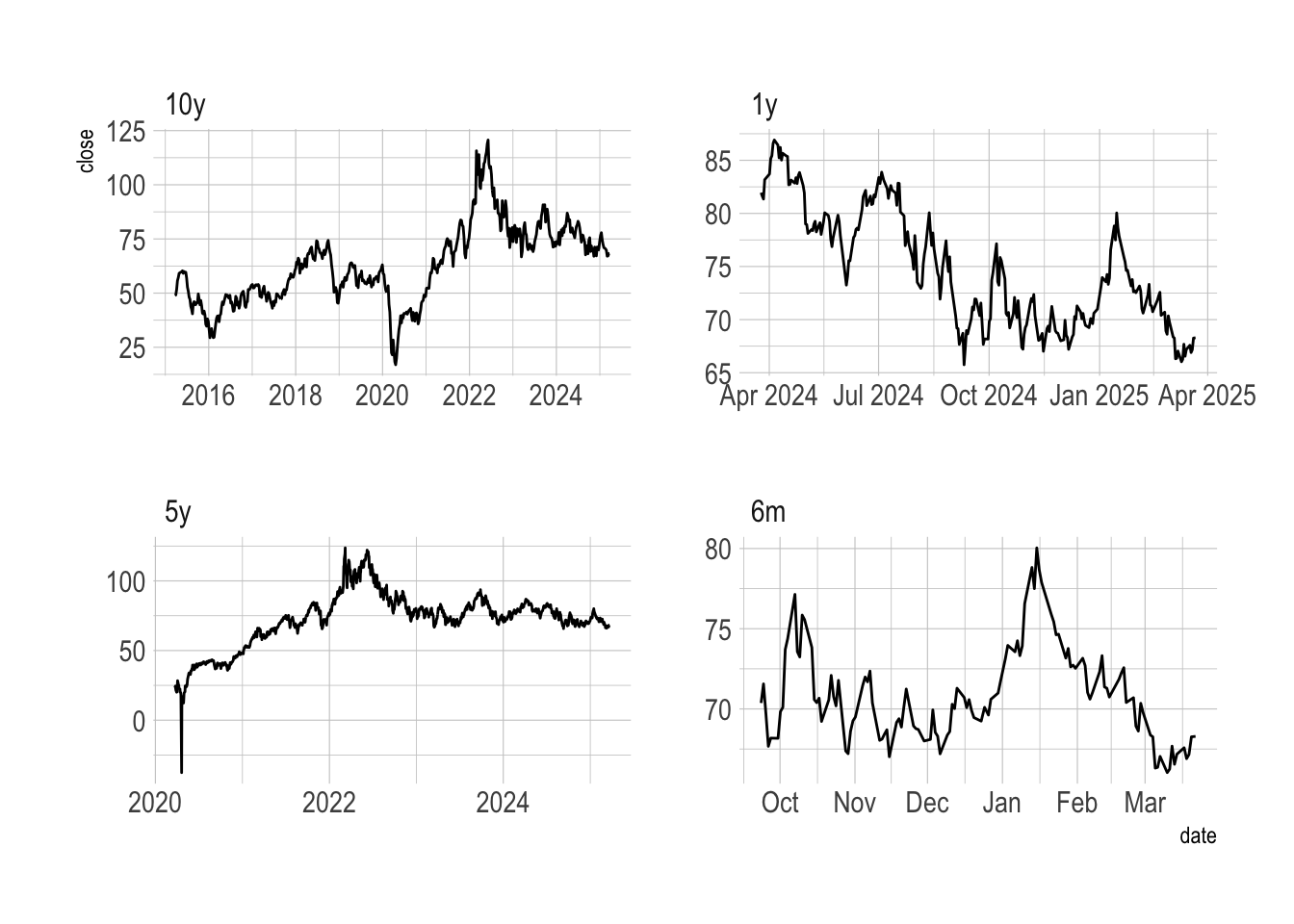

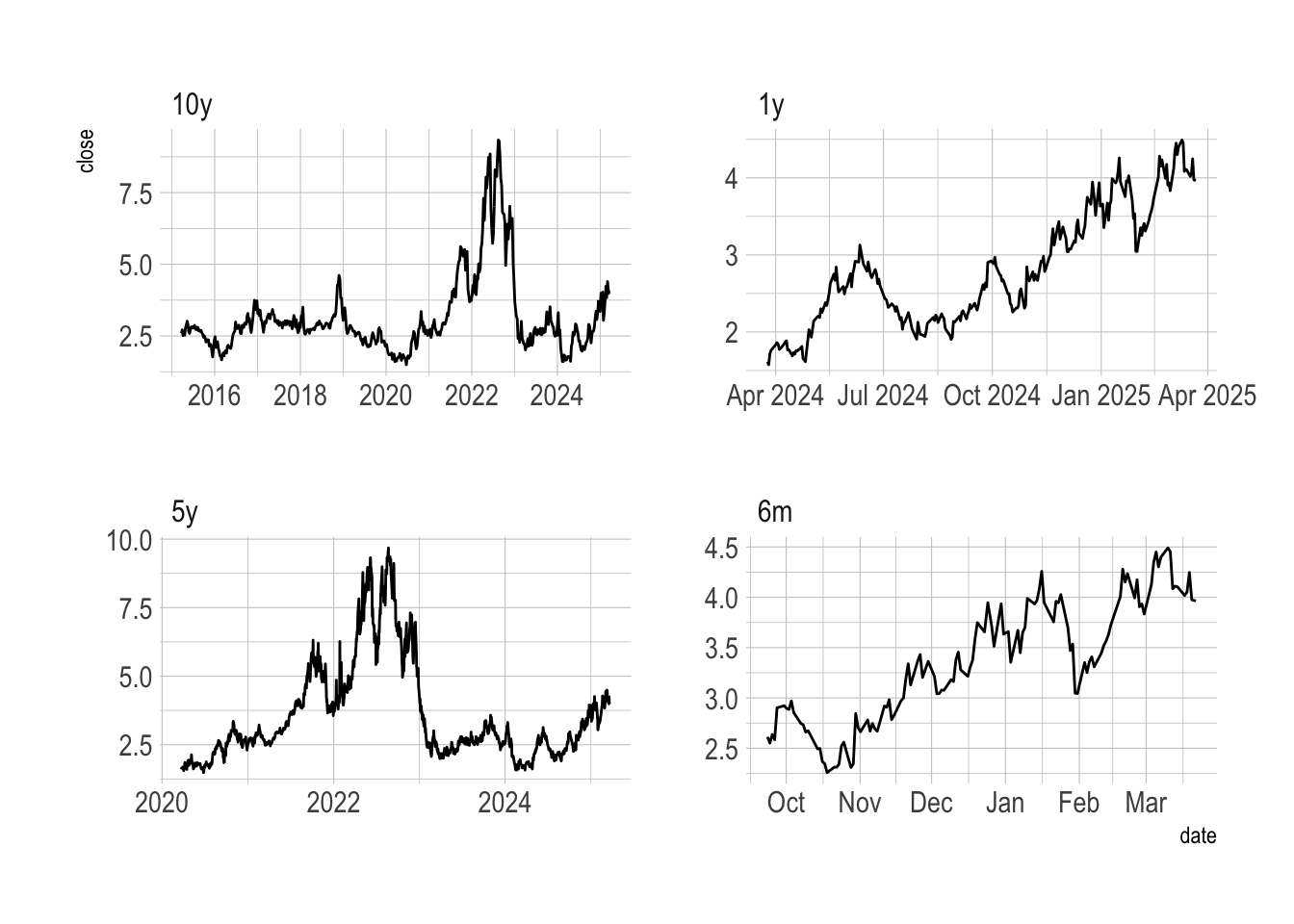

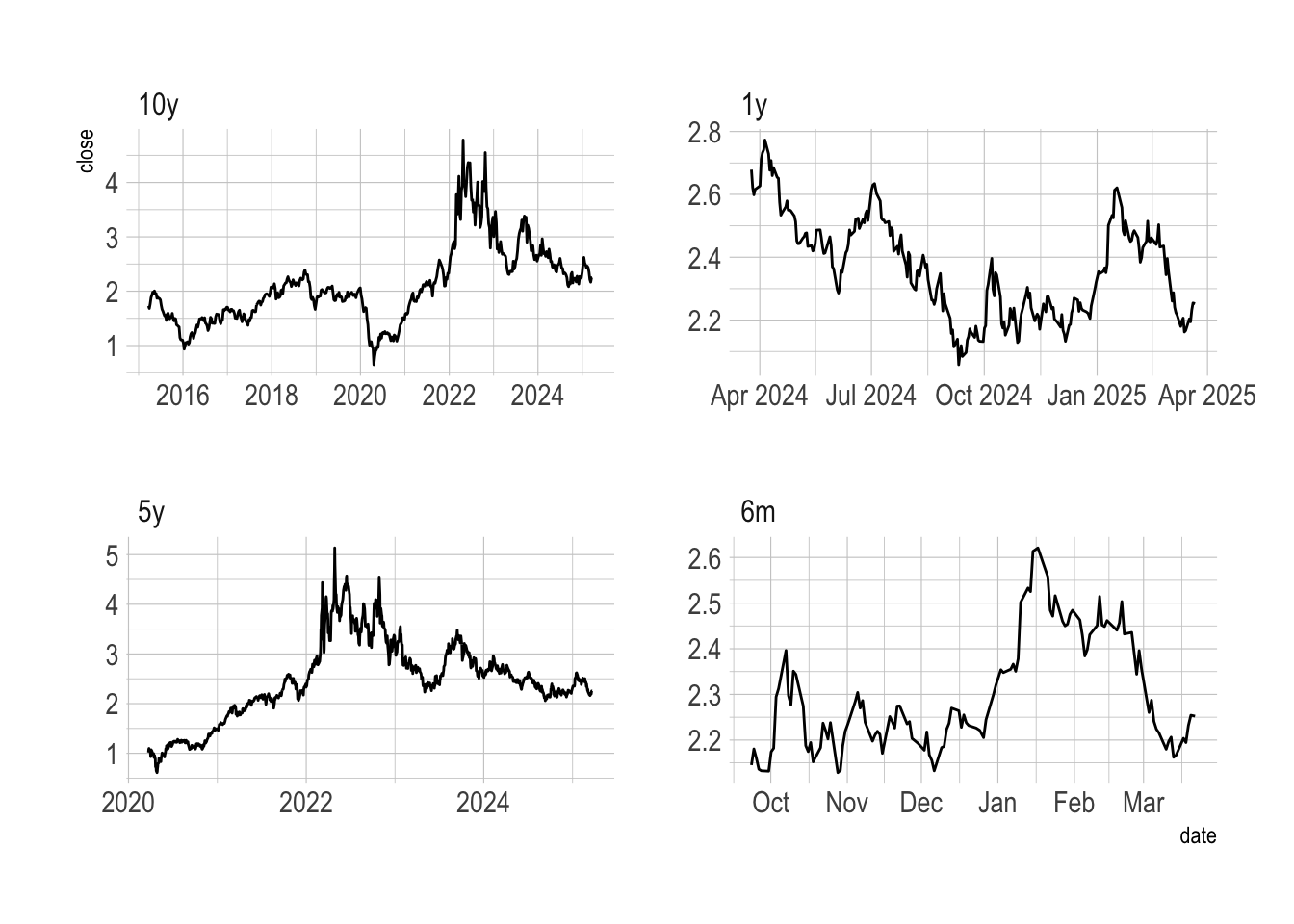

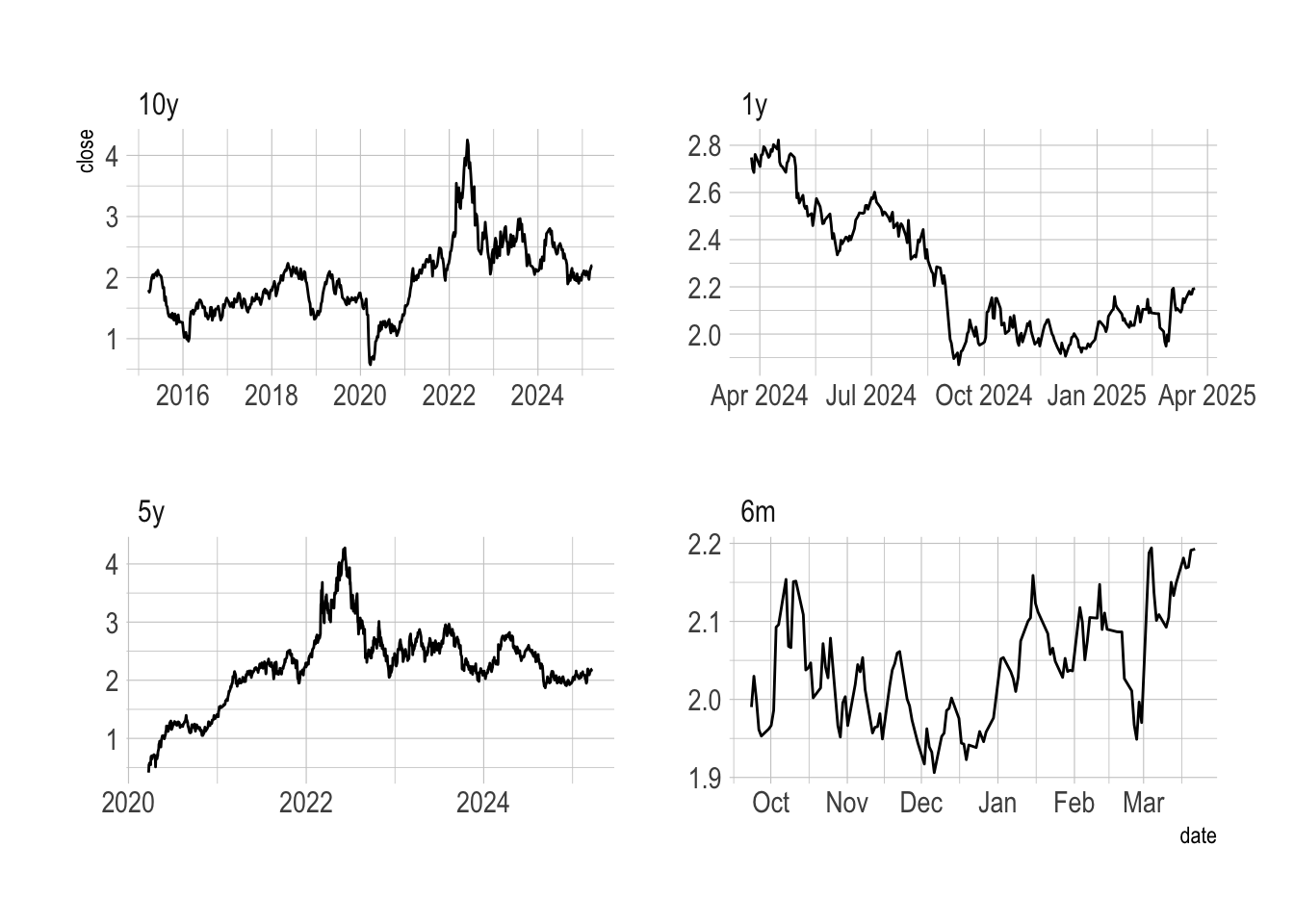

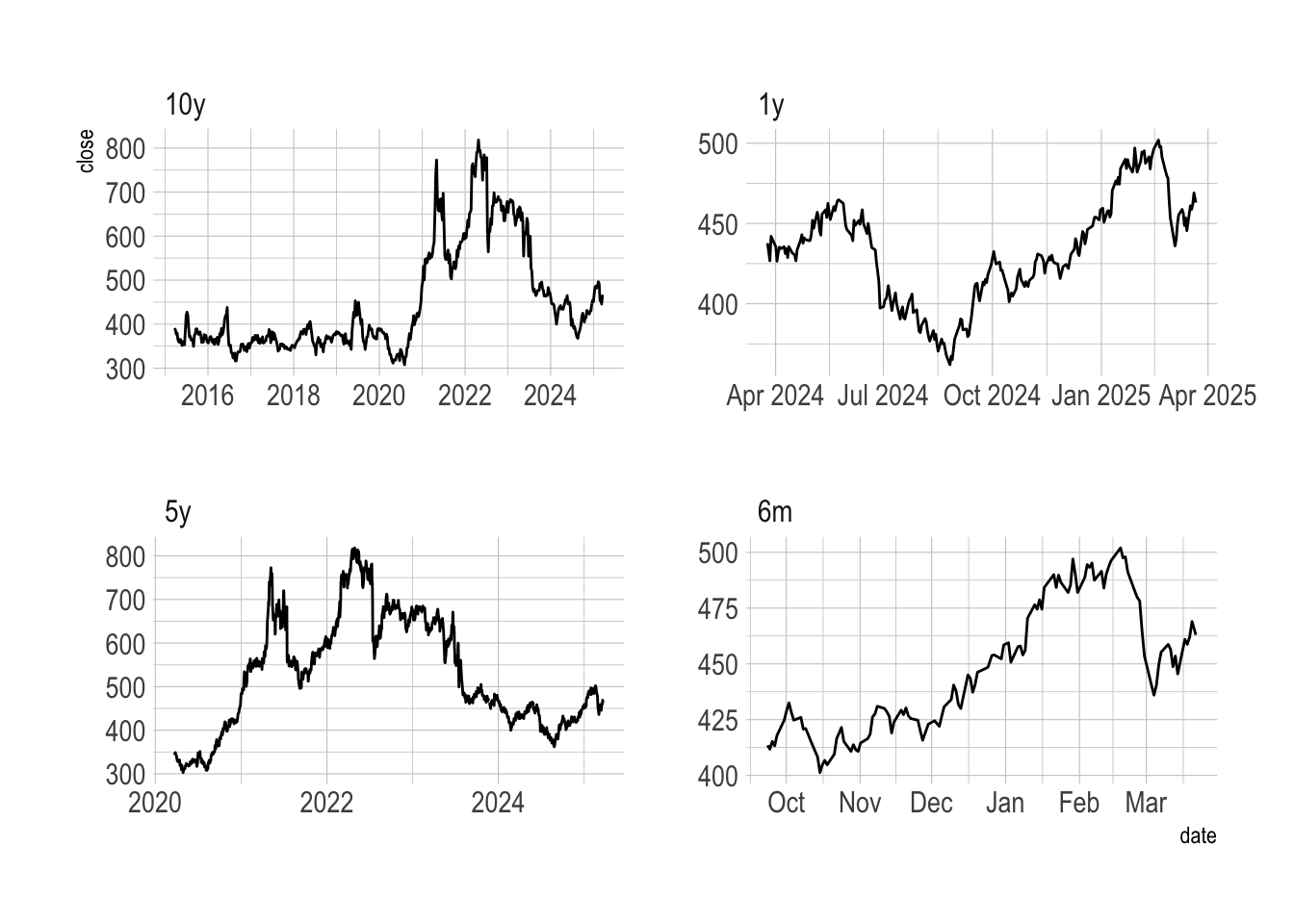

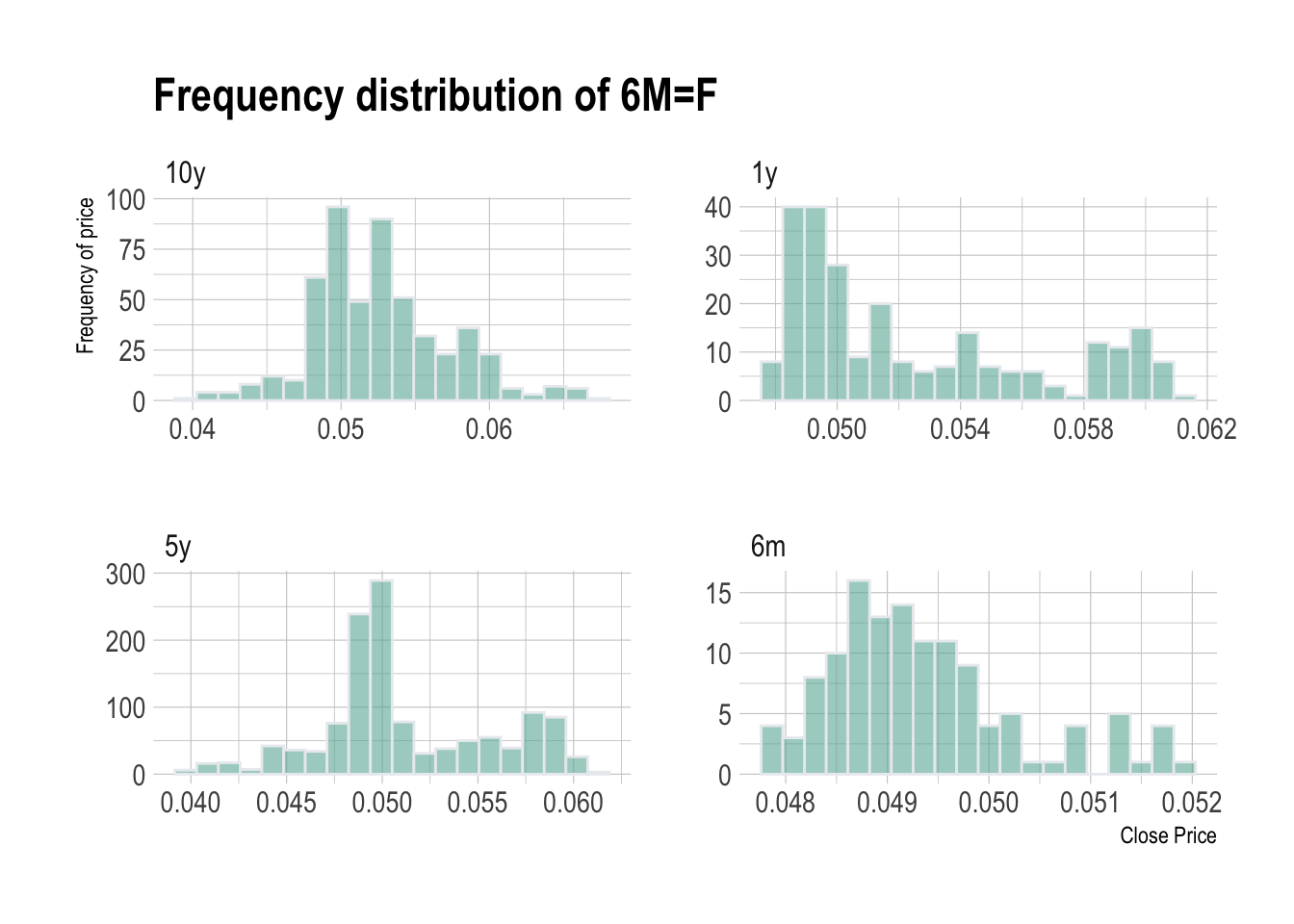

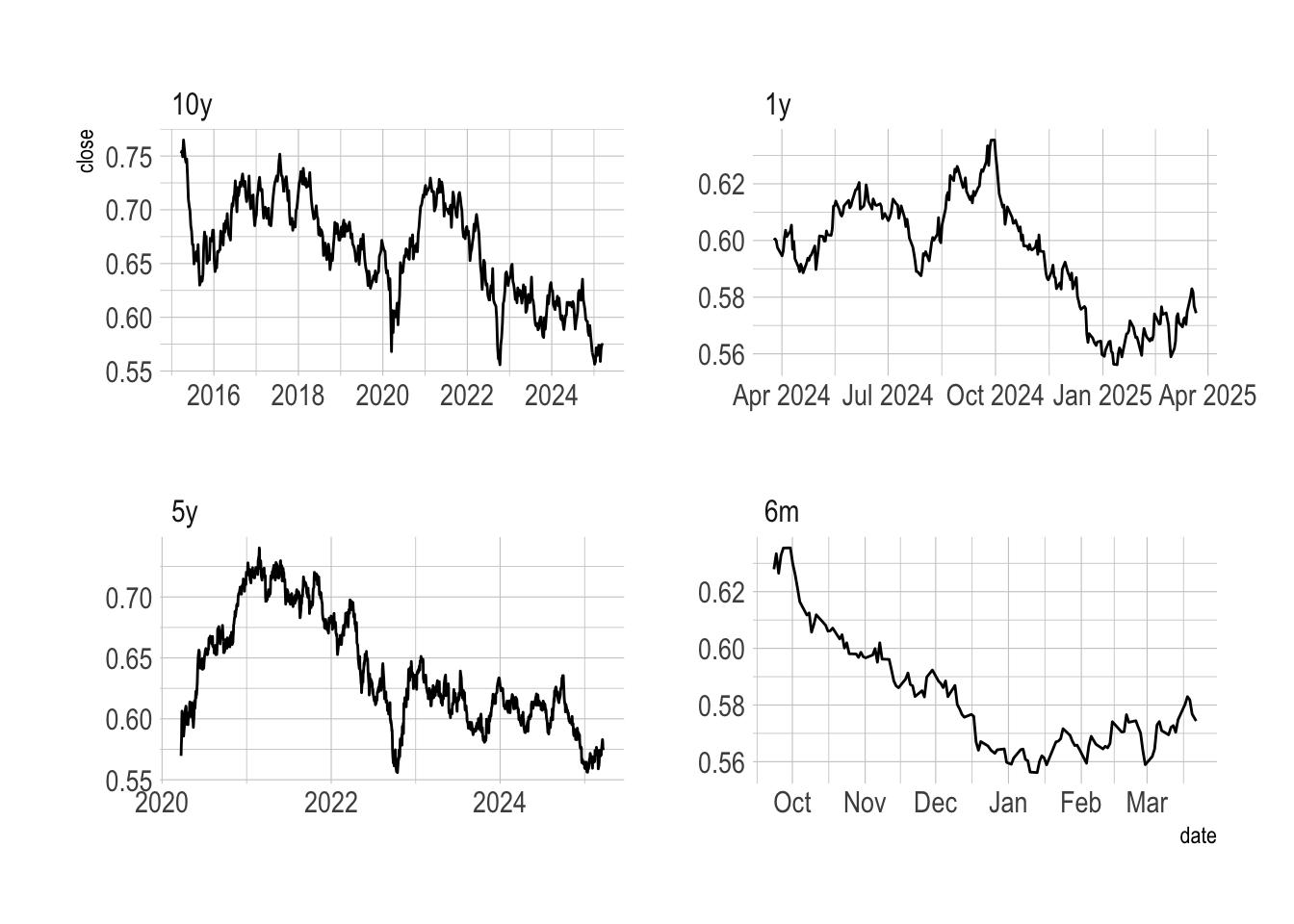

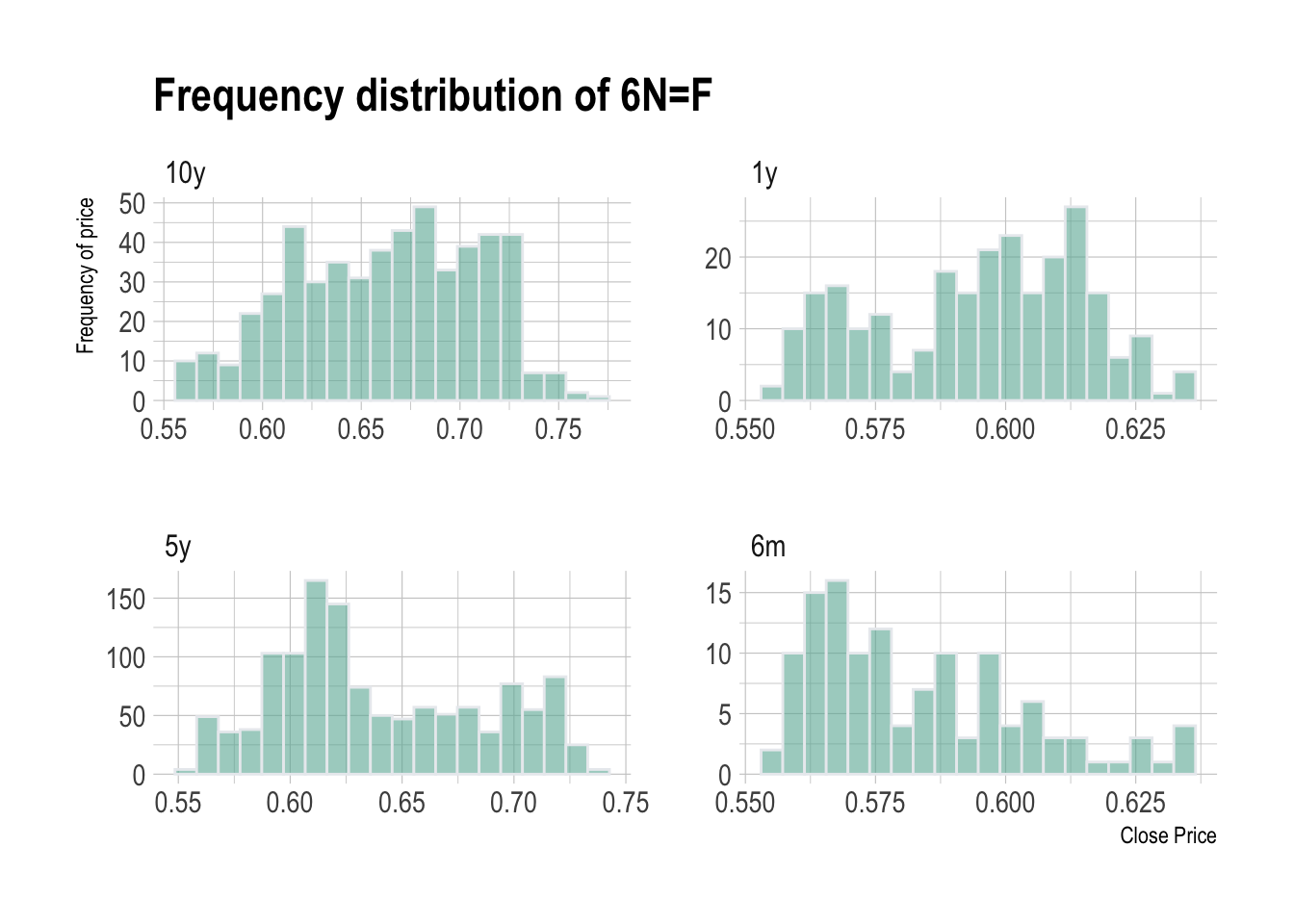

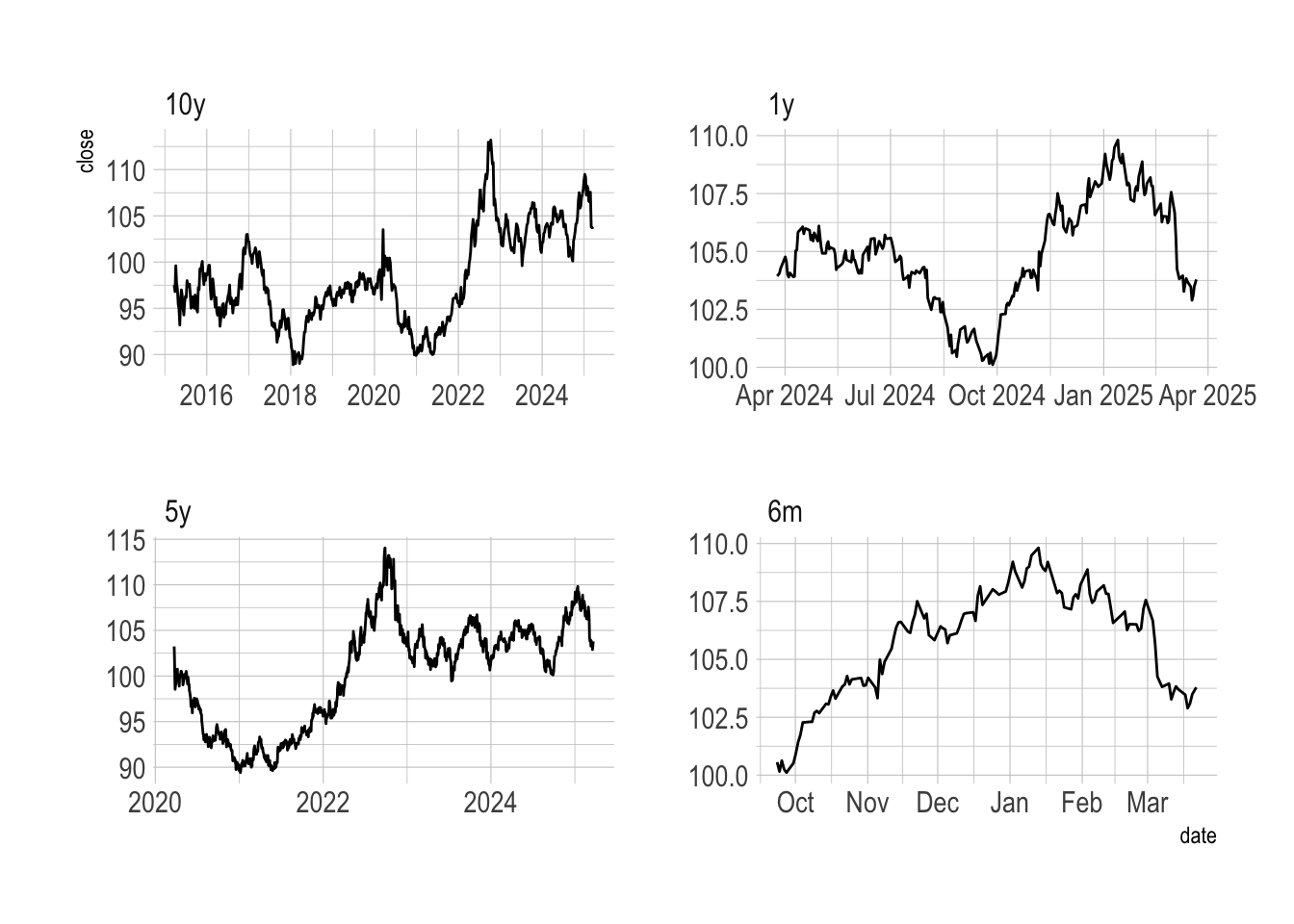

1-month (30-day) closing price histogram - Day bar

1-year closing price histogram - Day bar

5-year closing price histogram - Week bar

10-year closing price histogram - Week bar

1.1 Selection of ETFs

My goal is to cover all the asset classes with either ETFs or futures. My selection are as follow:

Equity:

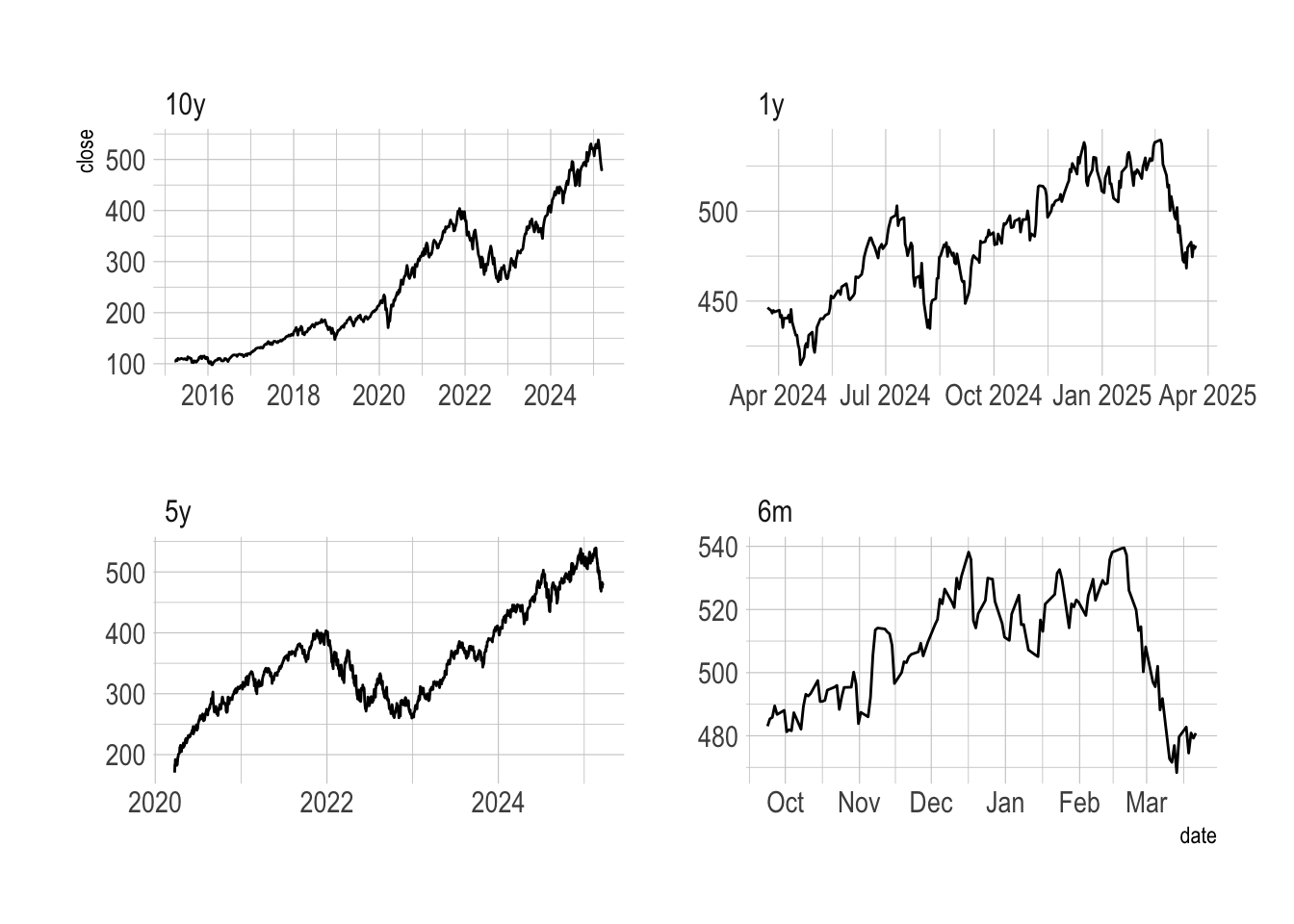

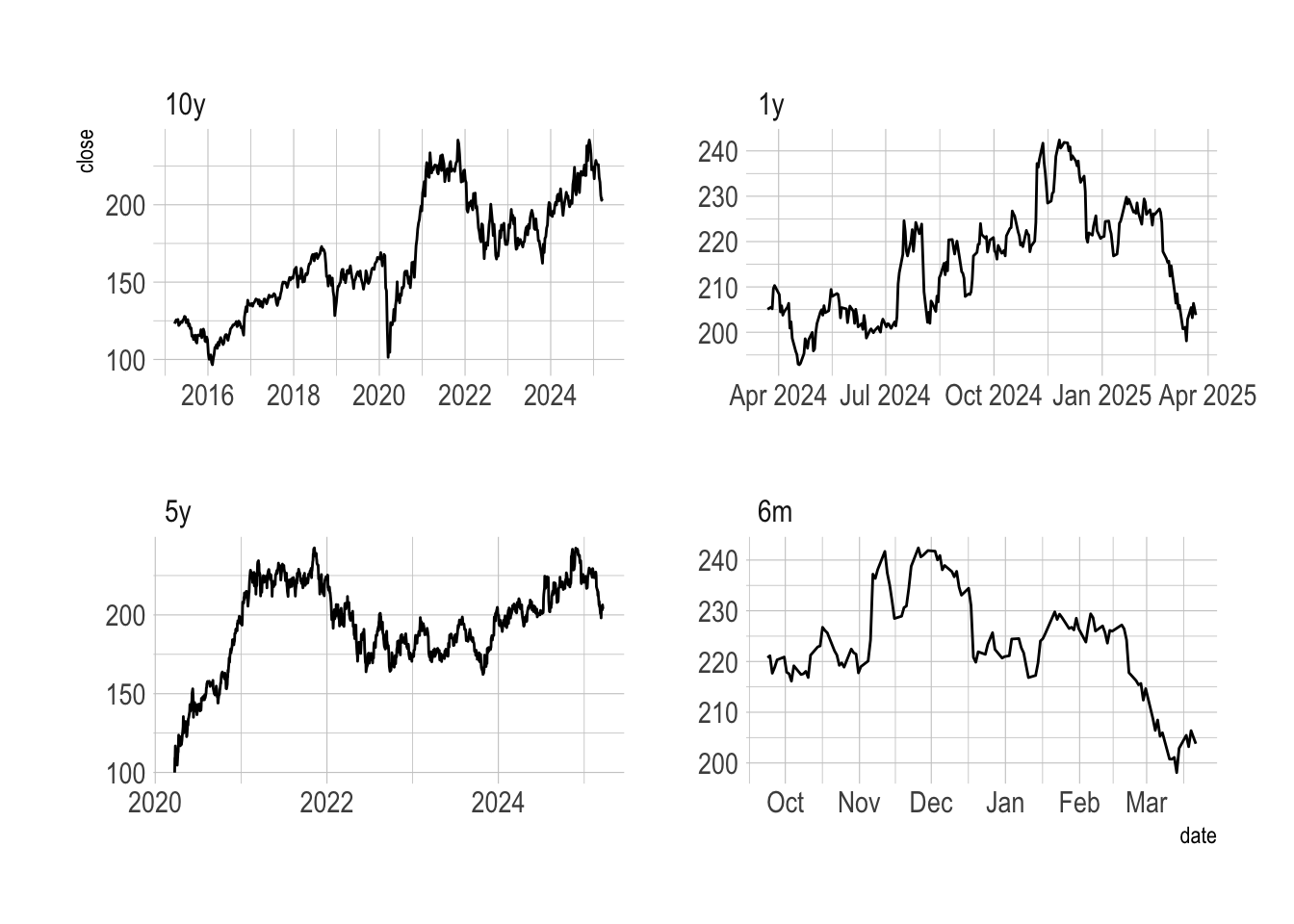

US: IYY, SPY, QQQ, IWM

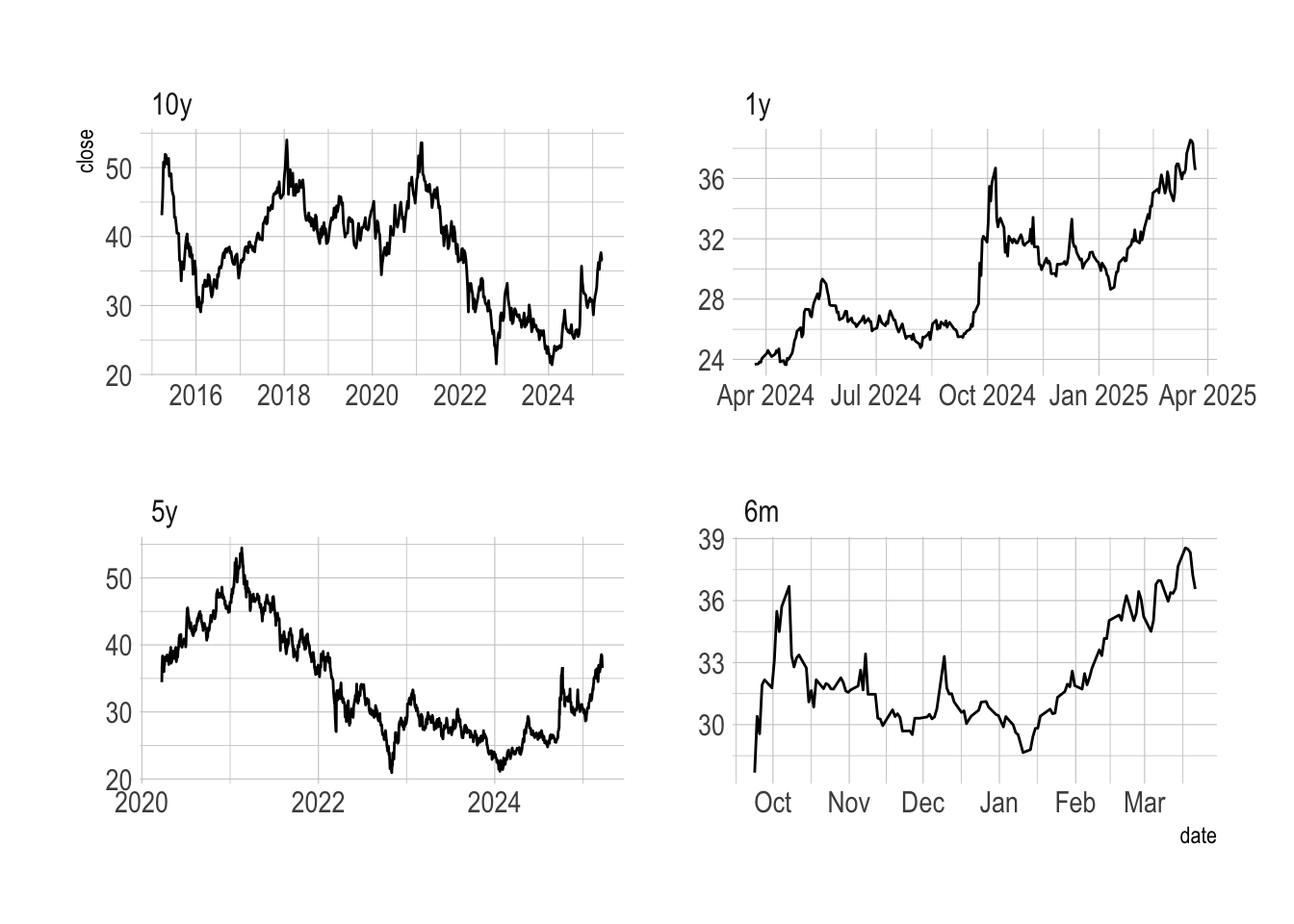

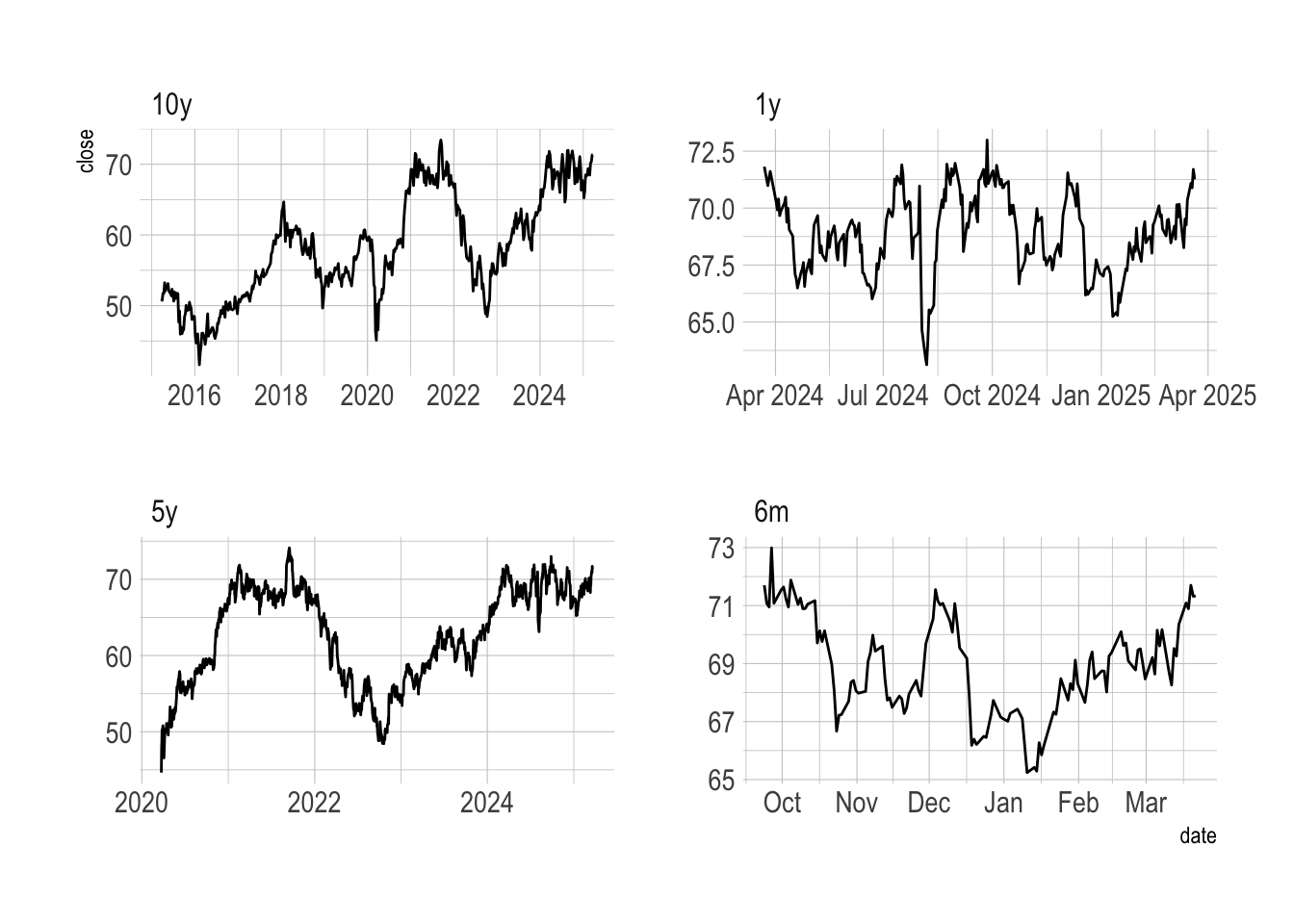

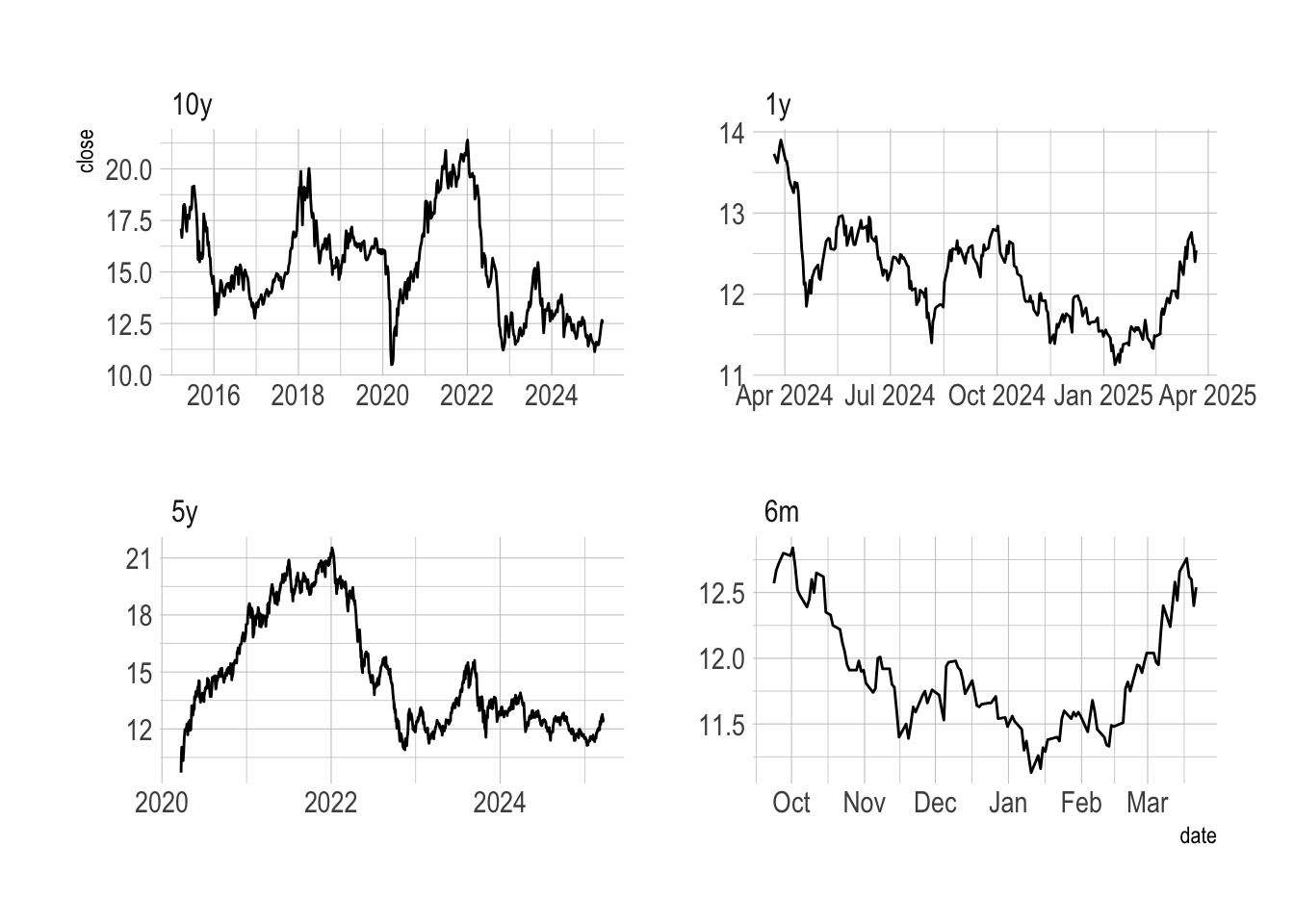

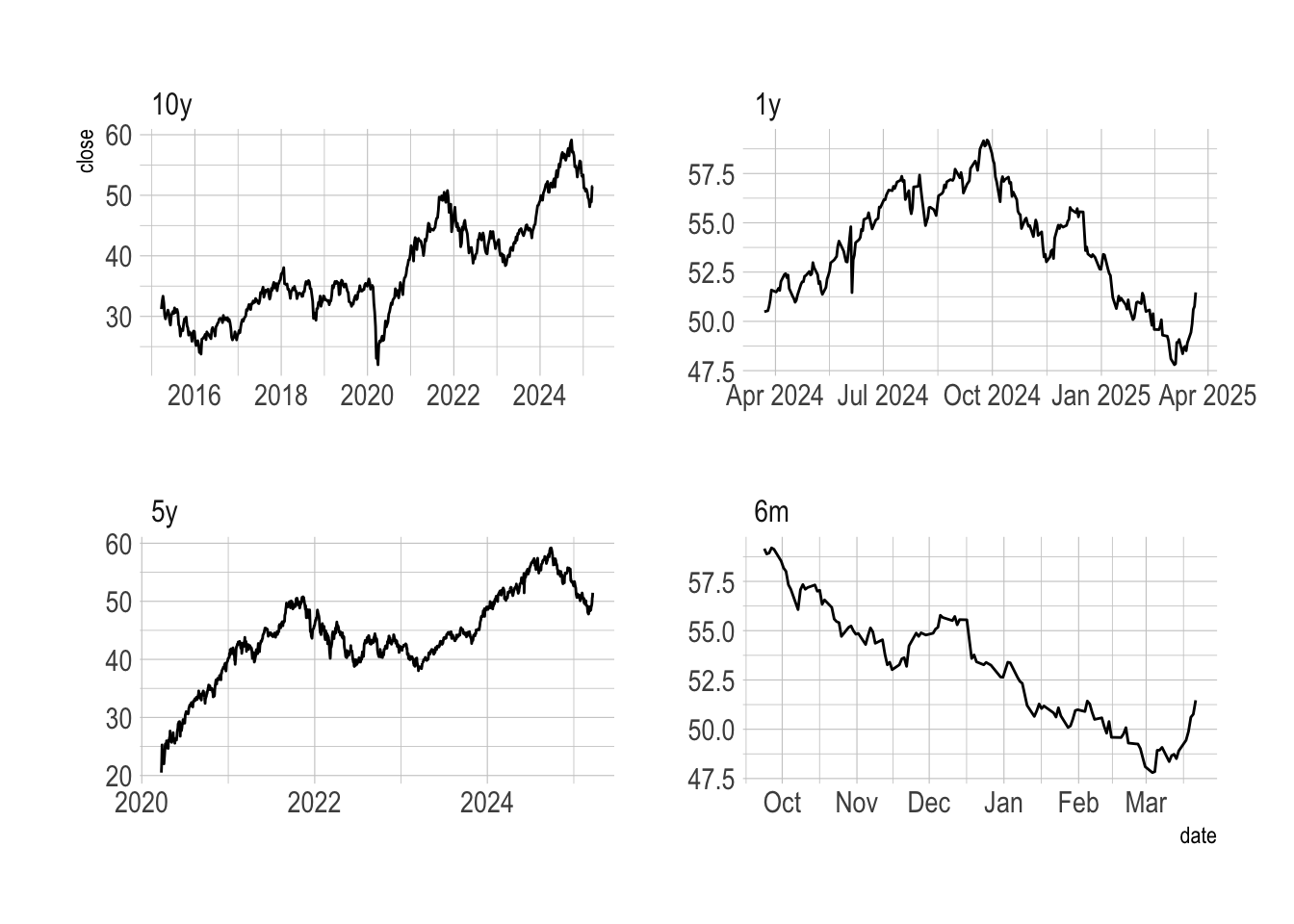

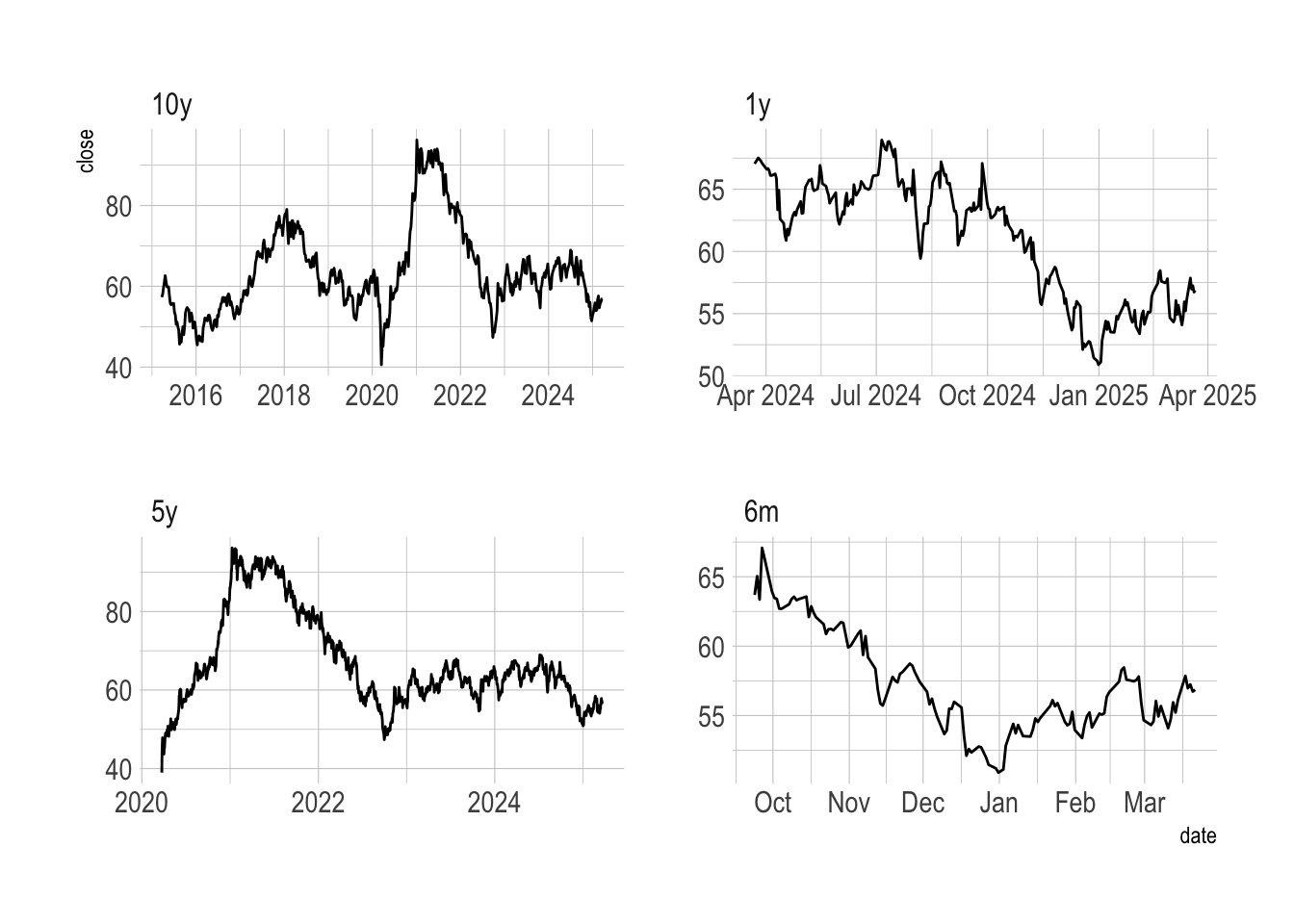

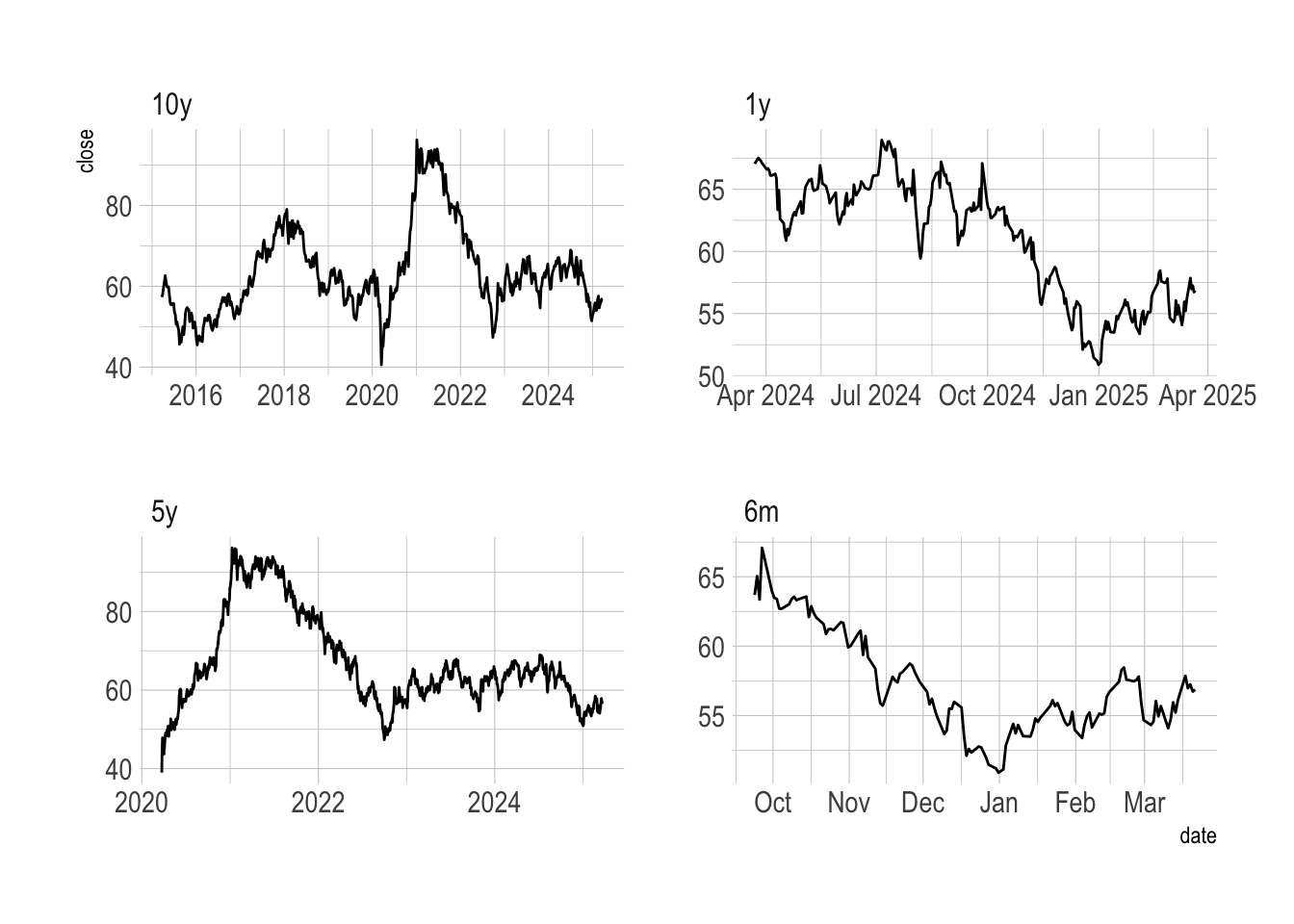

Asia: FXI, EWJ, VNM, INDA, EWY, EWT

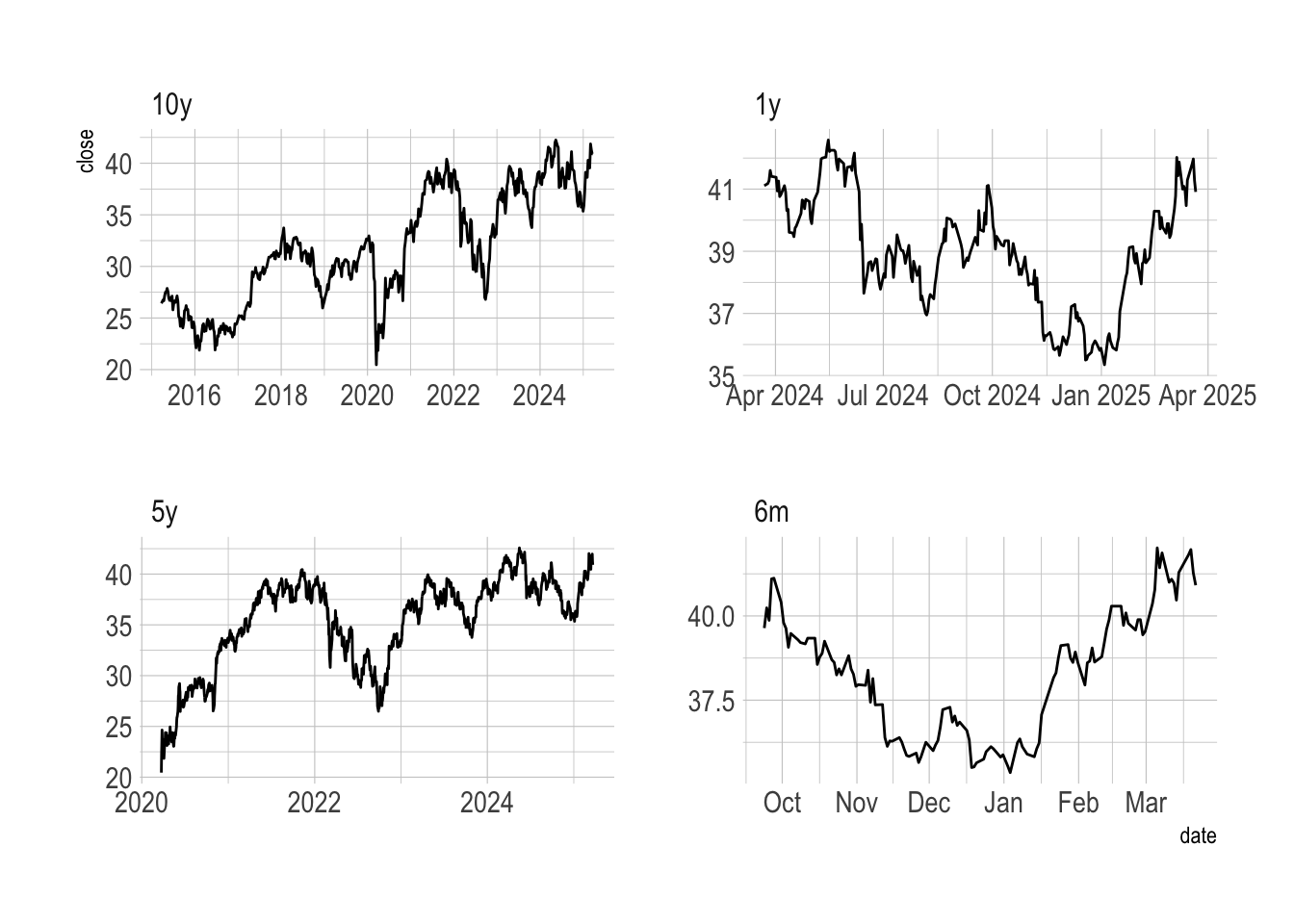

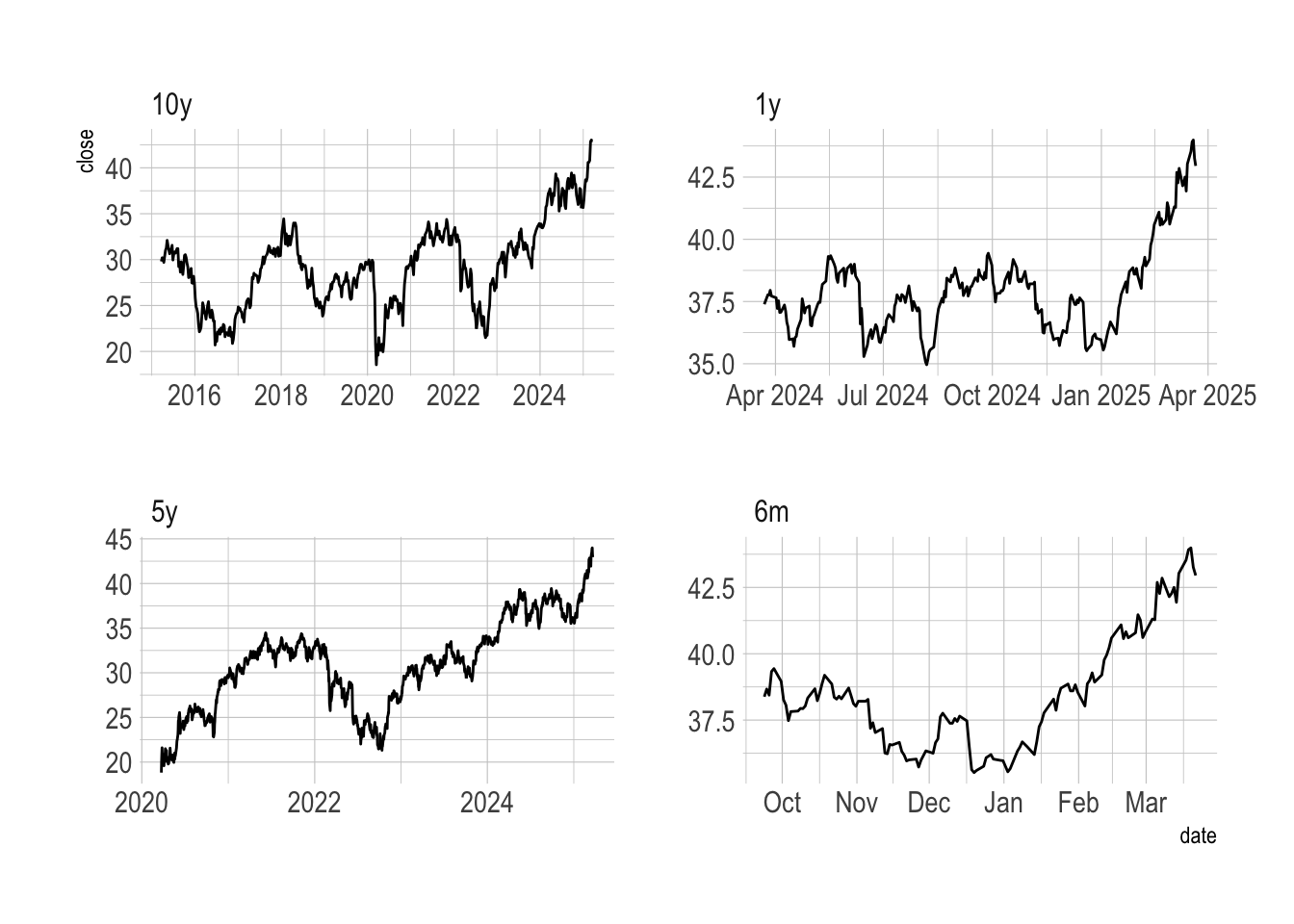

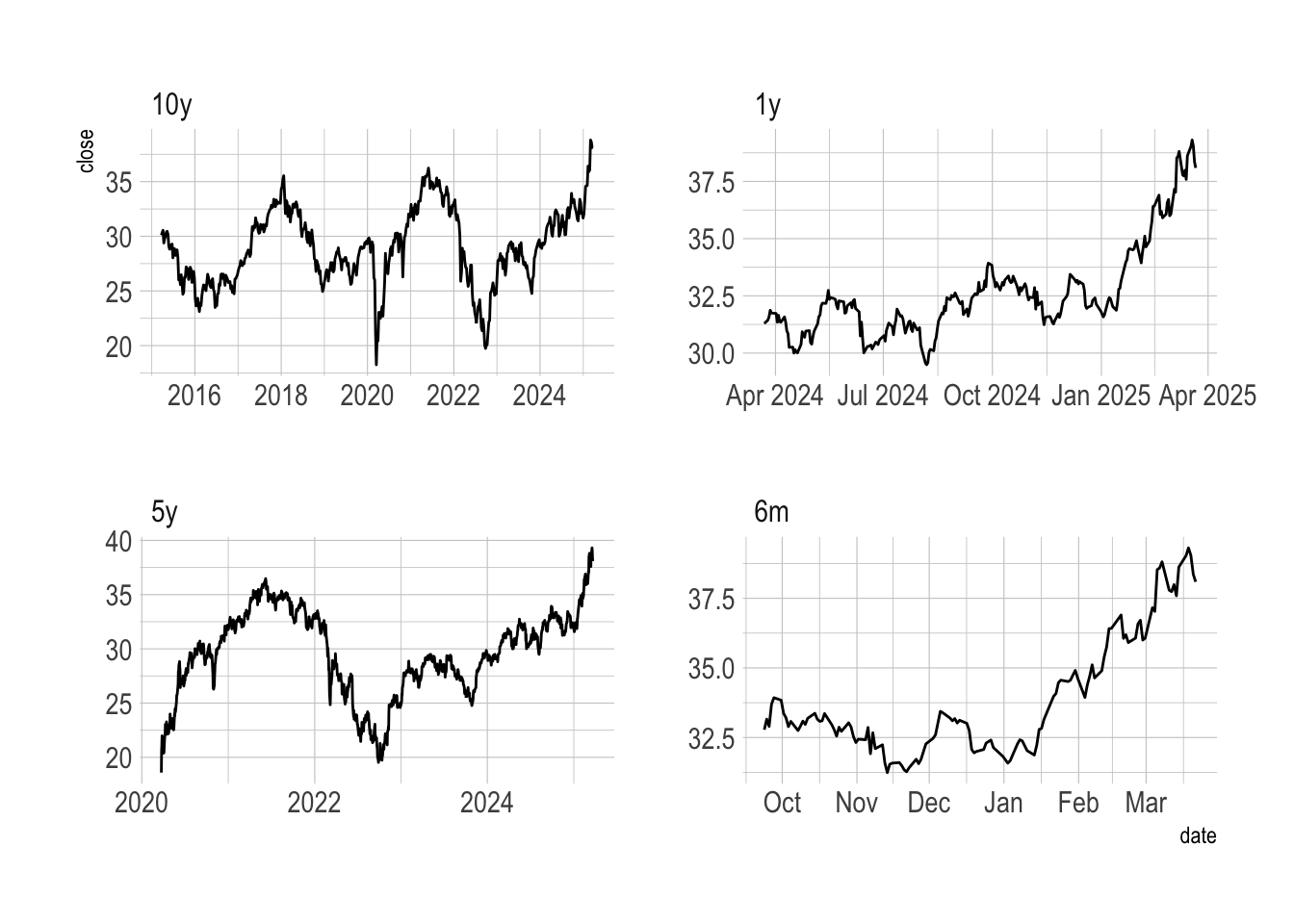

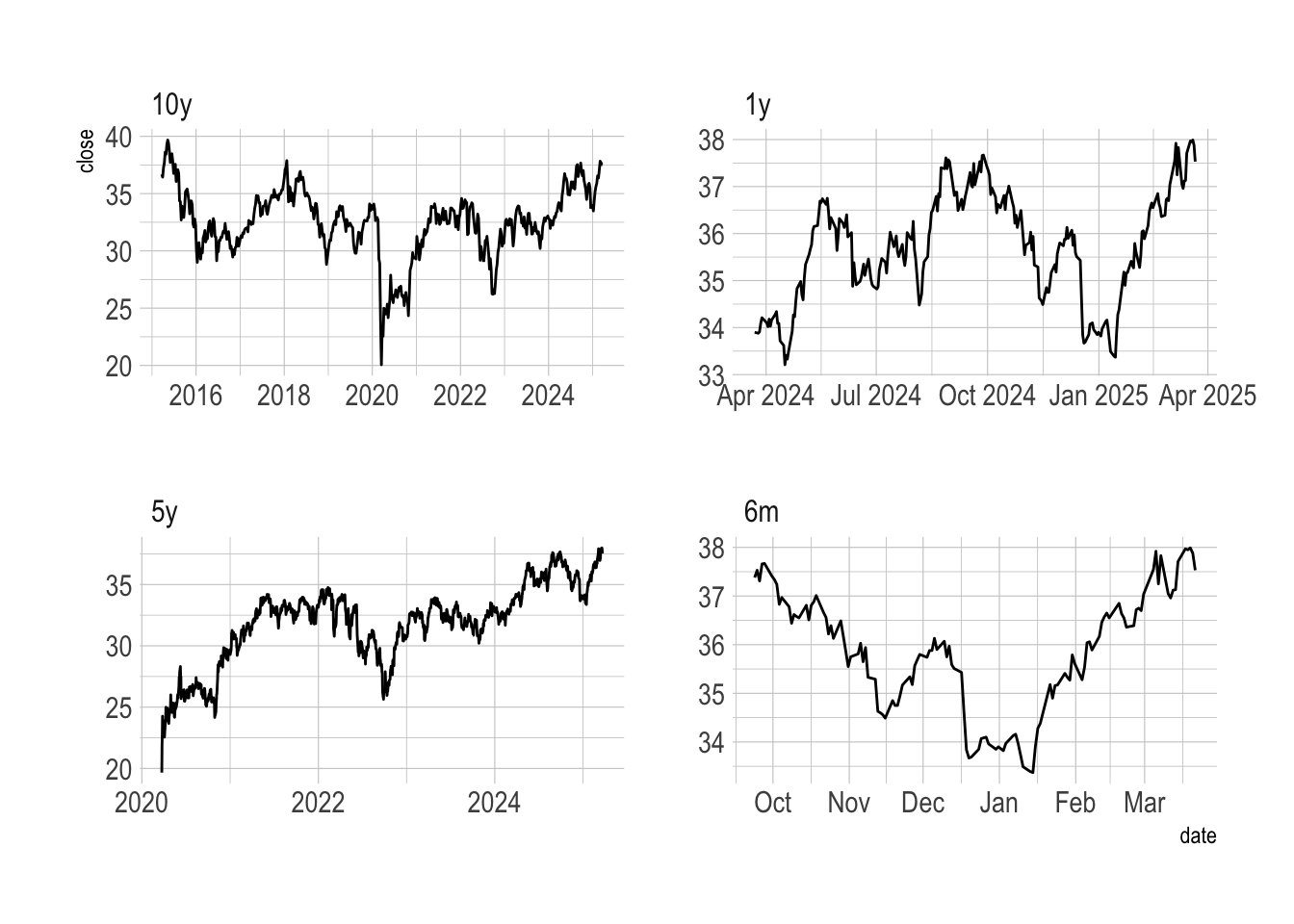

Europe: EWQ, EWI, EWG, EWU

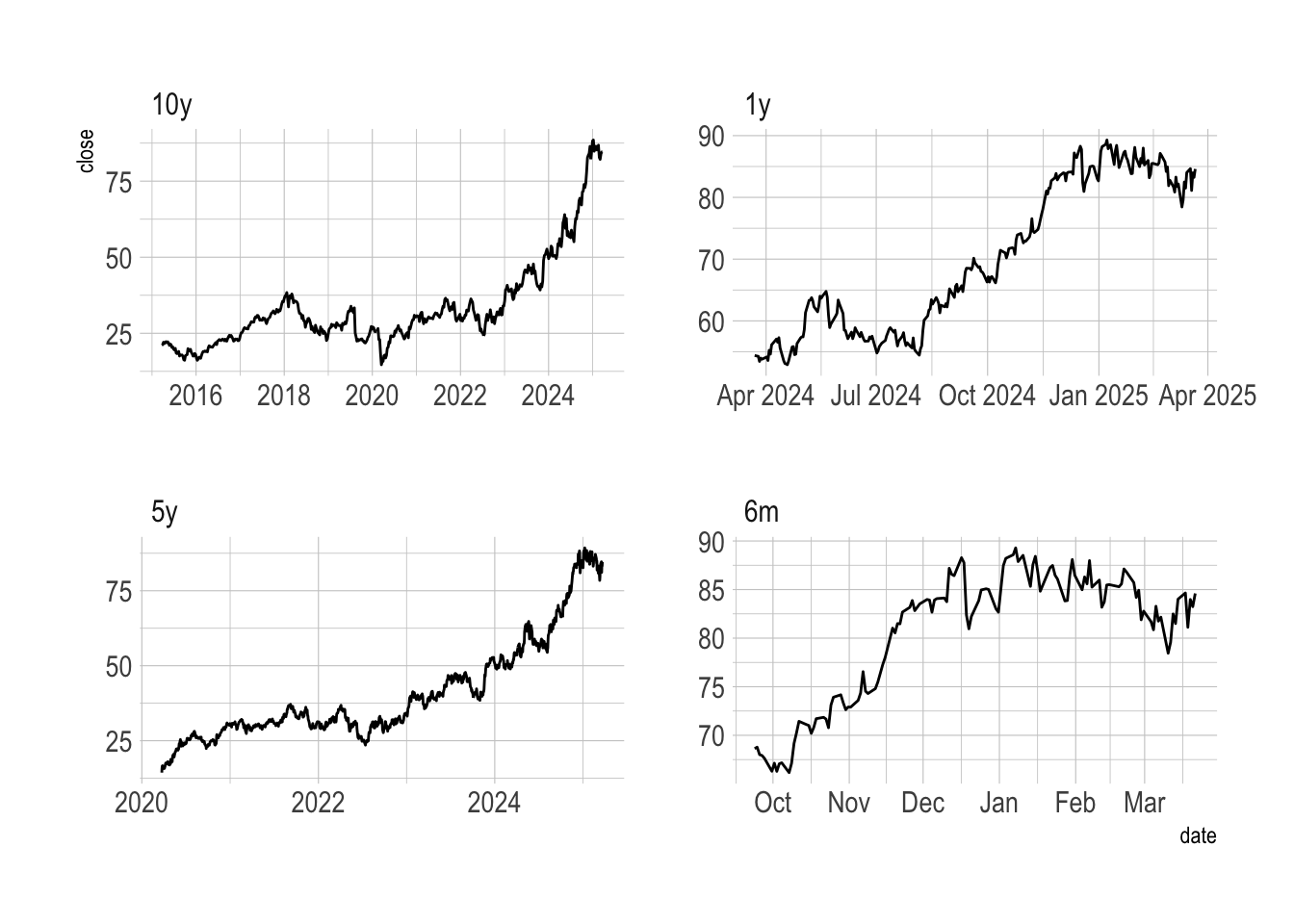

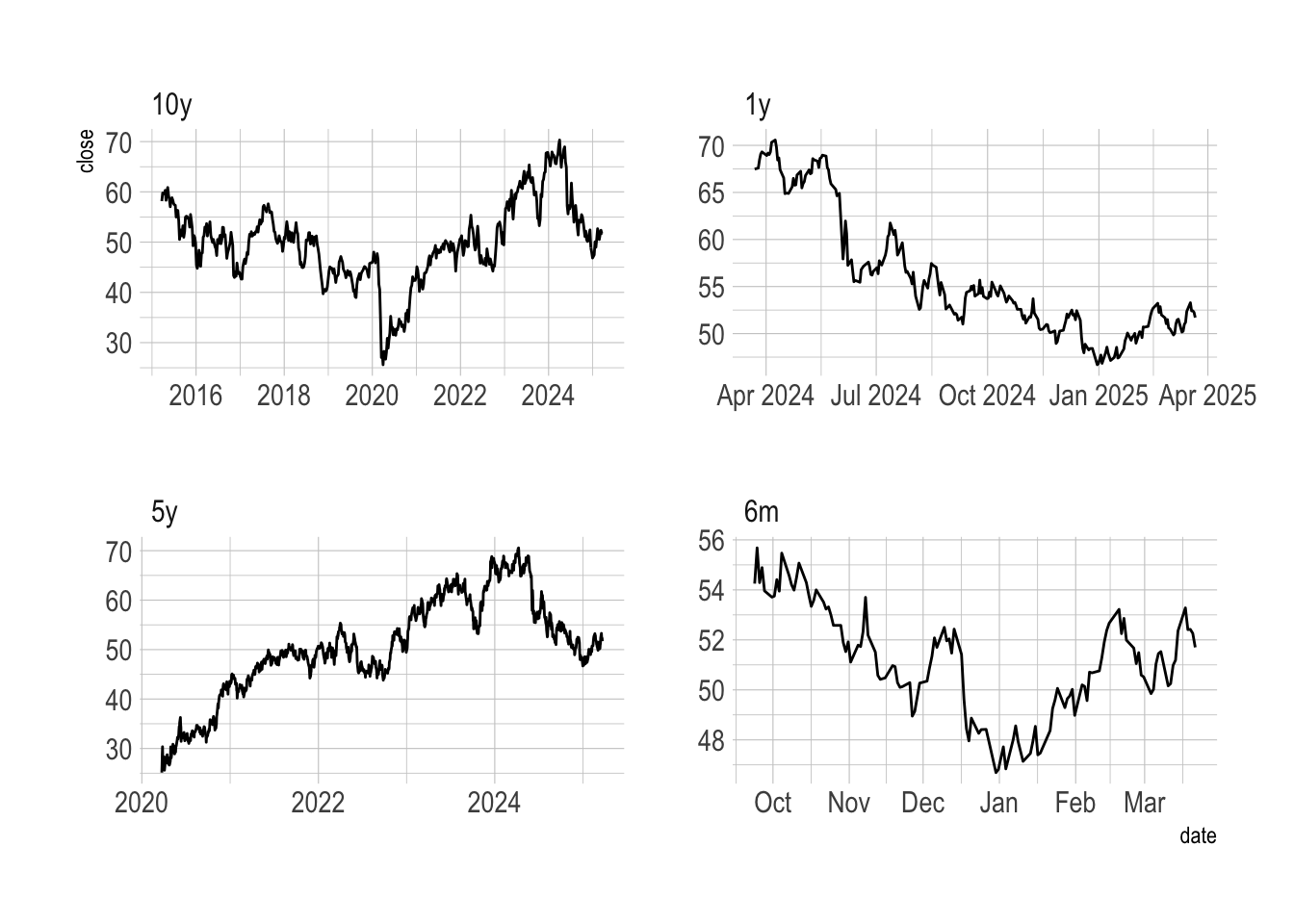

South America: ARGT, EWW, EWZ

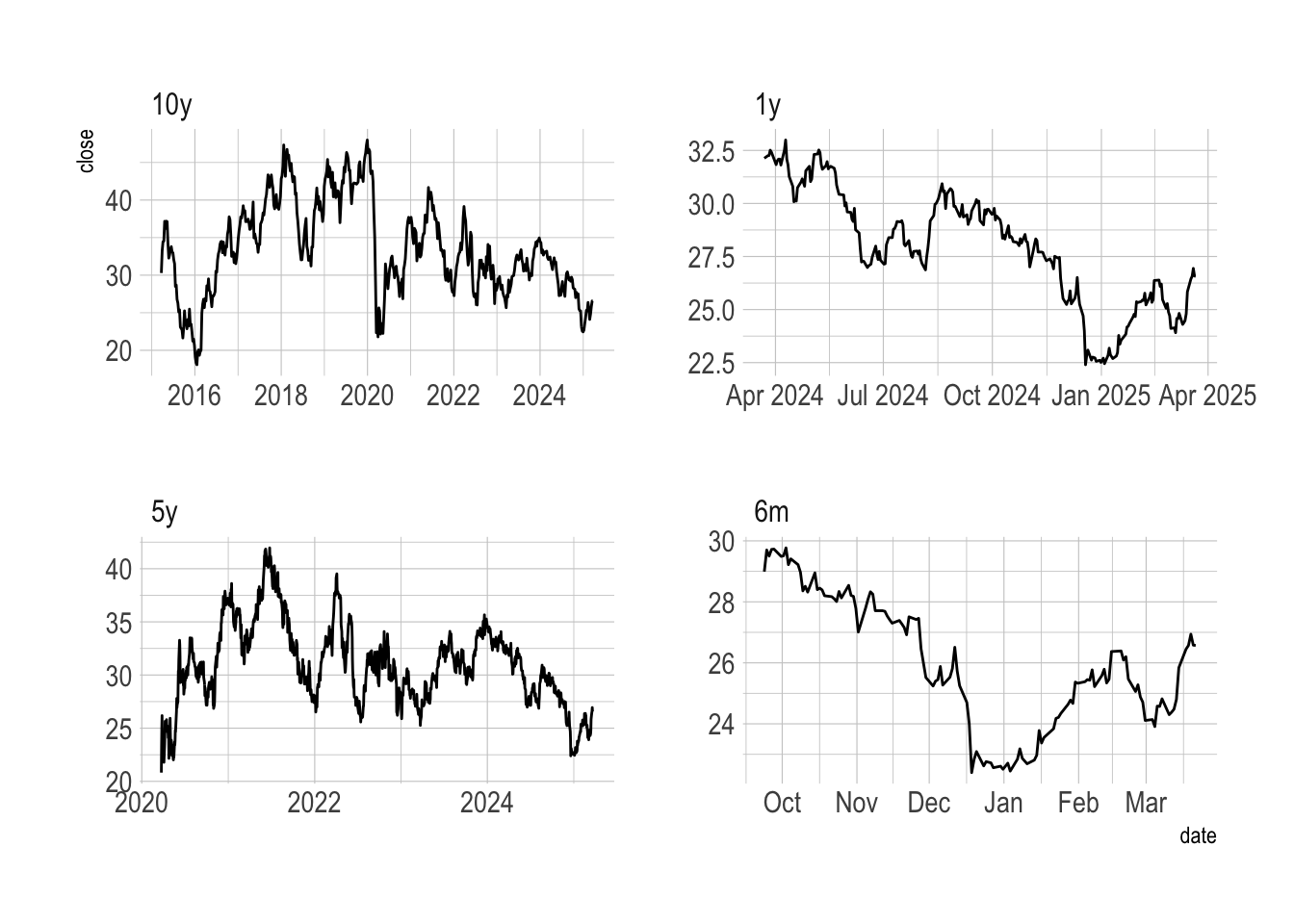

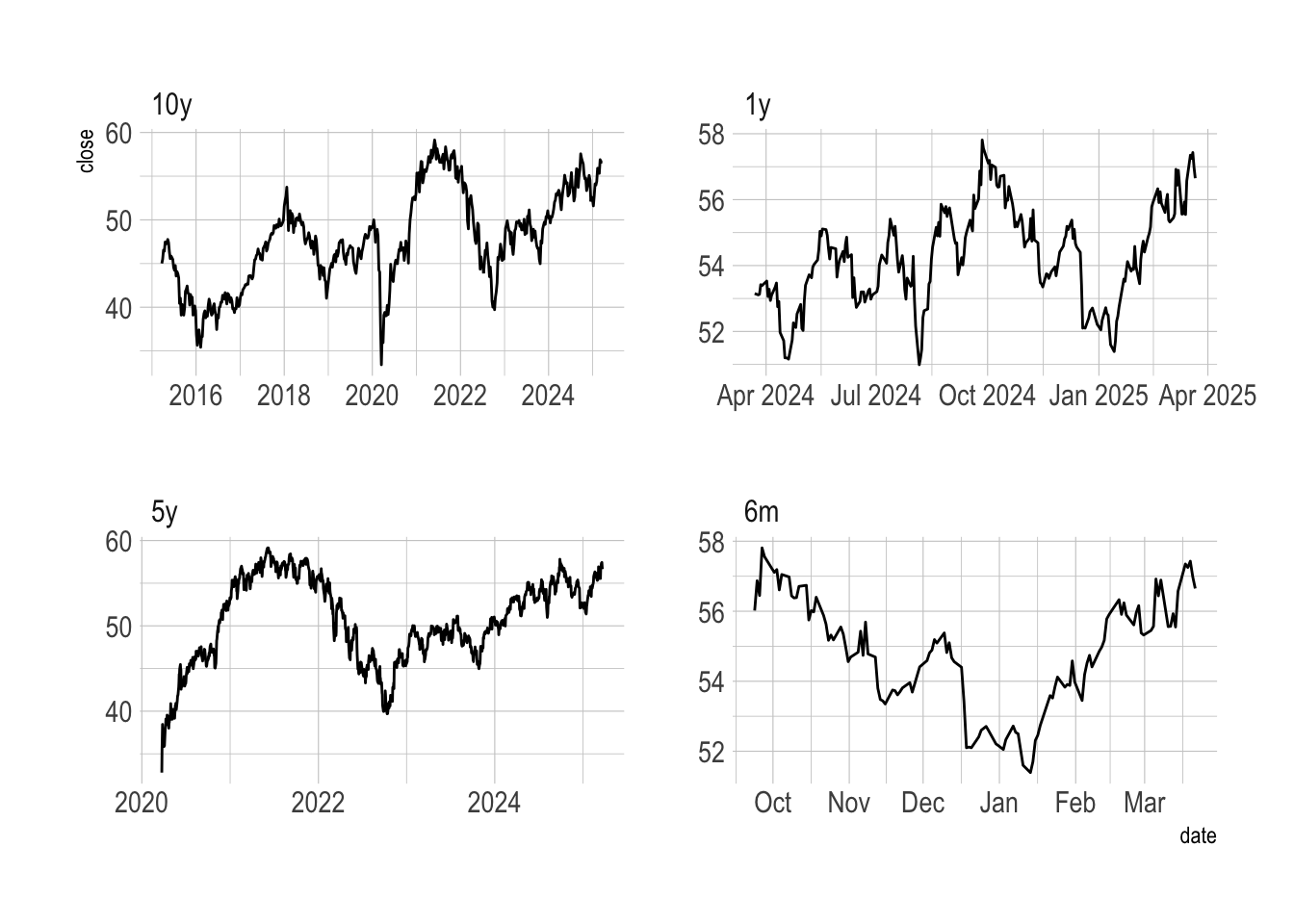

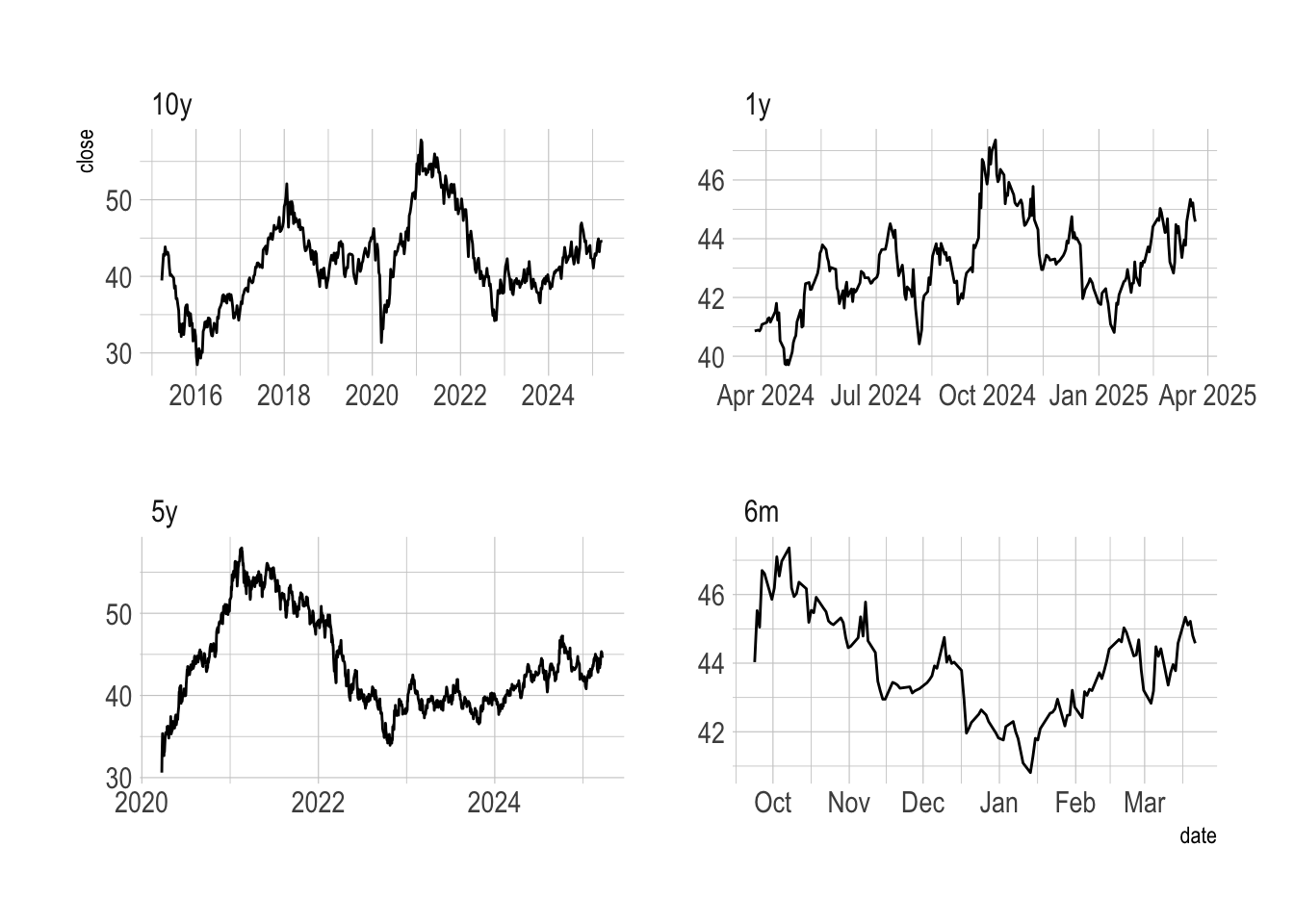

Emerging markets: ACWX, EEM

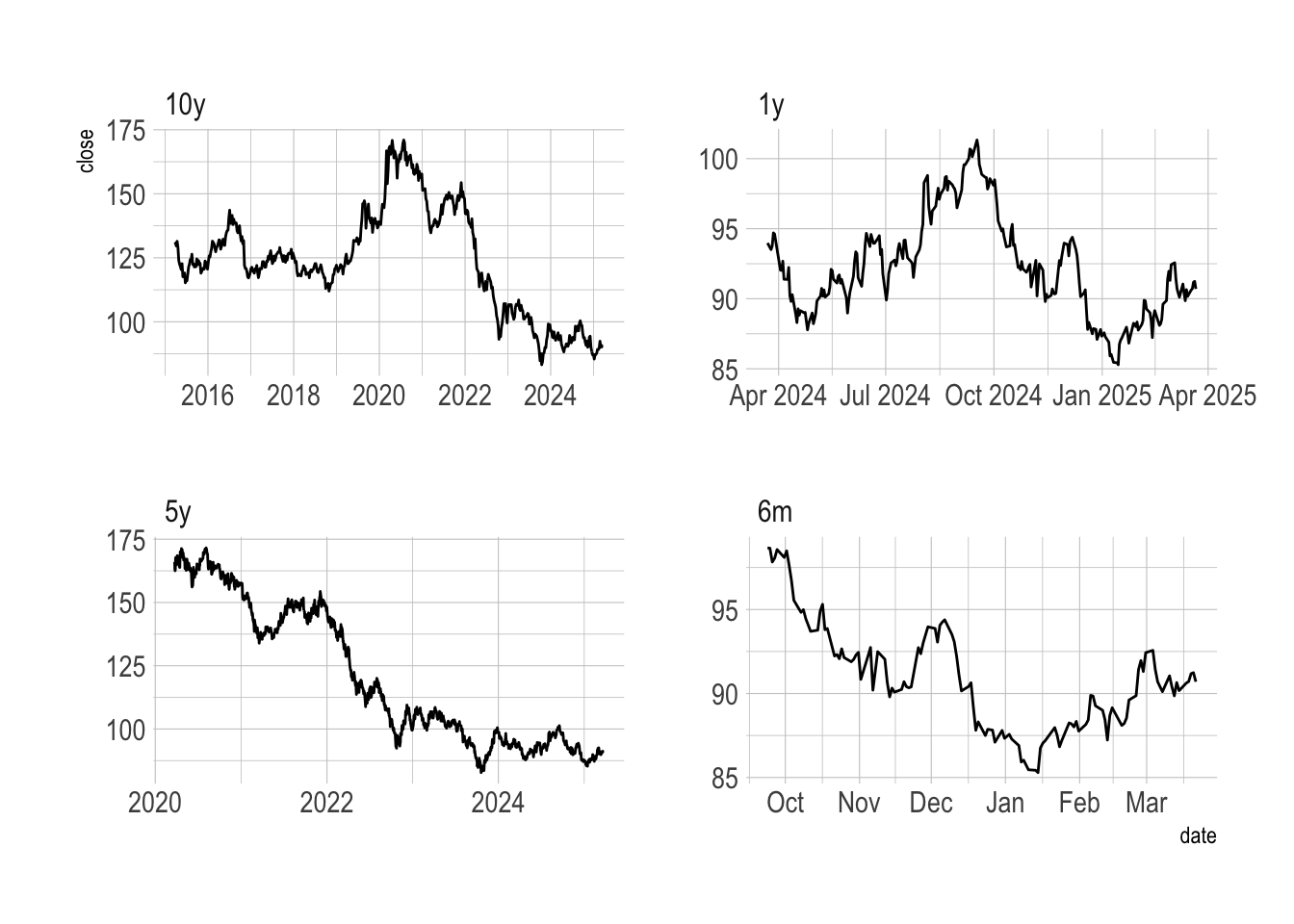

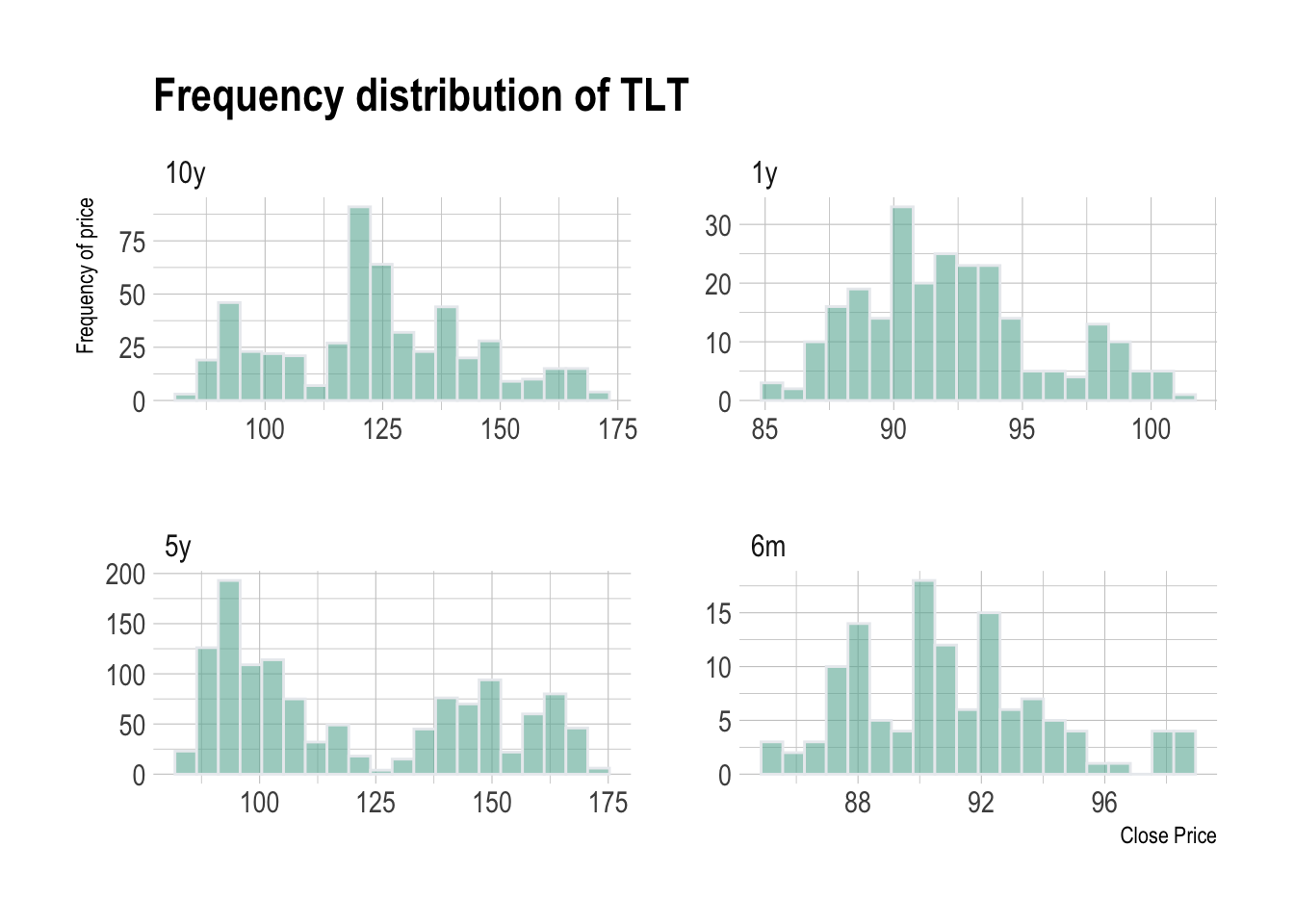

Bonds: SHY(1-3 years TBond), TLT (20+ Year Treasury Bond)

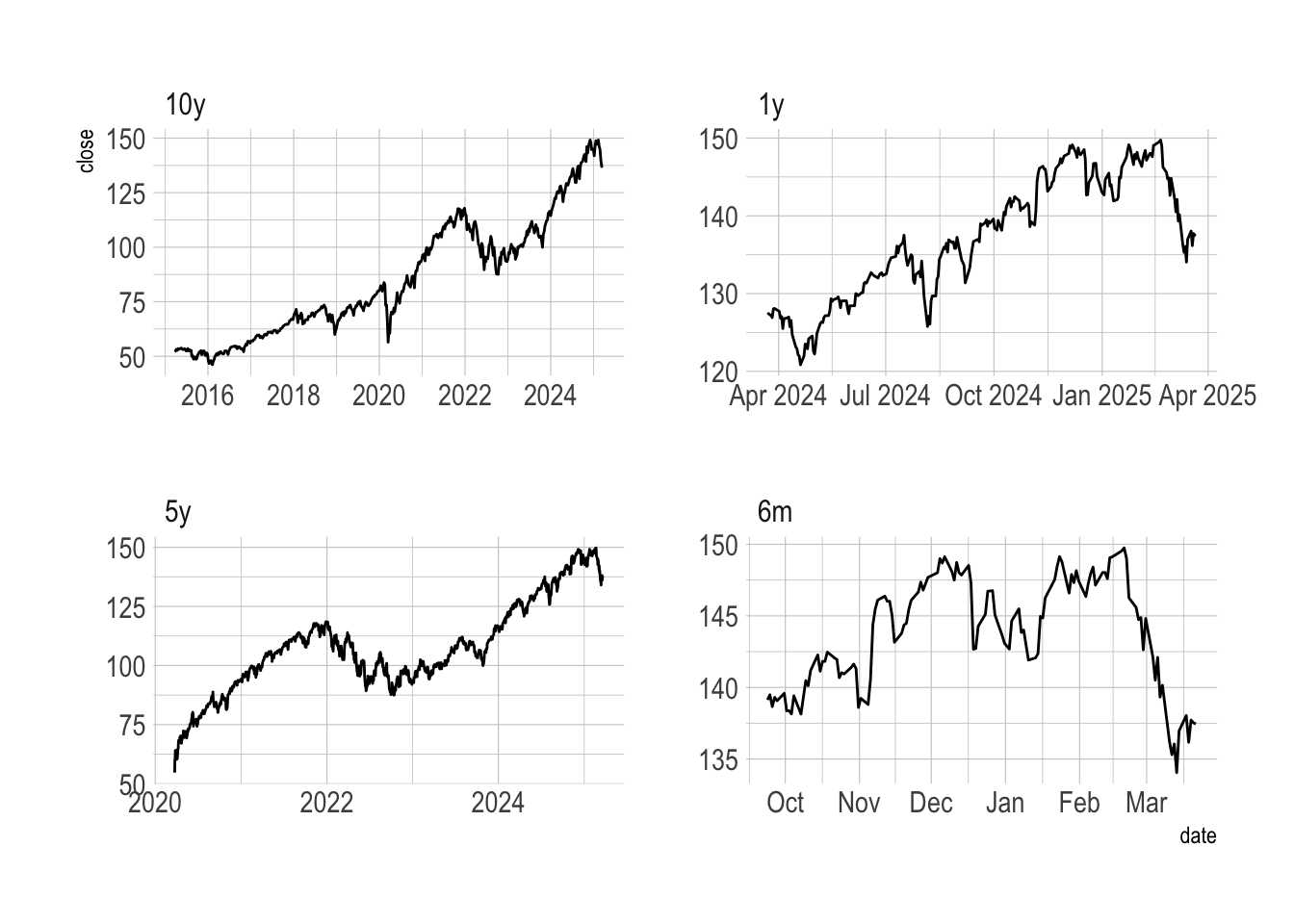

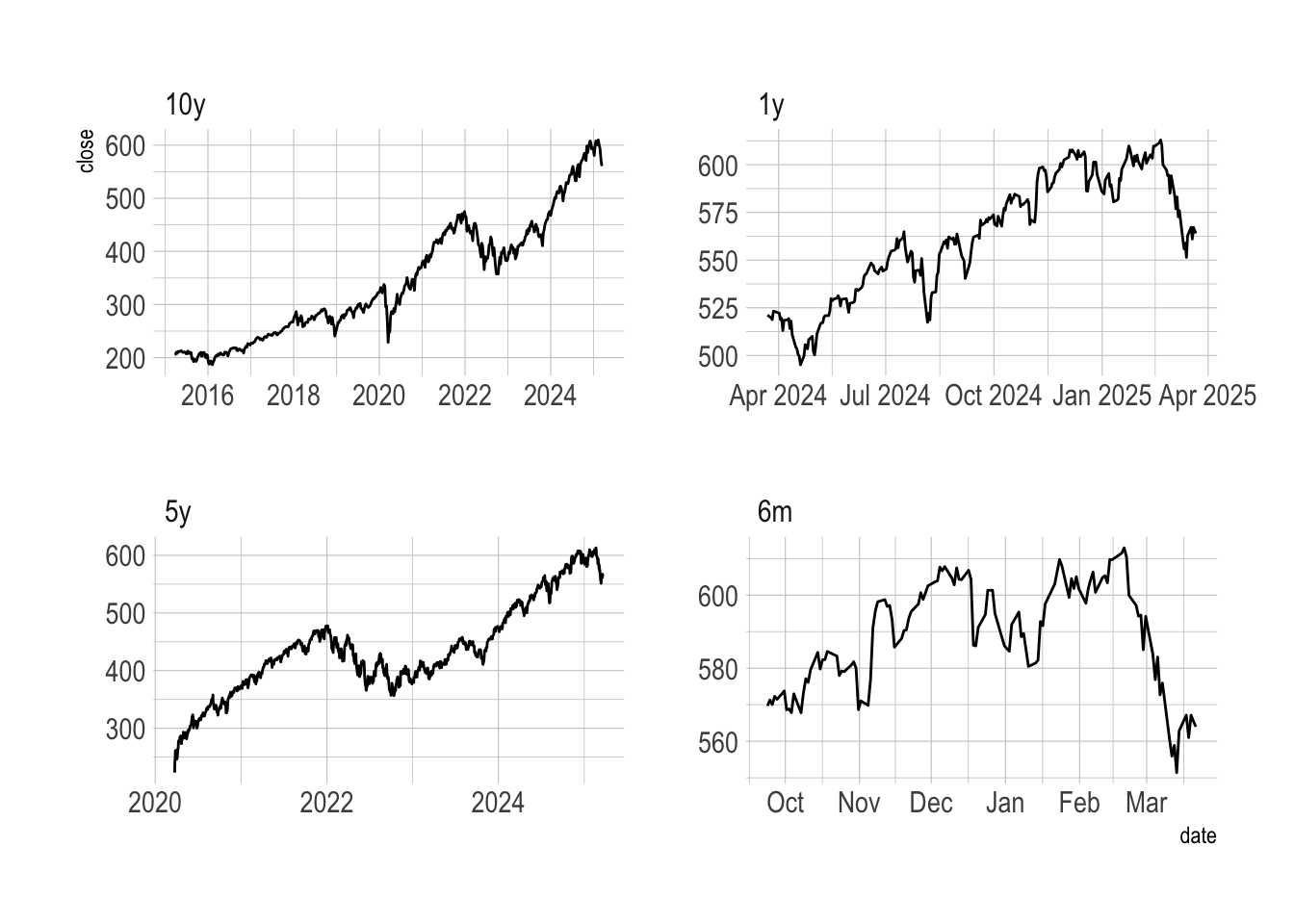

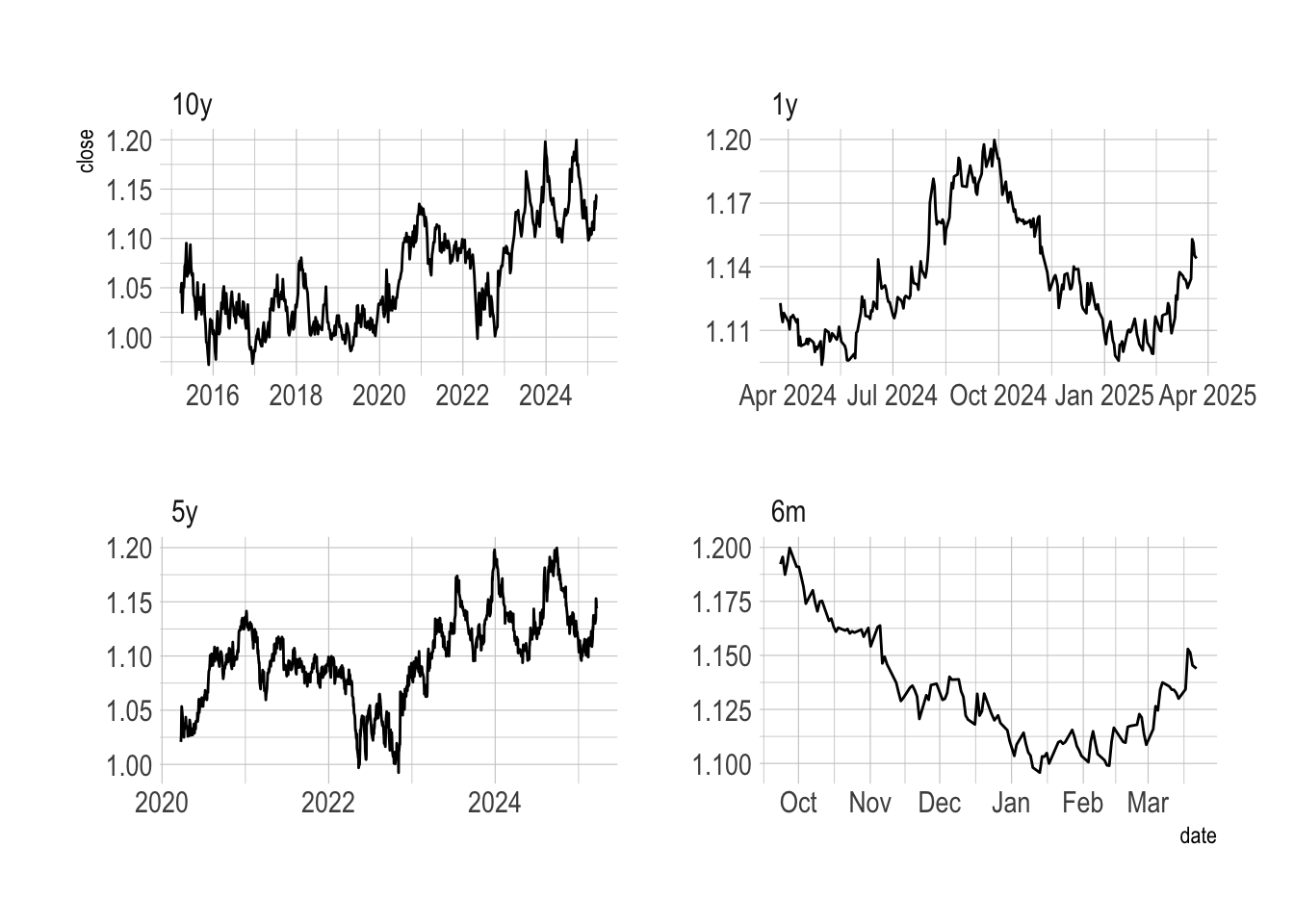

Let’s first take a look at US equity indices. As we can see from the Long term 10-year plot, the equity market is a long trending market. I am not sure it would be right to see the Long term distribution in this way, or instead we should normalise it with price/earnings (P/E ratios) to adjust the “inflation”

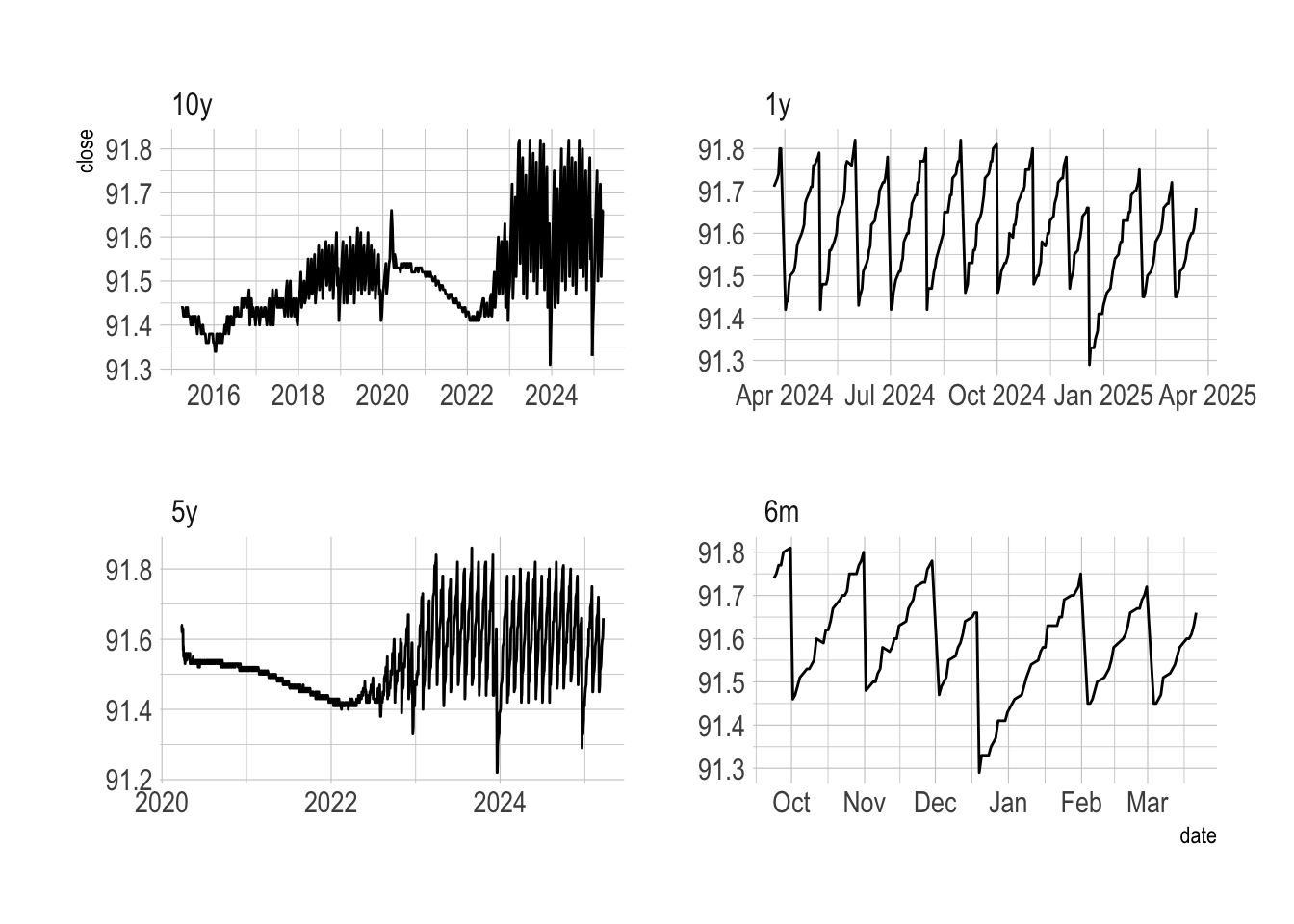

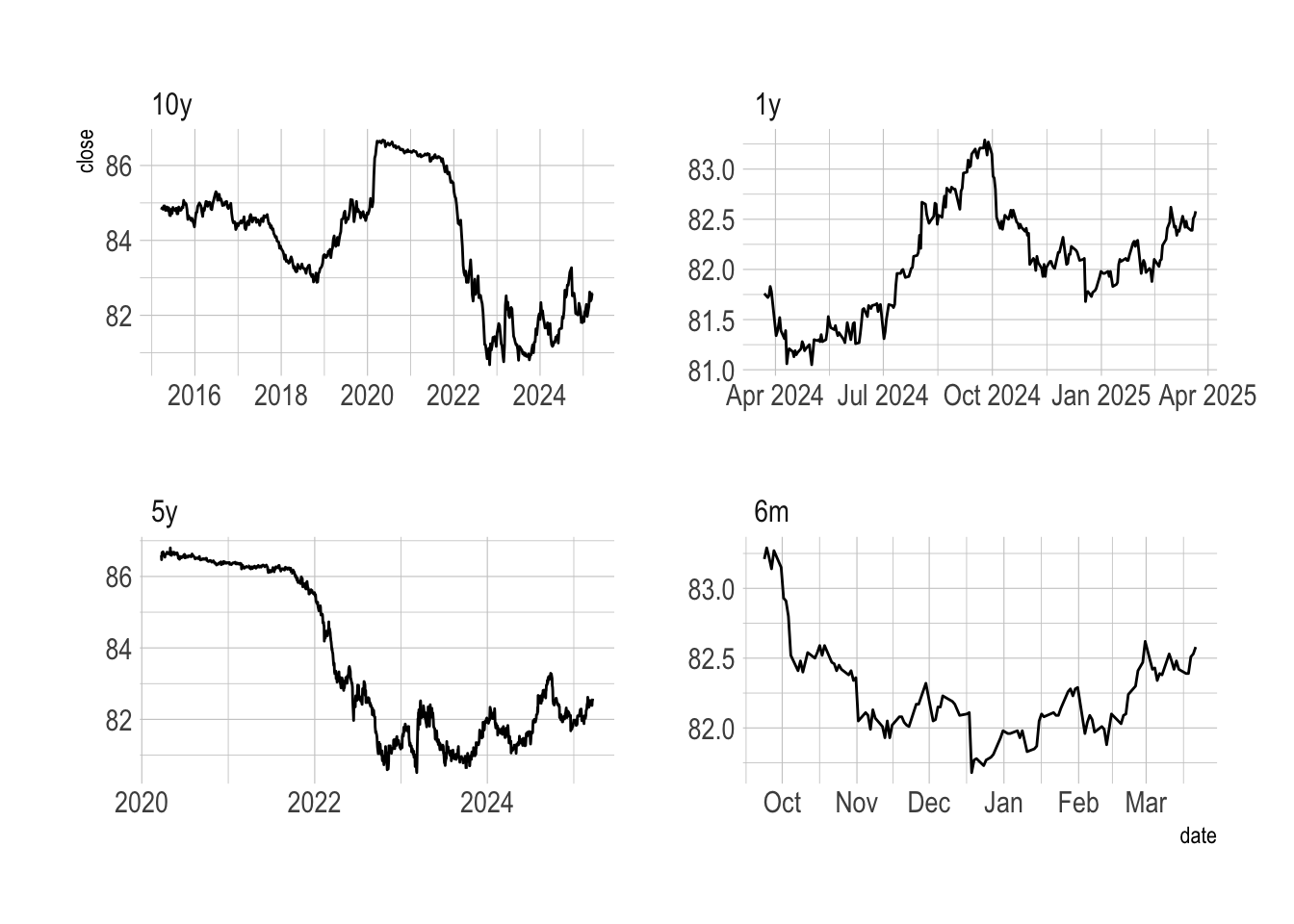

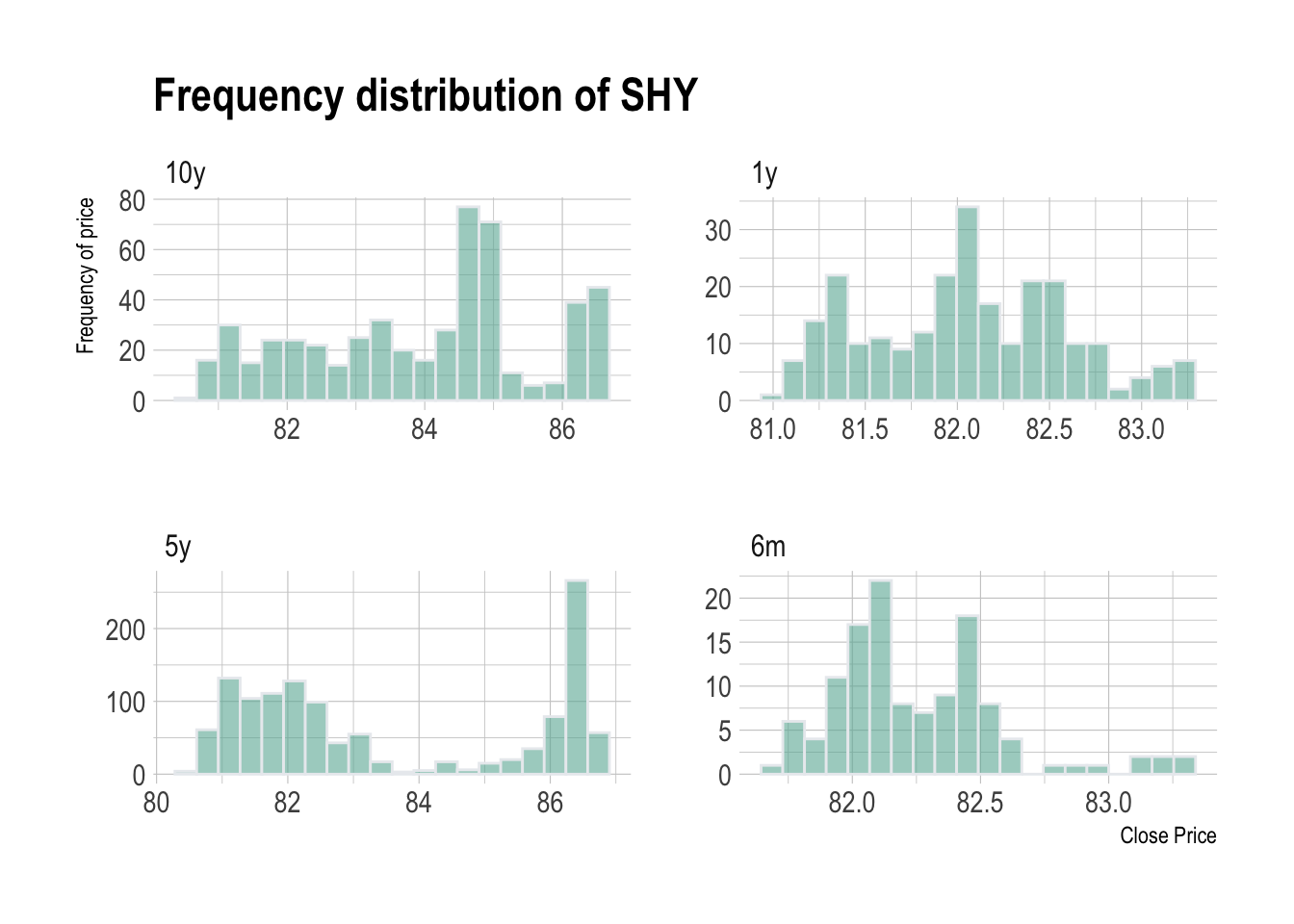

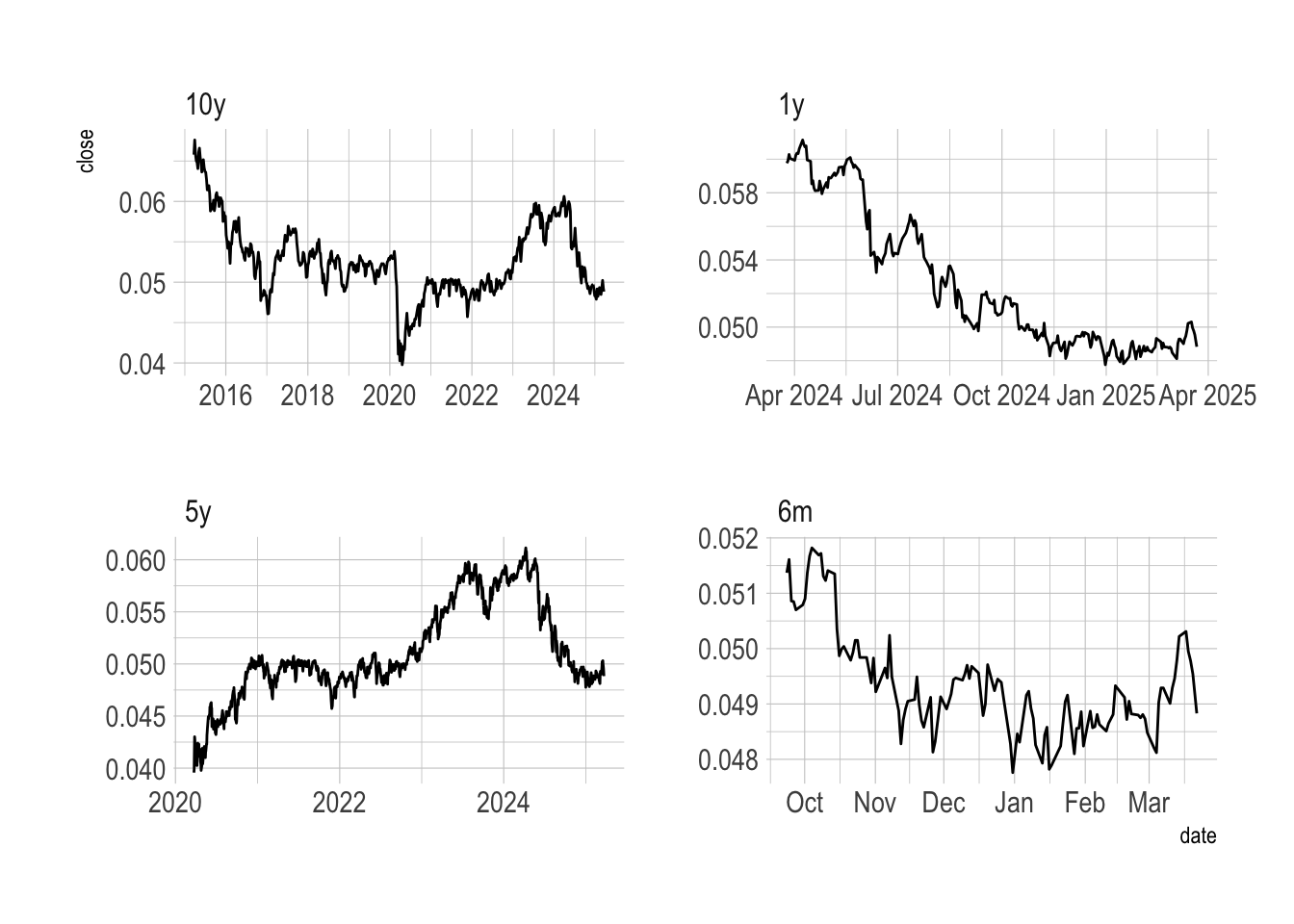

The bonds market is an important market as it is traded a lot with institutions. Comparing to the equity market, the bonds market is not a trending market in long term.

7.1 BIL (1-3 year T-Bills)

The T-bill has a very close trading range between 91.3 to 91.8 across all timeframes. It is more common to trade at the range between 91.4 to 91.5.

Similarly, the SHY has also a quite tight trading range between $78 to $88. In the last 5 years, the price of SHY slumped from the range of $86 to the range of $82, and trading around this range. In the past 6 months, it is more common to trade between the range of $82 to $82.5, where $82 is the key level.