Enough is enough

After 2 years of trading, I think I learnt the basics about the market. I start to get comfortable to trade with different asset classes - which I consider is something that I have learnt in this period of time. However, I still cannot be consistent. I feel like sometimes I do well but most of the time I don’t.

The drawdown from the beginning of 2025 is painful. I think I am just not a good subjective pattern discretionary trader. I am a data scientist, and my strength is to do computarised data analysis. Can I use this expertise to build trading systems that help achieve my financial objectives? A thousand mile trip begins with one step. Let’s get started.

What are my needs?

As inspired by Kevin J. Davey’s book, successful trading systems come with a S.M.A.R.T goal. Here is the mission statement of my trading system:

I will create a trading system in six months, one that trades the ETFs, returns an average of 20 percent per year, with a maximum drawdown of 5 percent, a winning percentage of 45 percent or higher, and follows all the steps in a well‐defined development process.

Having this mission in mind, here are the list of things that I like with the system, and the list of things that I don’t like with the system.

| Things I like | Things I don’t like |

|---|---|

| Trade ETFs only | Over-complicated strategies (Pairs Trading, complex options, etc) |

| 30% annual return, 5% MDD (I am really risk averse and don’t like losing - happy to not achieve 100% per year, but need to limit drawdown) | Average down to losing positions |

| Trade daily timeframe - I am a part time trader and I only have 1-2 days a week to generate trading signals | Holding position for too long (Over 40 days) |

| Average Trading Period - Not more than 30 days (See profit take profit) | |

| Swing Trading style | |

| 100% mechanical - no human intervention in decision making |

As I based in the U.K., I’d also need to be aware of the ETFs that can be traded in the U.K. account. Of course, I also have my H.K. account which can be used to trade required ETFs and Futures.

Trading Style - The framework

I am very thankful to read the great minds of systematic traders. Another great book by Perry Kaufman, A guide to Creating a Successful Algorithmic Trading Strategy, has illustrated the strategy development process.

As the author says, it is not hard to source of trading ideas. However, for an idea to be robust, we need to have a sound premise. Perry suggested these could be:

Trends based on interest rate policy set by the Fed.

Seasonal patterns that exist in agriculture, airline stocks, vacation resorts, heating oil, and other stocks and commodities.

Exploiting the difference between two similar stocks, such as two chip manufacturers, pharmaceutical companies, or home builders.

That’s called stock arbitrage, or pairs trading. Buying or selling price volatility before an earnings report or after a price shock.

Fading an upgrade announcement by a major firm (old news by the time it prints on the screen). Same-time-next-month patterns, when funds redeem and add to their positions.

The 3-day cycle, based on human nature, but dependable for 50 years.

Weekly patterns, such as, “Up on Monday, down on Tuesday.

Excerpt From A Guide to Creating a Successful Algorithmic Trading Strategy Perry J. Kaufman This material may be protected by copyright.

Based on my needs, I eventually my trading systems will be boiled down to 2 categories - Trend Following and Short-term systems.

I think I will spend most of the time in developing Trend-following system as it suits my needs more. I will be very unlikely to babysit my positions and do intraday trading. I hope to rely on the the system more, and I hope my system can ride on the trend when it works. However, I am a very risk averse person and I don’t like systems with very low win rate along with high R/R. It would be a big deal to take a balance between them.

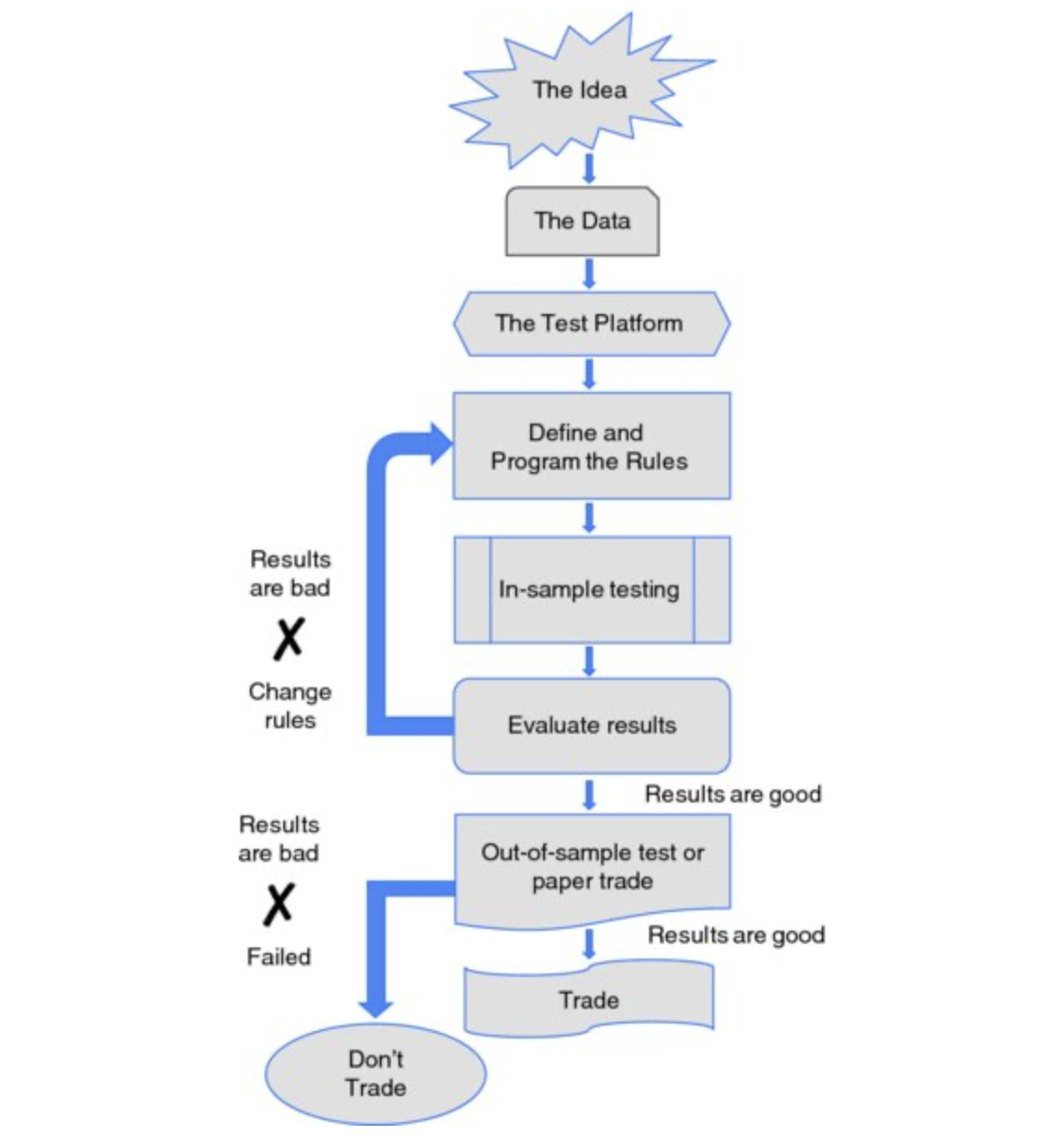

From Idea to system

The system rationale and the details

A system profile would not change a lot. For example, a trending system expect taking small losses and fishing for big fish. The details are just hidden in how to find a trending asset, or when will the asset be trending. As long as the concept is the same, the details of different trading methods are not that different.

Backtesting software

Before writing this article, I have just test quantstrat in R. However, one thing I really don’t like is it cannot write a strategy that buy and sell on the same day. More importantly, it is very hard to define position sizing rules. I think I will need 2 sets of position sizing rules - one for Stocks/ETFs and another one for Futures.

I may also test backtesting.py as well for some of the systems. Hope it will work better.