One great learning from Perry Kaufman is to use the efficiency ratio to measure the noise of the market. Kaufman’s Efficiency Ratio was invented in the 1970s to measure how noisy the market is, and from his book Trading Systems and Methods, 5th edition, Chapter 1.

Here’s the formula for the n-day Efficiency Ratio.

\[

ER = \frac{|P_t-P_{t-n}|}{\sum_{i = t-n}^{i = t}|P_i-P_{i-1}|}

\]

The idea is simple. A trend with high efficiency ratio is smooth and linear. Conversely, a trend with low efficiency ratio is choppy.

As we see from the formula, the efficiency ratio will be based on different factors:

The timeframe: In lower timeframe prices tend to fluctuate more

The length of the window

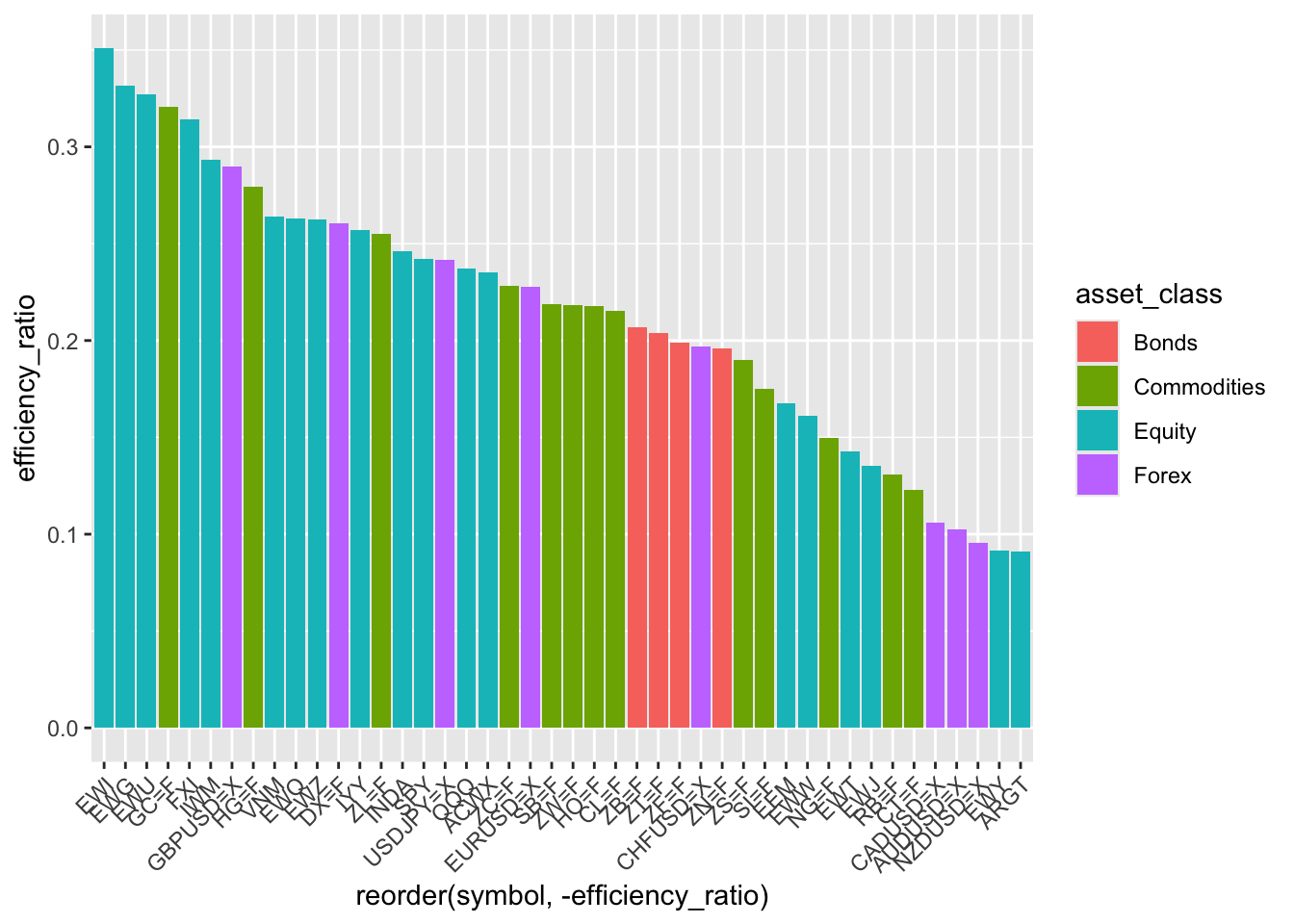

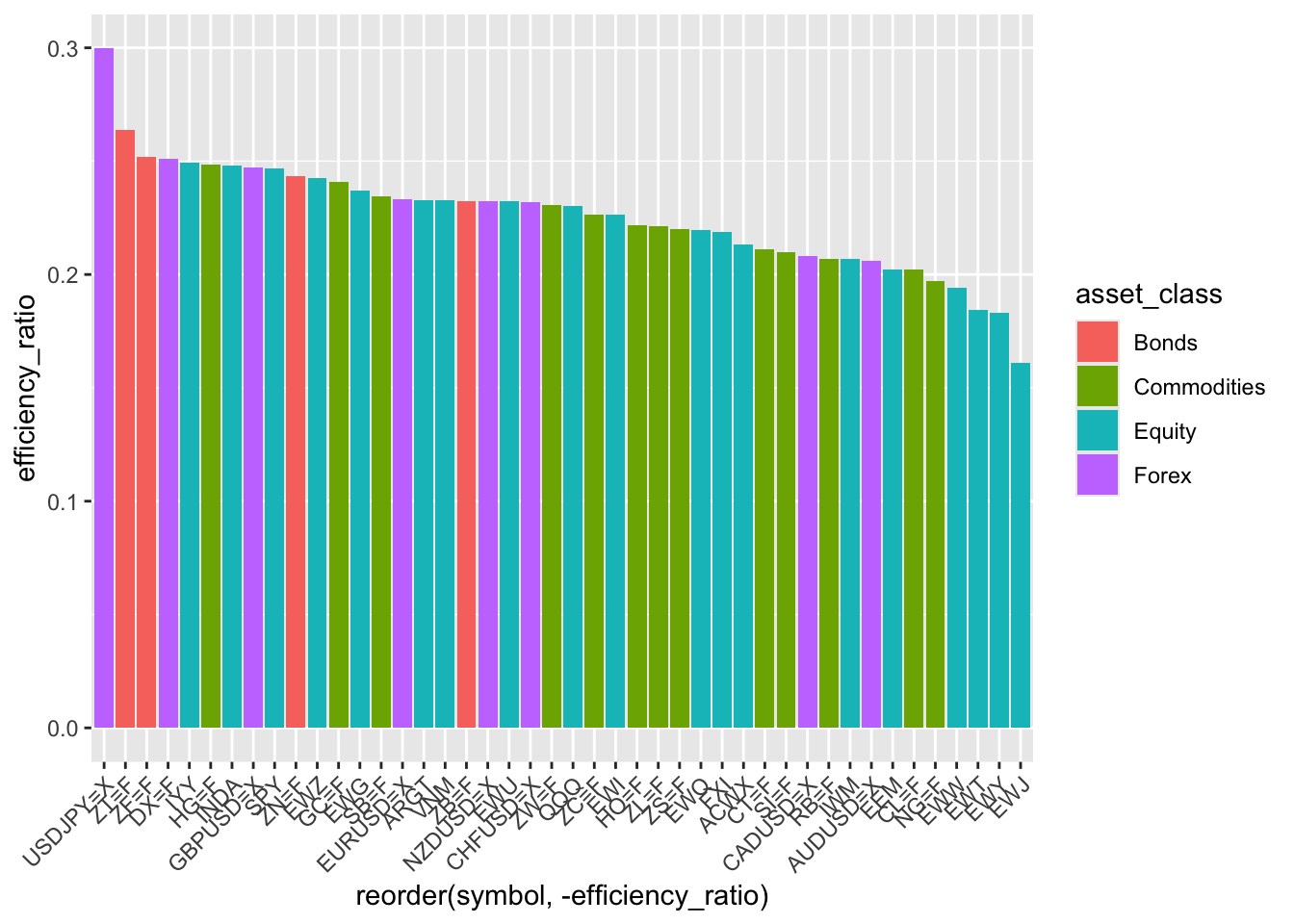

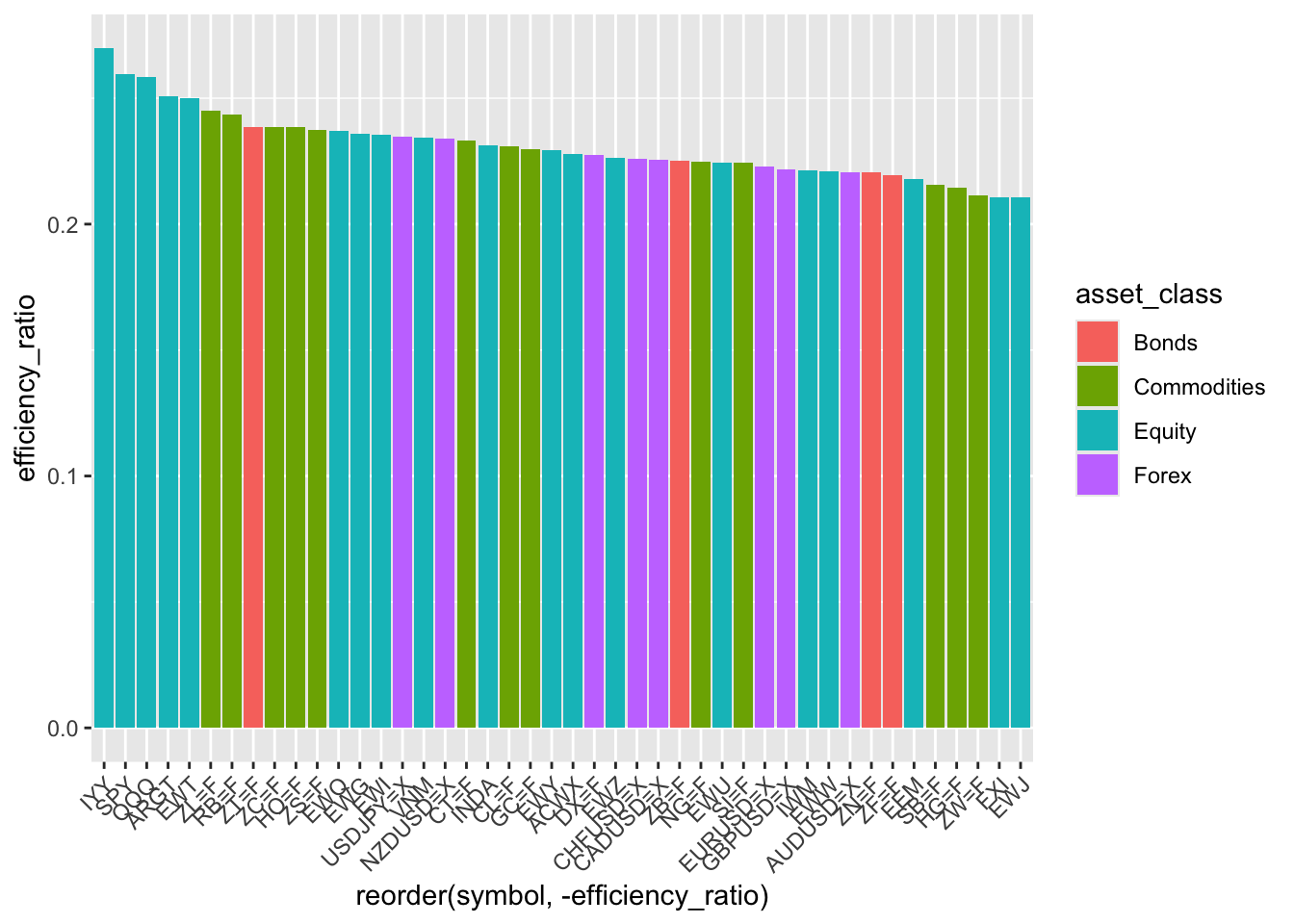

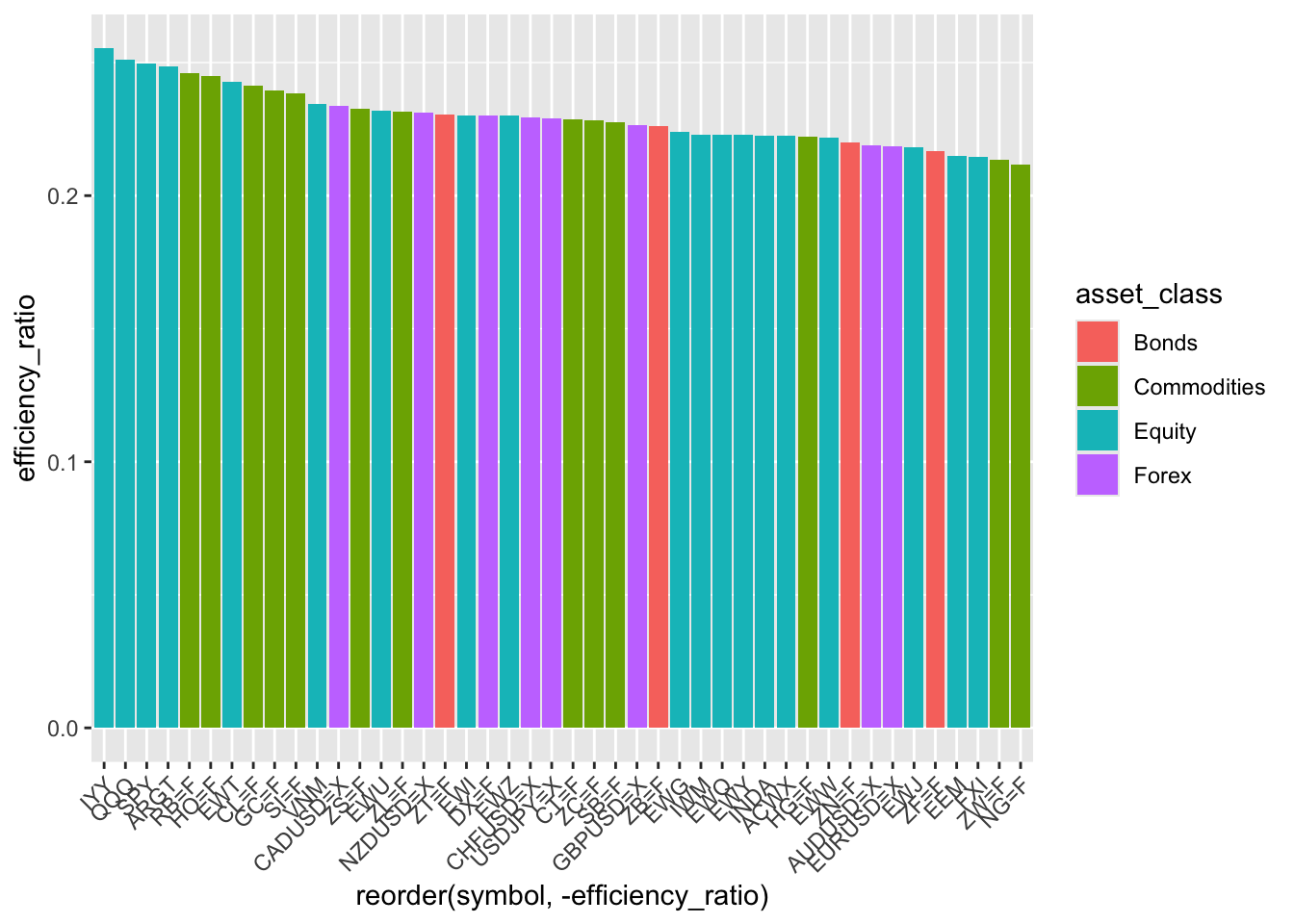

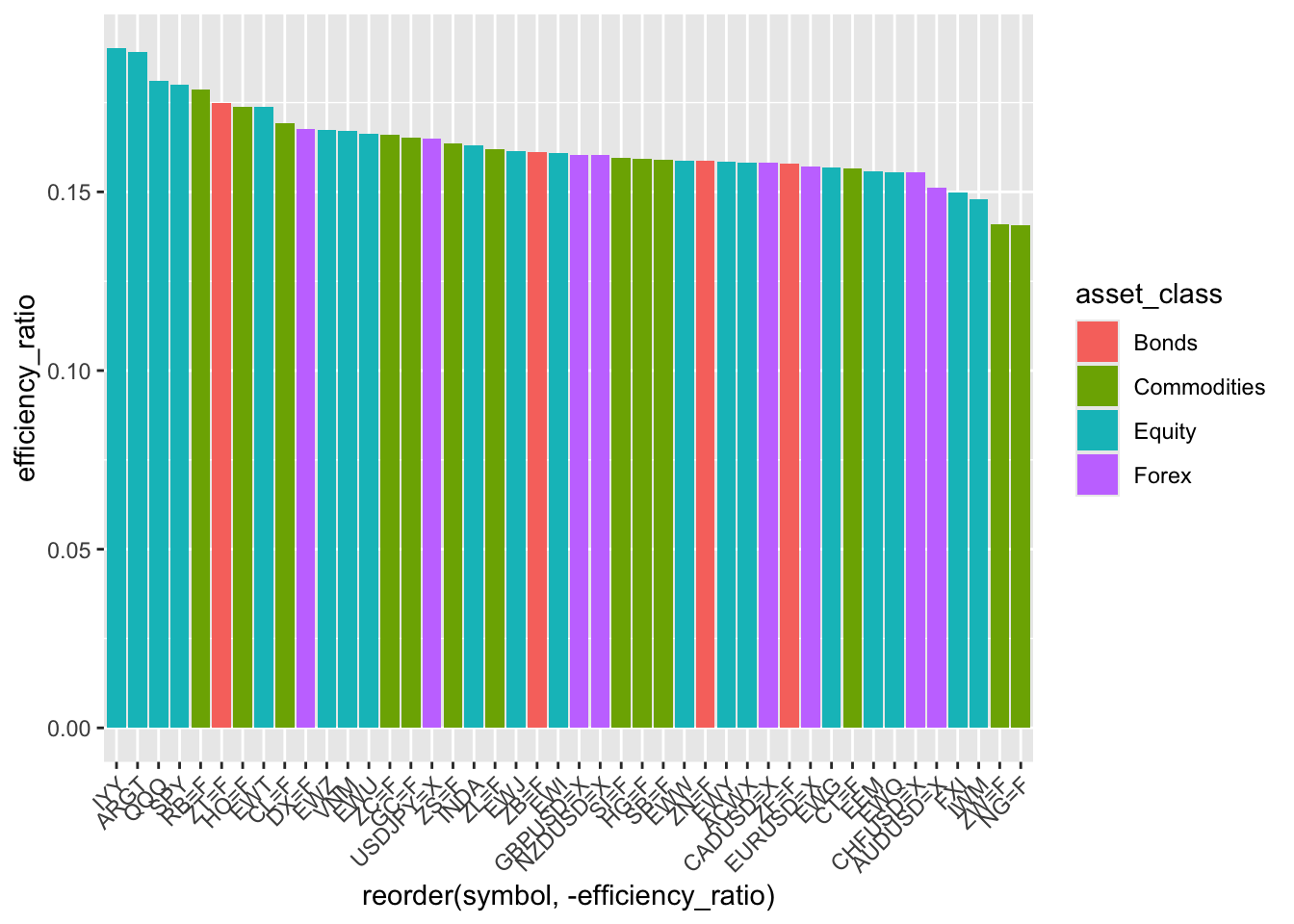

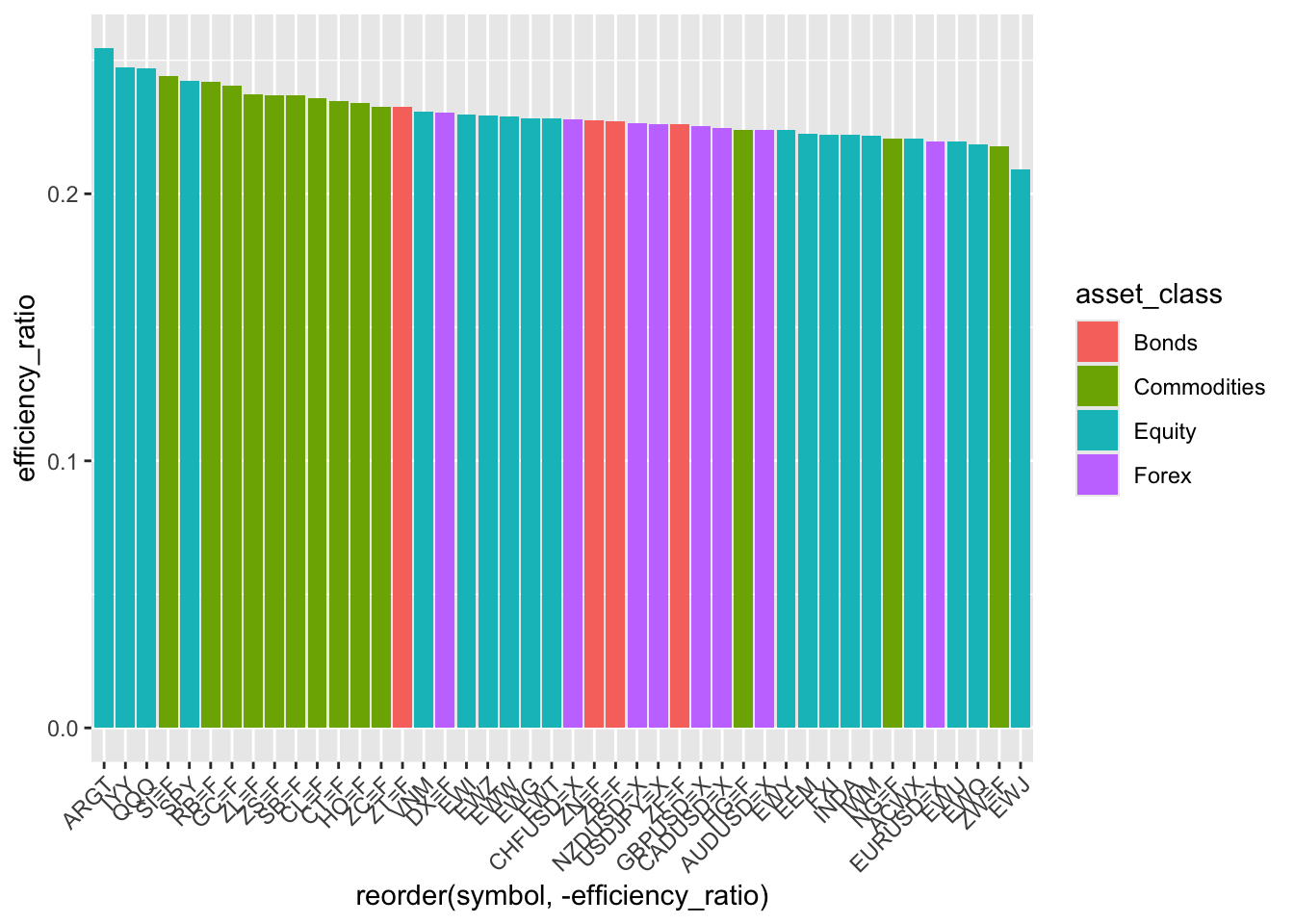

Efficiency ratio across markets for last 5 years

We will examine the efficiency ratio across the following asset classes (or proxy ETFs)

Equity:

US: IYY, SPY, QQQ, IWM

Asia: FXI, EWJ, VNM, INDA, EWY, EWT

Europe: EWQ, EWI, EWG, EWU

South America: ARGT, EWW, EWZ

Emerging markets: ACWX, EEM

Bonds: SHY(1-3 years TBond), TLT (20+ Year Treasury Bond)

efficiency_ratios <-c()for (symbol in universe) { efficiency_ratios <-c(efficiency_ratios, efficiency_ratio(Cl(get(symbol)), n =20))}result <-data.frame(symbol = universe,asset_class = asset_class,efficiency_ratio = efficiency_ratios)ggplot(result, aes(x =reorder(symbol, -efficiency_ratio), y = efficiency_ratio, fill = asset_class)) +geom_bar(stat ="identity") +theme(axis.text.x=element_text(angle=45, hjust=1))

Conclusion

It is interesting to see that the findings is different from what Kraufman suggested in his book (p. 13). It could be due to the fact that the market is always changing.

In past 5 years, futures market are trending and linear, while emerging market and small-caps are choppy. It could be a good insights to design relevant trading strategies.